Closing the Emissions Gap: A Climate Action Roadmap for Limiting Warming to 1.5°C

About the blog

Authors: Sophie Boehm, Clea Schumer, Kelly Levin, Louise Jeffery (CAT), Claire Fyson (CAT), Joe Thwaites, Stephen Naimoli, Aman Majid (CAT), Katie Lebling, Anna Nilsson (CAT), Judit Hecke (CAT), Michelle Sims, Joel Jaeger, Ryan Wilson (CAT), Rich Waite, Emily Cassidy, Andreas Geiges (CAT), Anderson Lee, Neelam Singh, and Sebastian Castellanos.

Table of contents:

- Summary

- 1. Transitioning to Zero-carbon Power

- 2. Decarbonising Buildings

- 3. Reducing Industrial Emissions

- 4. Shifting to More Sustainable Modes of Transport

- 5. Protecting and Restoring Ecosystems

- 6. Shifting to More Sustainable Food Systems

- 7. Scaling Up Carbon-removal Technologies

- 8. Scaling Up Climate Finance and Aligning Financial Systems with 1.5˚C

- Getting Climate Action on Track for 2030 and 2050

- Links

Summary

The science is clear about how to prevent increasingly dangerous and irreversible climate change impacts: Limit global temperature rise to 1.5˚C (2.7˚F), which means cutting GHG emissions in half by 2030 and reaching net-zero CO2 emissions by mid-century.

While countries, companies, cities and investors have announced some encouraging commitments to help achieve this global goal, they’re far short of what’s needed. Worse still, new research shows the world’s highest-emitting sectors — power, buildings, industry, transport, forests and land, and food and agriculture — aren’t acting anywhere near fast enough.

The State of Climate Action 2022 report analysed progress across 40 indicators of action needed by 2030 and 2050 to limit warming to 1.5˚C, everything from increasing renewable energy uptake to halting deforestation to shifting to more sustainable diets. We found that none of the 40 indicators assessed are on track to achieve the 2030 targets.

While most indicators (27) are heading in the right direction, they’re moving far too slowly to cut GHG emissions in half by 2030, and are categorised as “off track” or “well off track” accordingly. Of the remaining indicators, five are heading in the wrong direction entirely and another eight lack sufficient data to assess progress.

Here’s what’s needed this decade to close the gap in climate action across the world’s highest-emitting sectors and keep the 1.5˚C goal alive:

1. Transitioning to Zero-carbon Power

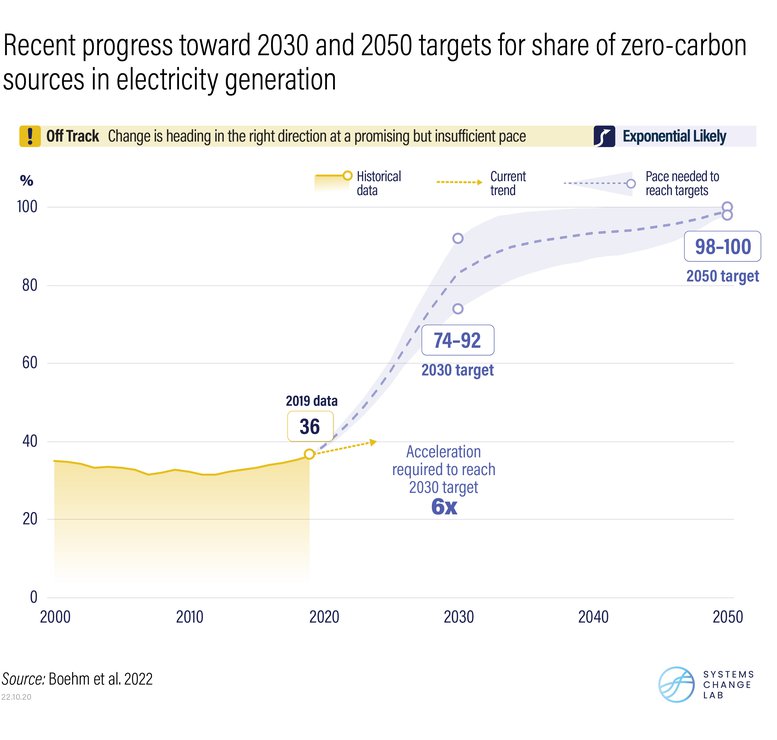

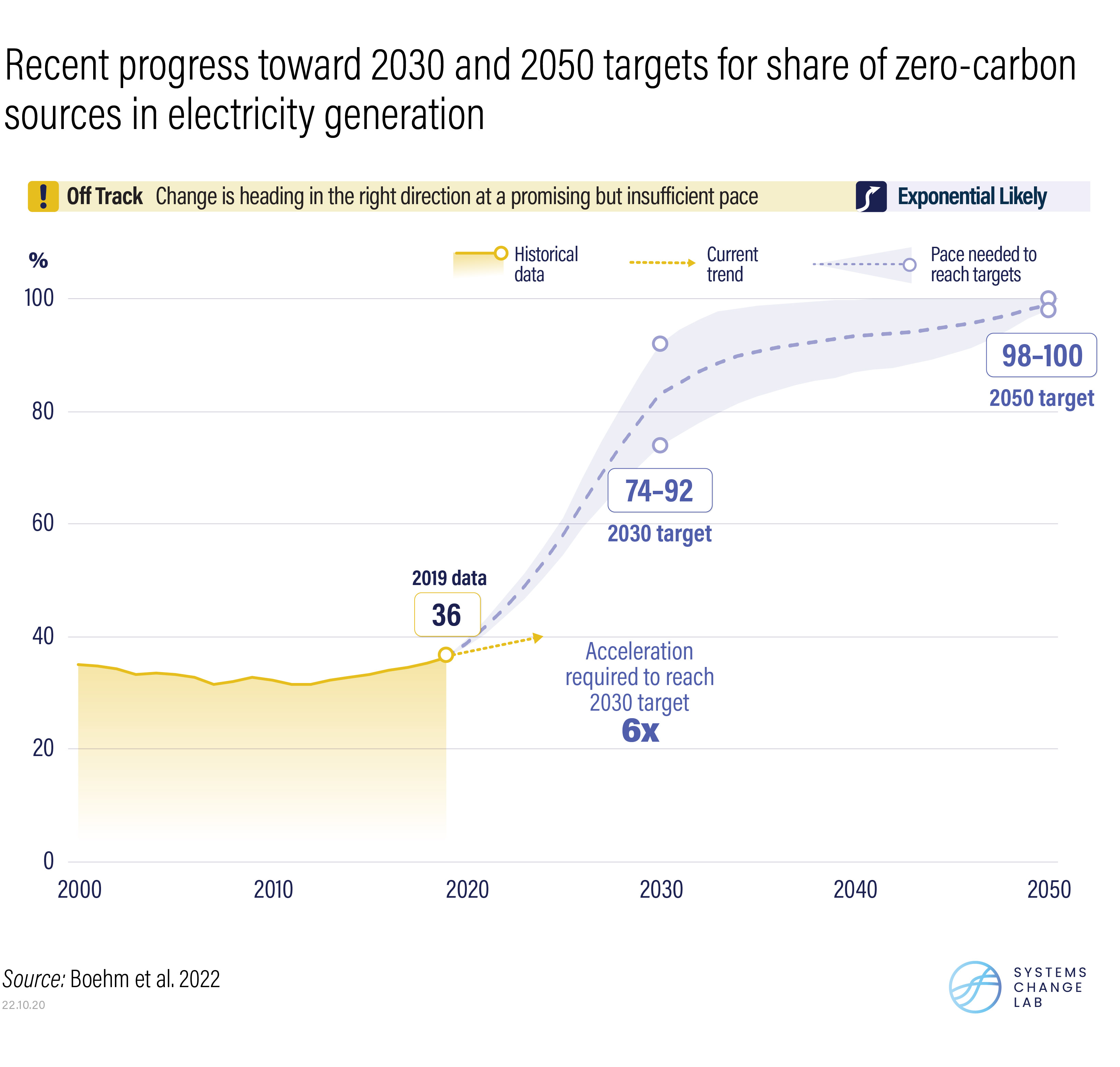

A major transformation is underway across the global power system, the world’s largest source of CO2 emissions. Adoption of zero-carbon power sources, including solar and wind, is on the rise, with recent years witnessing record-breaking growth that shows no signs of slowing. From 2019 to 2021, for example, solar generation grew by 47% and wind by 31%.

However, because total electricity generation also continues to increase, the share of electricity from zero-carbon power sources has experienced almost no net change since 2000. In fact, emissions from the power system hit an all-time high in 2021, ramping up after a temporary decline during the COVID-19 pandemic. Coal-based electricity generation, although declining globally, continues to expand across some regions, such as in Japan, China and India, while gas-based electricity is still rising around the world. These trends are largely offsetting gains made in scaling up zero-carbon power generation.

To meet growing demand for power and keep the 1.5˚C warming limit within reach, increases in the share of electricity generated from zero-carbon power sources must accelerate six times faster this decade. The good news is that, if properly nurtured with supportive policies, adoption of zero-carbon power technologies could follow a nonlinear trajectory and scale up much faster than in the past.

At the same time, unabated coal in electricity generation must be phased out six times faster — equivalent to closing down roughly 925 average-sized, coal-fired power plants each year through 2030 — and natural gas use needs to start decreasing instead of increasing.

2. Decarbonising Buildings

By 2030, the world’s buildings must not only become considerably more energy efficient, but also transition to zero-carbon energy. But despite the widespread availability of zero-carbon technologies like heat pumps, recent efforts to decarbonise this sector continue to fall far short of the transformational change required.

The amount of energy used per square metre of floor area in buildings (also known as energy intensity), for example, declined during the 2000s and early 2010s, but progress has slowed recently. Holding warming to 1.5˚C will require energy intensity improvements to accelerate nearly seven times faster in residential buildings and five times faster in commercial buildings over this decade. Decarbonising buildings will also require meeting remaining energy needs with low-carbon or zero-carbon sources — for example, by electrifying operations and using renewables to produce that electricity.

Achieving 2030 targets for both energy intensity and carbon intensity of buildings will require retrofitting rates of existing buildings to increase from less than 1% today to 2.5%-3.5% per year by 2030, especially in developed economies across Europe and North America.

Simultaneously, new buildings should be designed to operate without generating emissions, including avoiding new connections to gas grids, and their construction should rely on low-carbon, circular materials wherever possible. Failure to do so risks significant carbon lock-in.

3. Reducing Industrial Emissions

Since 2000, total GHG emissions from industry — which encompasses the production of goods and materials like cement, steel and chemicals, as well as the construction of roads, bridges and other infrastructure — have risen faster than in any other system.

Historically, efficiency improvements have reduced the amount of GHGs emitted per unit of production. But rising demand for industrial products is now offsetting these efficiency gains, thereby increasing total emissions. And recent efforts to electrify industrial processes — a key climate change mitigation strategy when coupled with a decarbonisation of the electricity supply — must move 1.7 times faster to help change the course of this sector’s emissions trajectory.

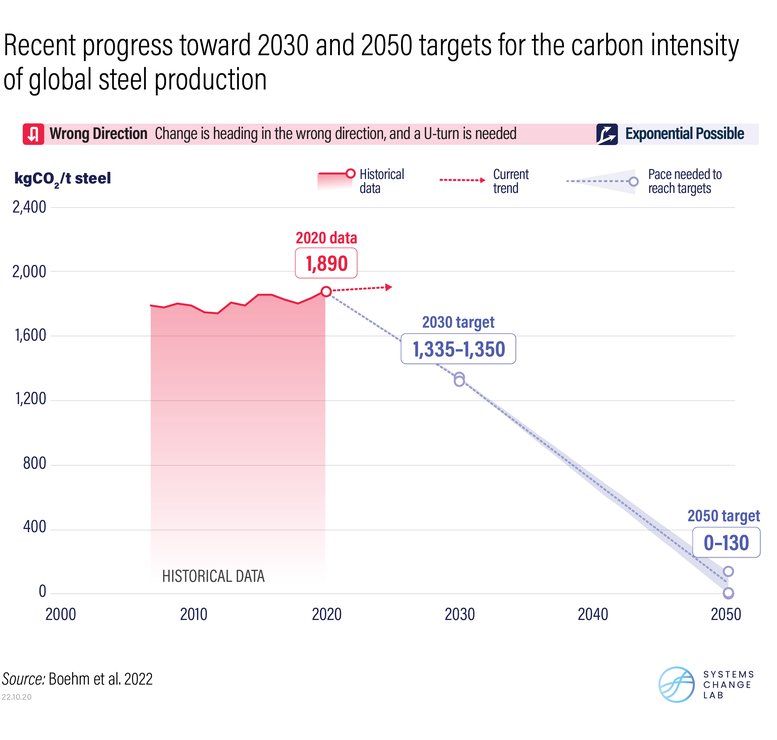

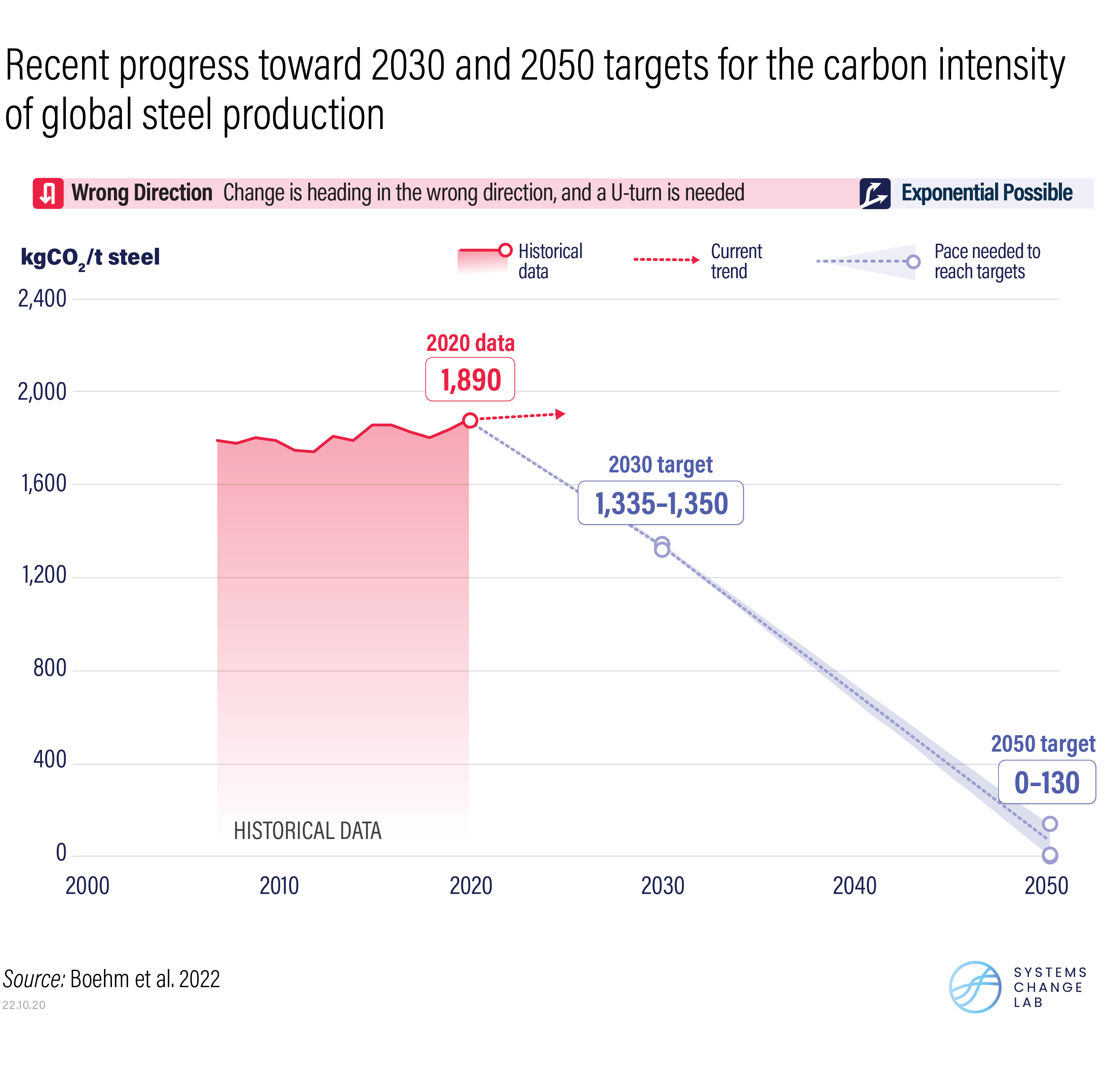

It’s also critical to develop new technologies that can decarbonise the hardest-to-abate industrial operations, including high-heat processes that cannot easily be electrified or chemical reactions that emit GHGs (known as “process emissions”). Recent efforts to improve the carbon intensity of cement production, for example, remain well off track, requiring these gains to accelerate more than 10 times faster this decade. Even more concerning, the carbon intensity of steel production is heading in the wrong direction entirely, likely due to increased reliance on emissions-intensive production processes in China, which manufactures more than half of the world’s steel.

Lowering emissions across these hard-to-abate sub-sectors will require much faster deployment of low-carbon steel plants, as well as low-carbon cements and zero-carbon technologies like green hydrogen.

4. Shifting to More Sustainable Modes of Transport

Economic development gains have increased travel and car ownership, spurring steady growth in transport emissions. Although system-wide emissions dropped in 2020 during the COVID-19 pandemic, preliminary data from 2021 indicate that a rebound is already well underway.

Private car use, a big source of transport emissions, continues to rise, remaining stubbornly high in wealthy countries like the United States and Canada. Changing course will require shifts to more sustainable modes of transport, including walking, bicycling and public transit. Yet recent efforts to build out the requisite infrastructure, such as networks of metros, light-rail trains, rapid transit buses and high-quality bicycling lanes, are well off track across the world’s highest-emitting cities. Recent rates of change need to accelerate six-fold and more than 10-fold for public transit and bike lanes, respectively.

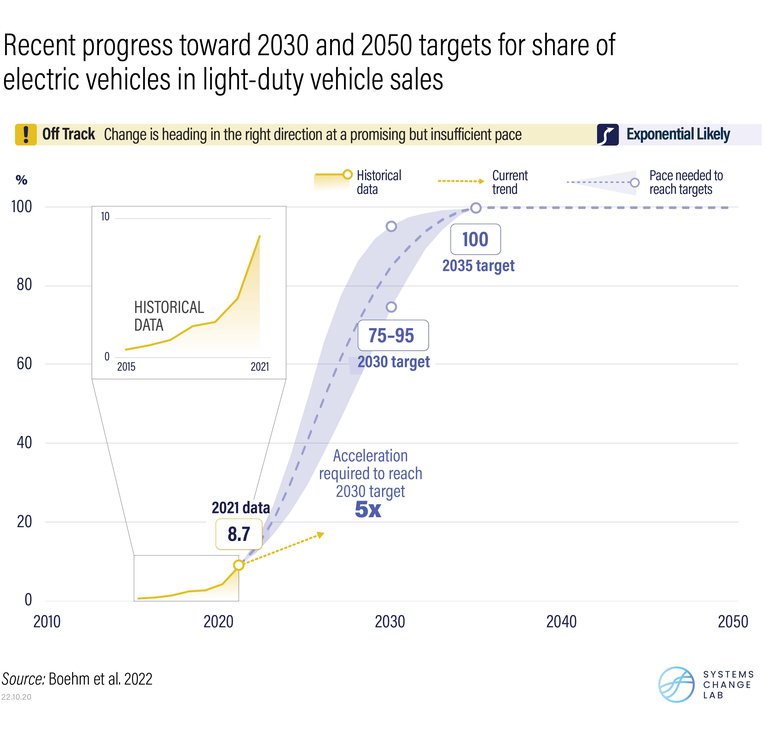

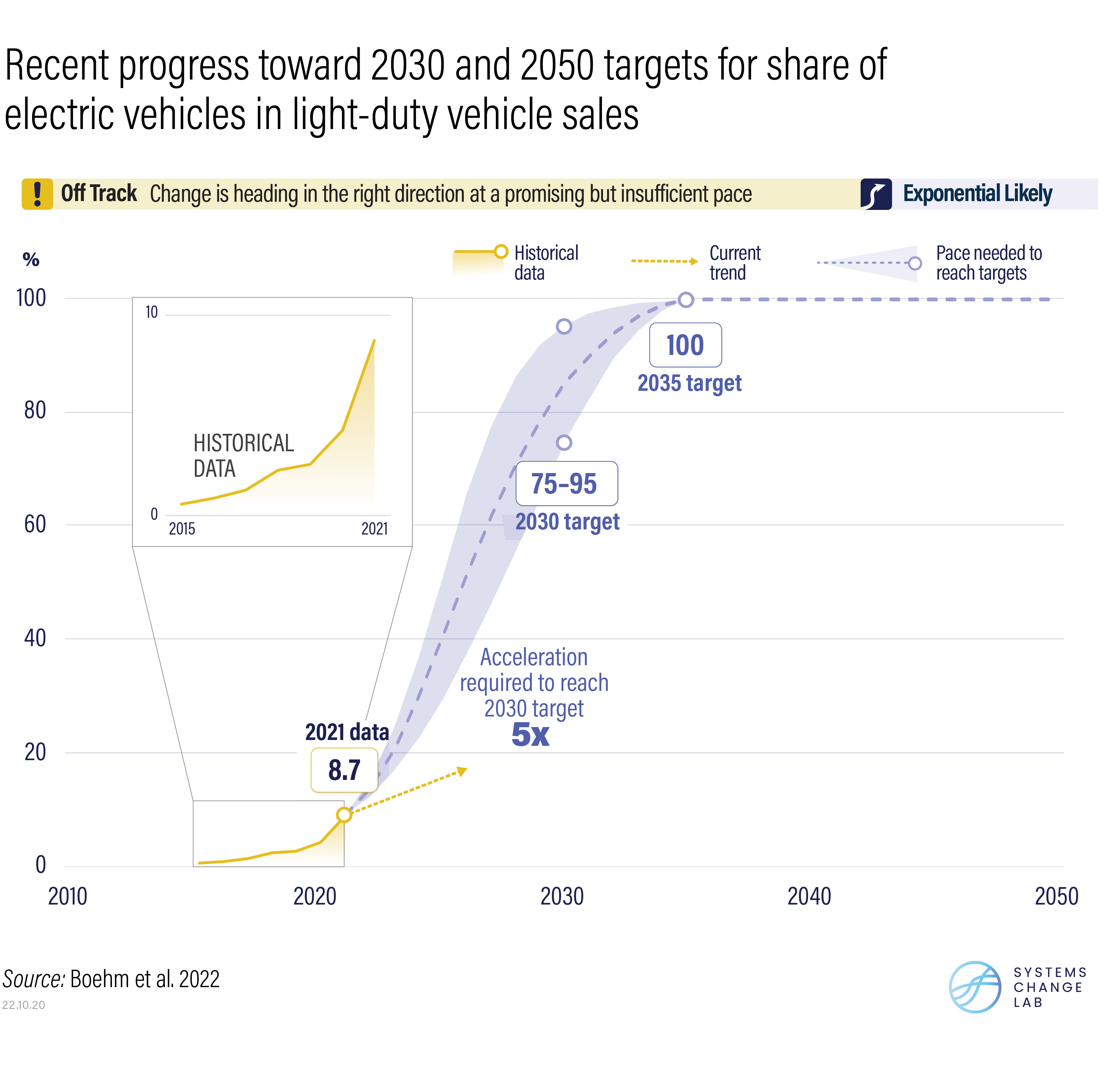

Where these modal shifts may prove difficult to achieve, electric vehicles (EVs) can fill in the gaps. The good news is that this transition is beginning to take off. The share of EVs in light-duty vehicle sales, for example, reached almost 9% in 2021 — a doubling from the year before. And in many major markets, EVs are already cost-competitive with fossil fuel-powered cars. These promising signs of accelerating growth suggest that electric passenger car adoption, which must move five times faster over this decade, will likely experience exponential change in the coming years.

Shifting to zero-carbon technologies in long-haul transport, however, is more difficult. Adoption of electric trucks, for example, lags far behind uptake of electric passenger cars, as battery costs are only beginning to come down enough to make electrification economical. The share of sustainable aviation fuels in the global aviation fuel supply was less than 0.1% in 2020, and efforts to scale them up remain well off track. Zero-emission fuels in maritime shipping are even further behind: They have yet to reach commercialisation, although many pilot and demonstration projects are underway.

5. Protecting and Restoring Ecosystems

Limiting warming to 1.5˚C will require dramatically reducing deforestation and mangrove loss over the next decade, as well as effectively halting peatland degradation. Safeguarding these ecosystems, which collectively hold carbon stocks equivalent to more than three times cumulative global emissions from 1990-2019 (1,020 GtC or 3,740 GtCO2), is critical to near-term climate action. Forests, mangroves and peatlands can rapidly lose carbon after certain disturbances like fire, but can take lifetimes to regain their carbon stores. It would take up to 10 decades for forests to rebuild lost carbon stocks, over a century for mangroves and centuries to millennia for peatlands.

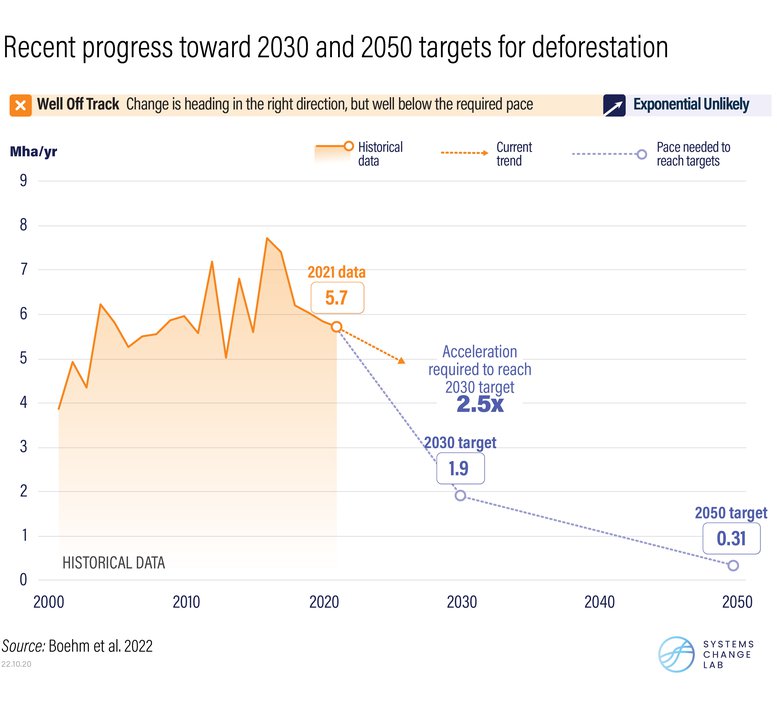

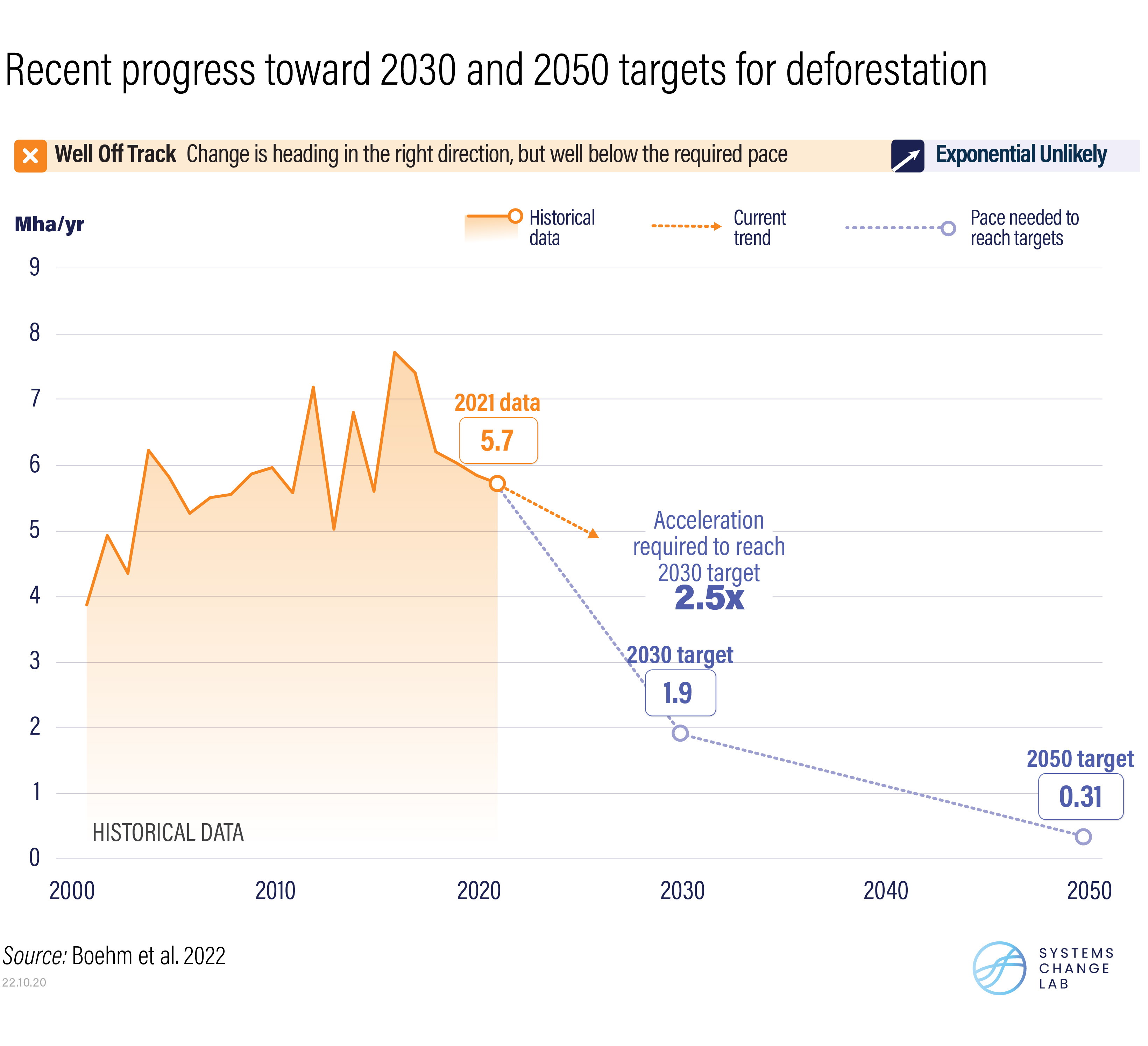

Yet global initiatives to protect these ecosystems remain woefully insufficient. From 2015 to 2021, deforestation occurred across an area roughly the size of Iraq (45 million ha), emitting a total of 25 GtCO2e, or roughly 42% of global GHG emissions in 2019. Worse still, nearly half of these losses happened in humid tropical primary forests, among the world’s most important lands for biodiversity and carbon storage. Getting on track for 2030 requires that annual declines in deforestation occur 2.5 times faster — equivalent to avoiding deforestation across an area roughly half the size of Puerto Rico each year.

The world also needs to restore 300 million ha of forests and 20 million ha of peatlands by 2050, as well as 240,000 ha of mangroves by 2030. But here, too, progress toward near-term targets is inadequate. For example, getting on track for a 1.5˚C pathway would require the world to reforest an area roughly the size of South Korea (10 million ha) annually — about 1.5 times faster than current efforts.

6. Shifting to More Sustainable Food Systems

Transforming the global food system from its current state to one that can feed nearly 10 billion people by 2050 — while lowering GHG emissions and without expanding agriculture’s land footprint — will require immediate action across supply chains this decade. Farmers must produce more food on fewer hectares to avoid clearing more forests for new fields and pastures. At the same time, they need to reduce emissions from a range of agricultural practices, such as those associated with livestock production, rice cultivation and fertilisers.

Recent trends, however, are heading in the wrong direction entirely. Although the emissions intensity of agricultural production fell by 4% over the past five years, total emissions continue to rise, accounting for around 10% of global emissions in 2019.

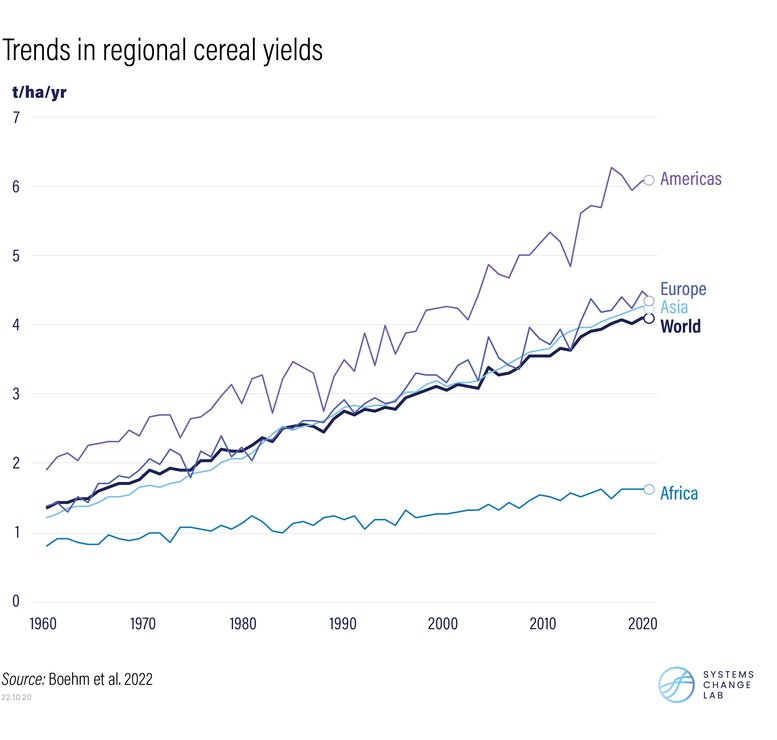

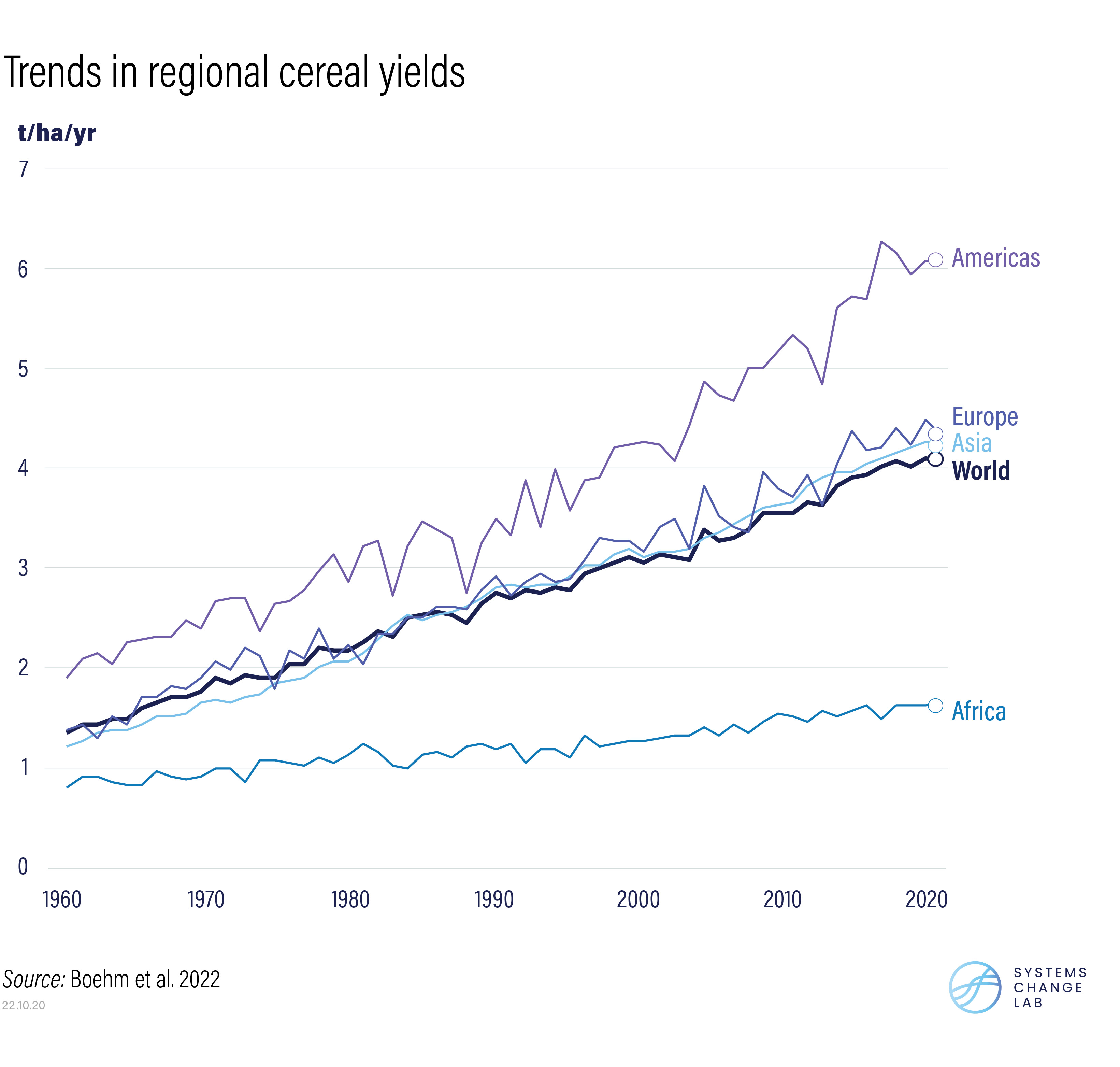

Growth in crop yields must accelerate six-fold over this decade, while annual advances in ruminant meat productivity (the amount of meat from animals like cows, goats and sheep produced per hectare) must occur 1.3 times faster to avoid emitting GHGs from deforestation and without compromising food security. Particular attention is warranted in Africa, where yields have remained stagnant for decades and climate impacts like crop-withering droughts will likely intensify. Increasing resilience to these risks will prove critical in the coming decades, as will the development and deployment of new technologies that boost yields and lower emissions.

Demand-side shifts, particularly among high-income consumers, also play a critical role in mitigating emissions across the global food system. Halving food loss and waste by 2030 and reducing per capita ruminant meat consumption in high-consuming regions by 13% below 2019 levels by 2030 (roughly two burgers a week) and 34% by 2050 (approximately 1.5 burgers a week) can help lower demand for emissions-intensive food. While the data is insufficient to assess progress in decreasing food loss and waste, efforts to accelerate dietary shifts remain well off track, requiring a five-fold increase over this decade.

7. Scaling Up Carbon-removal Technologies

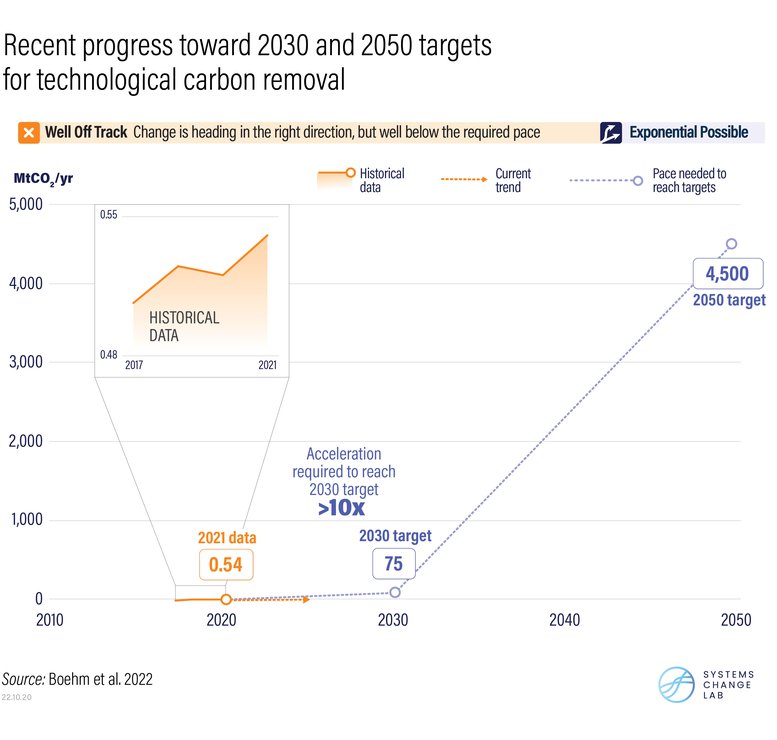

The latest climate science finds that reducing emissions is not enough — holding warming to 1.5˚C will also require removing carbon from the atmosphere, using both natural approaches like reforestation and carbon-removal technologies. The scale of change required over this decade is enormous. Today, existing technologies remove just 0.5 MtCO2 per year, less than 1% of the 75 MtCO2 needed annually by 2030. Getting on track to achieve this target will require a portfolio of technologies to capture and permanently store an additional 7.4 MtCO2 each year.

Public and private investment in carbon-removal technologies is growing, and multiple large-scale projects are expected to come online in the next several years. Both will play a critical role in tackling the many challenges associated with implementing technological carbon removal and in better establishing these technologies’ long-term potential.

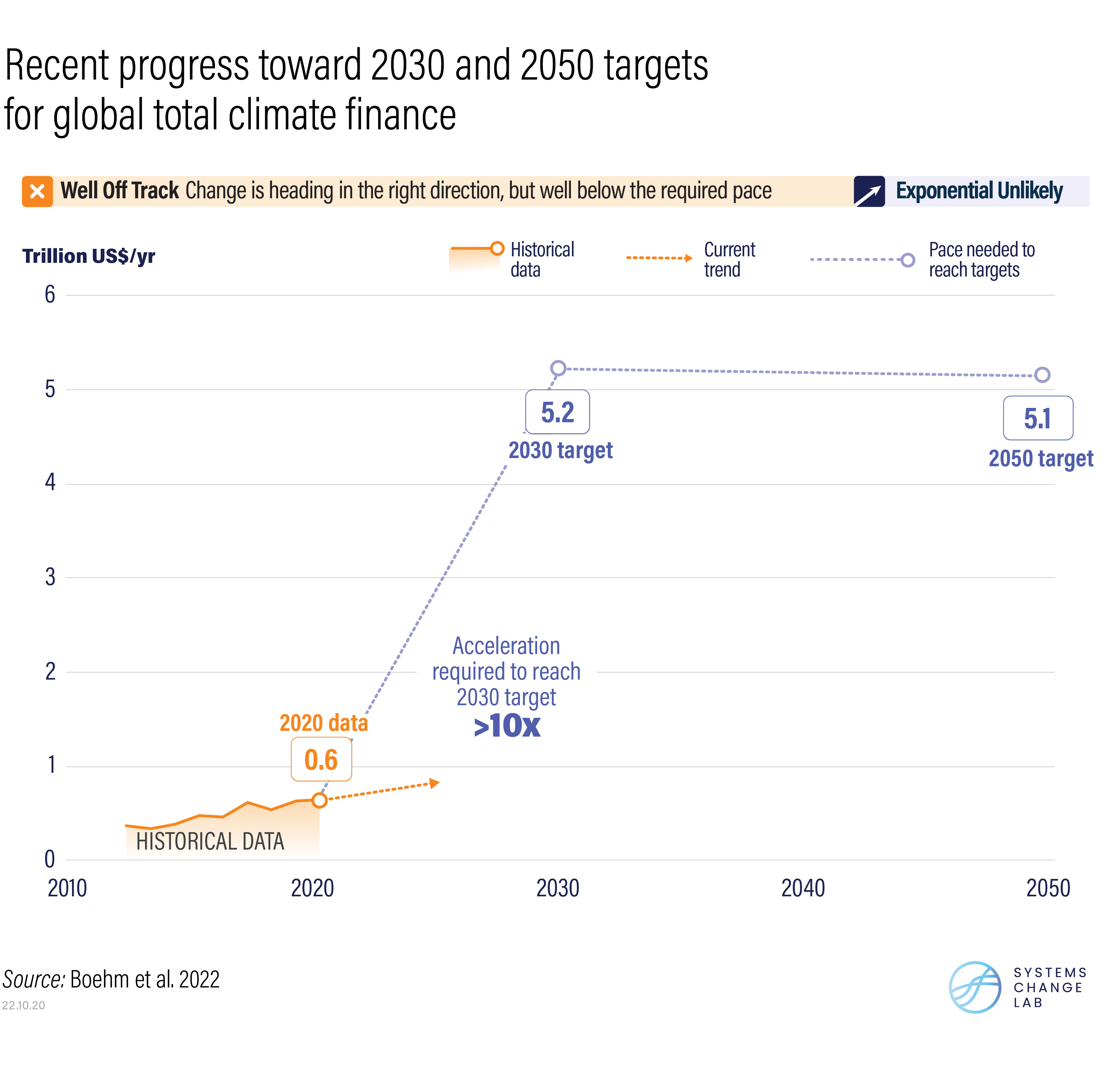

8. Scaling Up Climate Finance and Aligning Financial Systems with 1.5˚C

Accelerating these systemwide transformations will not only require substantial increases in finance, but also the broader alignment of the financial system with 1.5˚C pathways.

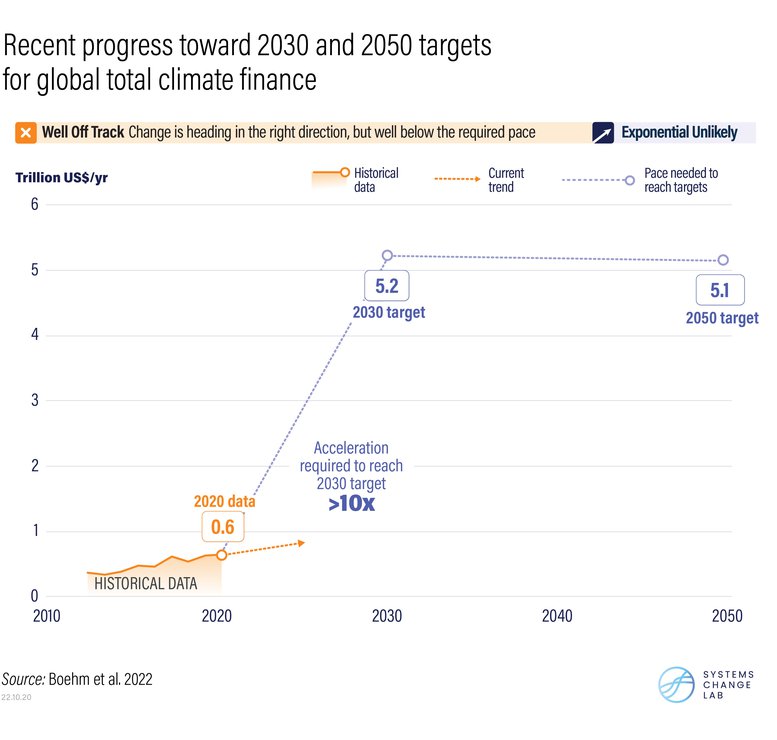

Total climate finance continues to grow globally, but not at the pace needed. To make matters worse, not only has the rate of increase slowed in recent years, but the multiple crises the world now faces — the COVID-19 pandemic, Russia’s invasion of Ukraine and related energy and food price spikes, rising inflation, an economic slowdown, and a wave of sovereign debt crises — pose severe challenges to sustaining and expanding climate investments.

Total climate finance must reach USD 5.2tn a year by 2030, requiring an average increase of roughly USD 460bn a year — more than 10 times faster than current rates. Both public and private finance from domestic and international sources will need to rapidly scale up to achieve this near-term target. Critically, flows from developed to developing countries must increase to at least USD 100bn annually, the collective goal developed countries pledged to achieve by 2020, but have still not delivered.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Boosting climate finance, however, represents just one facet of transforming the financial system. Phasing out investments in high-carbon activities like fossil fuel development and commodities that drive deforestation is equally critical. Here, too, the world has made insufficient progress. Efforts to mandate corporate climate risk disclosure remain well off track, as do carbon-pricing mechanisms and efforts to end public financing for fossil fuels.

Getting Climate Action on Track for 2030 and 2050

Achieving 1.5˚C-aligned targets across all major sectors will require today’s leaders to be clear-eyed about the magnitude and urgency of change required this decade. Emissions today are higher than they were when 196 Parties adopted the Paris Agreement in 2015. The most recent round of national climate commitments delivers only modest improvements in ambition, putting the world on track to curb GHG emissions by just 7% by 2030 (relative to 2019). And countries are now grappling with numerous crises that risk stymying climate action, from Russia’s invasion of Ukraine and its cascading impacts on food and energy security to recessions following the pandemic and rising inflation.

But these circumstances are not entirely bleak. We also have never had more information about the gravity of the climate emergency, nor what needs to be done to mitigate it. Investing in research, development and demonstration of zero-emissions technologies; adopting policies that mandate or incentivise the transition to a 1.5˚C pathway; strengthening institutions to more effectively implement laws and regulations; establishing more ambitious climate commitments and following through on them; and shifting behaviours and social norms can all help accelerate progress across all 40 indicators.

We’ve already seen how these solutions can work. For example, supportive policies — particularly substantial subsidies to build out charging infrastructure and replace city buses with electric buses in China, — spurred dramatic increases in global electric bus sales, which grew from just 2% of sales in 2013 to 44% in 2021. And following devastating fires in Indonesia, a portfolio of government actions — from a moratorium on development in primary forests and peatlands to the creation of an agency dedicated to restoration — helped reduce rates of primary forest loss since 2017 and restore roughly 300,000 hectares of peatlands in 2021 alone.

These bright spots show us what’s possible when leaders across government, civil society and the private sector deploy the many tools at their disposal to accelerate systemwide transformations. To do otherwise would be unthinkable — robbing both current and future generations of their health and prosperity.

Links

Stay informed

Subscribe to our newsletter