The faster fossil gas leaves our energy systems, the better it will be for the climate

Russia’s invasion of Ukraine is a provocation for global change. Intensifying efforts to reduce the demand for fossil gas is the right response to deal simultaneously with both the climate and Russia/Ukraine crises.

CAT Blog

We are now within the critical decade for climate action - by the end of this decade, global emissions must be cut in half from their current levels to keep the Paris Agreement’s 1.5°C temperature goal alive.

While there is a growing consensus that global coal use must decline sharply this decade, governments and companies continue to wrongly claim that fossil gas would be a “bridge fuel”, and could viably remain part of a climate-friendly energy system for decades to come.

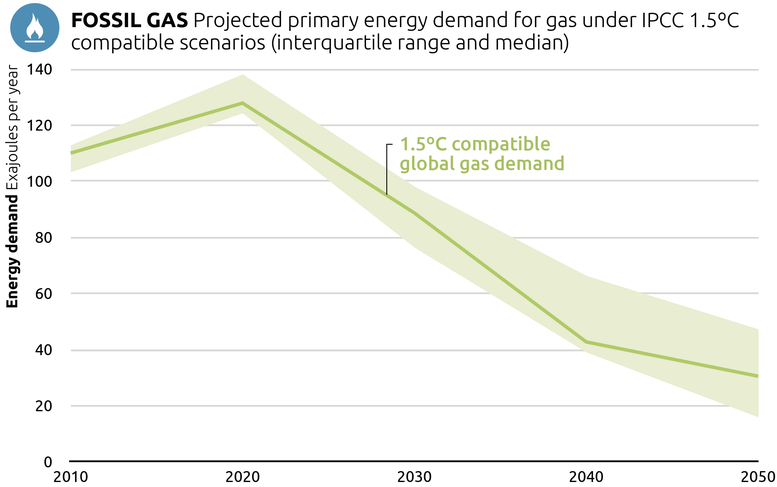

The set of 1.5°C-compatible modelled emissions pathways, including those from the latest report from the Intergovernmental Panel on Climate Change, shows that under most scenarios, total unabated natural gas consumption declines by a third between 2020 and 2030, and even further in the coming decades. This puts any additional fossil gas infrastructure that usually has a long lifetime at great risk of becoming stranded assets.

Figure 1: Total unabated fossil gas use in 1.5°C scenarios from the IPCC Special Report on 1.5°C

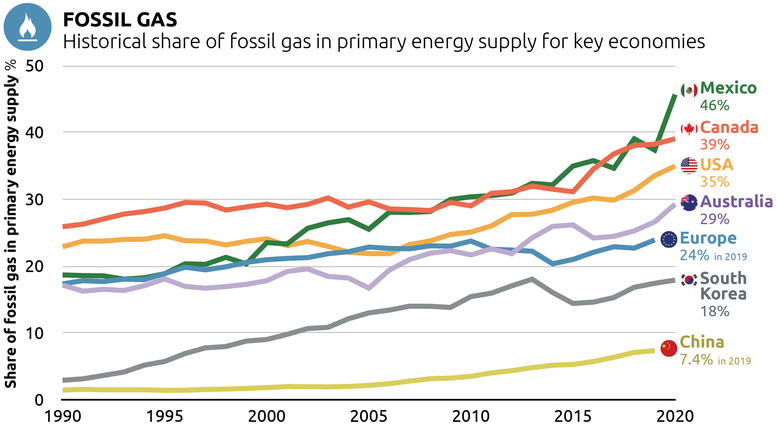

Despite the clear message that total gas demand should already be in decline its use in many economies continues to increase. Since 2015, a total of 14 G20 countries have seen an upward trend in gas’s share of primary energy supply, with particularly steep rises seen in North America (Figure 2).

Depicting sectoral data and comparing across countries, as shown below, is possible on the Climate Action Tracker’s Data Portal, with the corresponding data also available to download.

Figure 2: Share of natural gas in primary energy supply from 1990 to 2020. Source: CAT data portal, based on data from IEA World Energy Balances

The EU has seen the share of gas in primary energy reach an all-time high in 2020 of almost 25%. Much of the gas consumed in Europe is supplied by Russia and, in response to Russia’s invasion of Ukraine, the EU has announced a suite of measures to reduce demand for Russian natural gas this year.

It has also recently announced new measures that go beyond those in its ‘Fit for 55’ policy suite, itself projected to reduce EU gas consumption by 30% by 2030. Given the EU’s self-proclaimed role as a global leader on climate action, and the strong impetus now to rapidly scale down its gas demand, further strengthening its proposed measures would set a strong example.

A greater focus on energy efficiency gains and electrification, particularly through faster adoption of heat pumps and increased funding for building envelope upgrades, would help bring gas demand down more steeply and substantiate the EU’s climate credentials.

Such measures would also help to build badly needed momentum in decarbonising the buildings sector, a sector that has lagged behind others in achieving emissions reductions. IEA has released a 10-Point Plan for decreasing EU’s reliance on Russian gas, which could lead to a reduction of gas consumption by one third over the next year. The Climate Action Tracker (CAT) also provides suggestions on how to decrease fossil energy use, for example in the power, buildings and industry sectors.

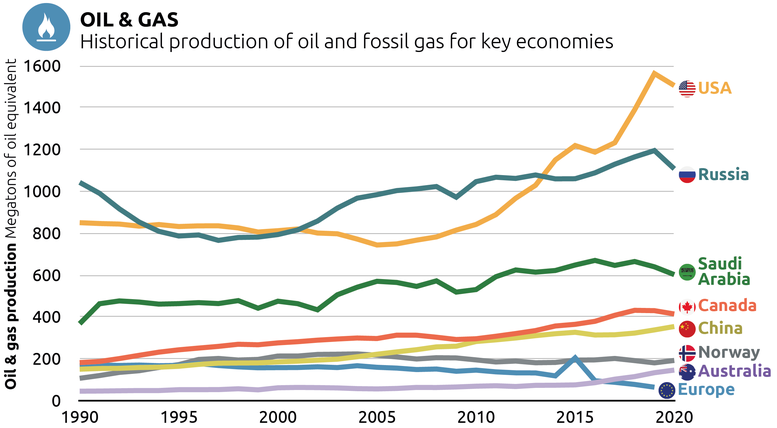

In the EU, where gas consumption has been increasing since 2014, gas production reached a peak in the 90s and has been declining ever since. In fact, the largest gas consumers in the EU - Germany and Italy - barely produce any gas. China is also increasing its gas consumption faster than its production can keep up.

Fossil gas production is largely concentrated in two countries - Russia and the US - who together produce about 40% of dry natural gas. Other producers in the Top-10 are Iran, Canada, Qatar, China, Norway, Saudi Arabia, Australia, and Algeria.

Some countries have increased their production in the last decade, for example USA and Australia (Figure 3). Most gas producers see the export of fossil gas as an important source of income for their economies. The US, for example, is betting on exporting large amounts of carbon-intensive fracking gas through LNG terminals, and increasingly to Europe in the face of Russia’s invasion of Ukraine.

Liquified natural gas (LNG) is a particularly carbon intensive fuel source, and taking into account its lifecycle emissions, may have a greater greenhouse gas footprint than coal fired generation when used for power production. LNG exports have grown rapidly to the point where emissions from LNG supply and end use approached about 17% of natural gas greenhouse gas emissions in 2020 and accounted for about 12% of total gas use globally in that year. Because of its carbon intensity the International Energy agency's Net Zero Emissions road map projects a rapid collapse in the trade of this commodity if the world implements the Paris Agreement. The top two exporters at present are Australia and Qatar.

Figure 3: Oil and gas production in select countries from 1990 to 2020. Source: CAT data portal, based on IEA World Energy Balances

Naturally, the differences in production and consumption of different countries lead to a critical role for fossil gas in international trade, and geopolitical interdependencies.

Relying on fossil gas as a source of energy or income carries multiple societal, economic and environmental risks, most importantly:

- Additional fossil fuel infrastructure risks locking-in high-carbon pathways and stranded assets. The technical life expectancy of gas pipelines, LNG terminals and power plants span several decades, while repurposing LNG terminals for green hydrogen may not be possible. 1.5°C scenarios show that a step change in gas consumption and production is now needed, putting any such investments at great risk.

- In many developing countries the production of fossil fuels has NOT led to an improvement in their populations’ wellbeing, but often worsened inequalities and dependencies on foreign investments. The CAT is currently looking into the role of fossil gas in Africa and will release a report on this topic soon.

- Fossil energy and resulting interdependencies are strongly interlinked with geopolitics, with the Russian invasion of Ukraine being a clear example. These linkages should also be considered when thinking about the potential role of green hydrogen in the future.

- Extraction and use of natural gas comes with substantial threats to the environment and communities beyond greenhouse gas emissions, for example local pollution, water scarcity and, in the case of fracking, risks of earthquakes.

- Renewable energy is as cheap as ever, and large capacities can be built at lower cost than other energy options. Renewable energy systems can support decentralised and flexible energy systems much better than large scale fossil infrastructure. Even without governments pushing towards long-term decarbonisation, renewables will out-compete gas, and large parts of the fossil gas infrastructure are at risk of being stranded.

Stay informed

Subscribe to our newsletter