Natural gas in Africa: Why fossil fuels cannot sustainably meet the continent’s growing energy demand

Attachments

Natural gas is on the rise globally & in Africa

Fossil fuel use is on the rise, with 70% of the increase in fossil CO2 emissions projected to come from natural gas by 2030 if current policies are not strengthened to align with the Paris Agreement goal to limit global warming to 1.5°C.

To meet the objectives of the Paris Agreement:

- No new investments should be made into natural gas exploration and production.

- Unabated gas-fired power generation needs to be phased out by 2050 globally, and in many countries by 2040.

- Total gas demand would need to decrease by 21%–61% from 2020 levels by 2050.

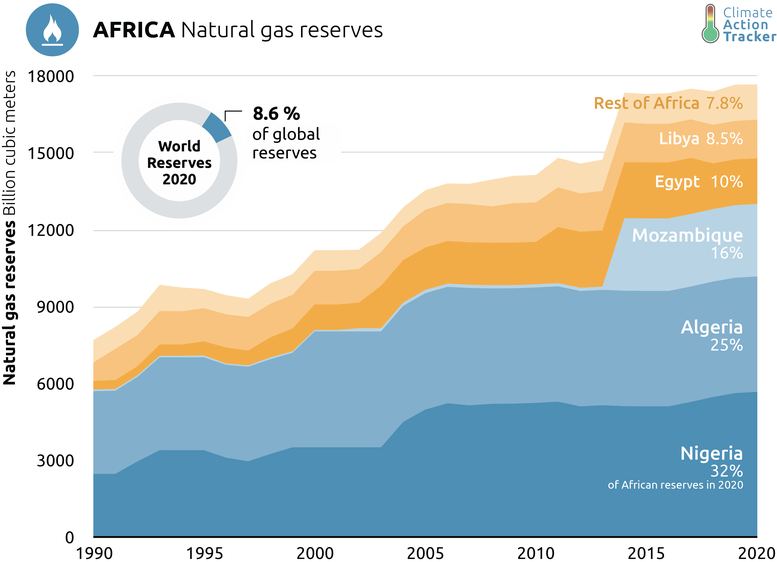

Africa, like most parts of the world, has plans to significantly expand natural gas production and consumption. This is likely to drive up currently lower emission levels on the continent. Africa is home to nearly 9% of the world’s gas reserves and produces around 6% of global natural gas.

The risks of relying on natural gas are ever more apparent

- The current natural gas infrastructure already supplies the volumes required globally, and any addition is at risk of becoming a stranded asset.

- Development strategies that rely on natural gas production and exports are risky, as the world is transitioning to zero emissions and future gas demand is subject to large uncertainties. Jobs in the fossil fuel industry are not secure: employment is estimated to fall by around 75% by 2050 under a well below 2°C scenario.

- Exploiting oil and gas resources has even proven to be counterproductive to development objectives in some instances: fossil fuel exporters in Africa experience slower economic growth compared to other countries on the continent.

Transitioning to renewable energy has multiple benefits

- Africa has vast renewable energy resources that can supply the continent’s growing energy demand. These resources could also support new export value chains, for example in the form of renewable electricity or green hydrogen.

- Wind and solar energy are already the cheapest sources of electricity—with new installations becoming increasingly competitive even when replacing existing fossil fuel plants.

Climate finance is needed to make this transition happen

- Developed countries, international companies and multilateral financial institutions need to urgently stop financing fossil fuels globally.

- In parallel, developed countries need to significantly ramp up international climate finance and support for the energy transitionin developing countries.

Egypt

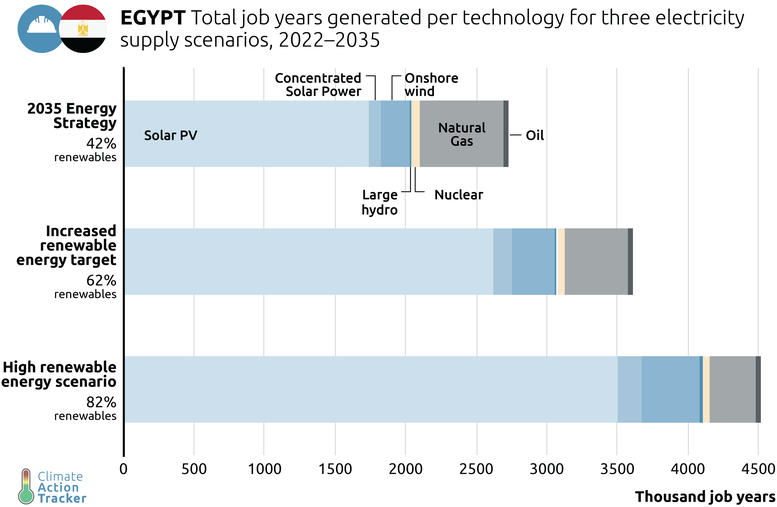

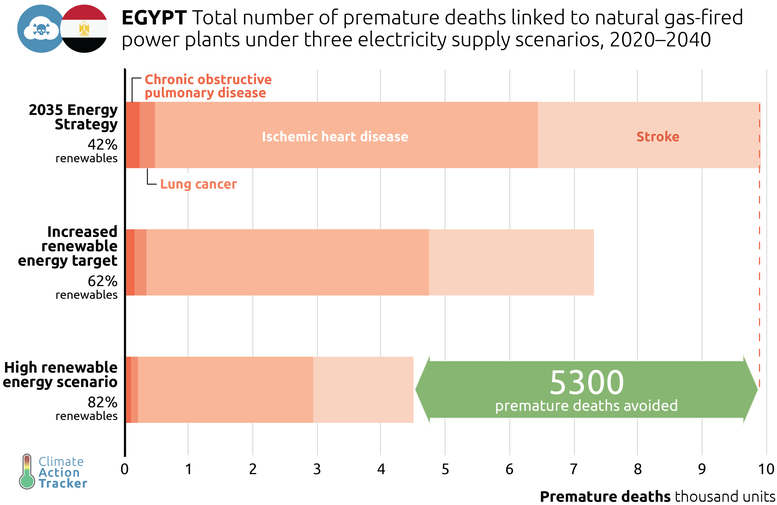

Egypt is responsible for over a third of total natural gas consumption in Africa. Close to 70% of its gas is used for electricity production. The government has plans to expand natural gas production and to increase natural gas infrastructure across many sectors, including electricity and transport. Egypt does not need to rely on gas to meet its energy needs, as it has abundant and cost-effective renewable energy resources. Increasing renewable energy in the power sector would lead to multiple benefits, including higher employment generation and reduced air pollution. It could also support Egypt’s ambition to become a net electricity exporter. Our analysis shows that a high share of renewables in the power sector (82% in 2035) could create an additional 1.8 million jobs compared to the government’s 2035 Energy Strategy — translating to nearly 130,000 additional jobs per year. A high share of renewable energy (82% by 2035) could also avoid more than 5,300 premature deaths linked to air pollution from natural gas in the next two decades compared to the 2035 Energy Strategy, which foresees over 50% of electricity to be generated with gas in 2035.

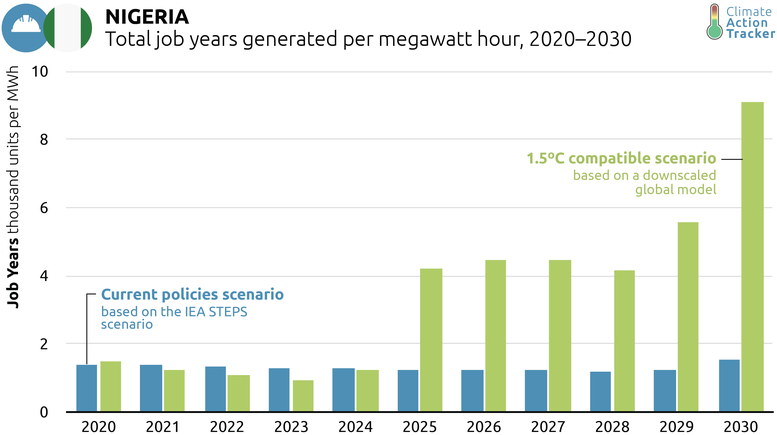

Nigeria

A majority of Nigerians rely on traditional biomass, with very limited access to electricity and clean cooking. Even when connected to the grid, Nigerians face frequent and prolonged blackouts, often due to gas supply shortages for power plants. The government has declared this decade to be the “Decade of Gas”, with plans to continue investing in gas infrastructure, which brings risks of stranded assets and locking the energy sector into carbon intensive infrastructure, when it should be investing in ever-cheaper renewables. Nigeria is currently the 17th largest natural gas producer in the world, although it has struggled to attract investment in recent years. While Nigeria has made progress reducing gas flaring, this is still a significant source of emissions, along with fugitive methane emissions in the gas supply chain. Our analysis shows that if Nigeria was to align its electricity sector to 1.5°C-compatible pathways, and increase its share of renewables, Nigeria could create, on average, more than 3,400 job years per MWh per year compared to the current gas-based strategy, creating only about 1,300 annual job years per MWh.

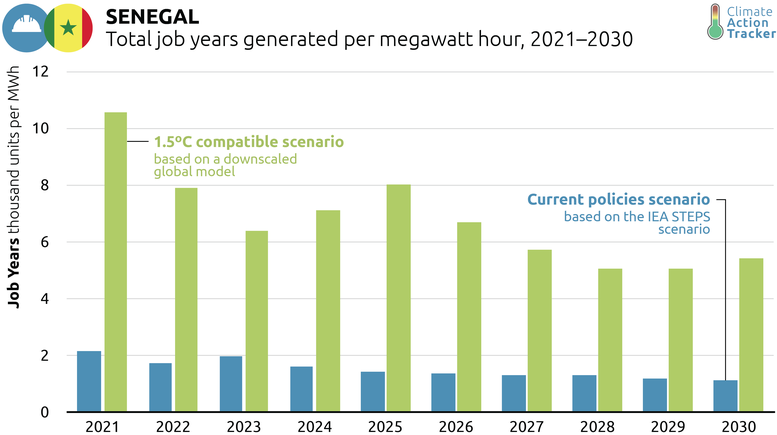

Senegal

Following significant oil and gas discoveries, Senegal has adopted a Gas-to-Power Strategy to shift from a power system dependent on expensive oil imports to one dependent on gas. However, for Senegal to exploit its gas reserves, it needs to build significant infrastructure that would be at risk of becoming stranded assets as the world moves to net zero emissions.Further, for new markets to attract finance for gas infrastructure, countries often have to agree to take on much of the risk through unfavourable agreements such as “take-or-pay” schemes. Finances planned for gas expansion could be channelled to renewables, which are cheaper and could provide sustainable jobs, increase access to energy, and improve local air quality. Our analysis shows that if Senegal does not pursue natural gas and increases renewable energy in the power mix in line with 1.5°C pathways, it could create on average 6,700 job years per MWh annually compared to 1,500 job years under current policies from 2021 to 2030.

More materials

Additional analysis from Climate Action Tracker on the countries covered above is available via the links below.

Stay informed

Subscribe to our newsletter