New Zealand

Pledges And Targets

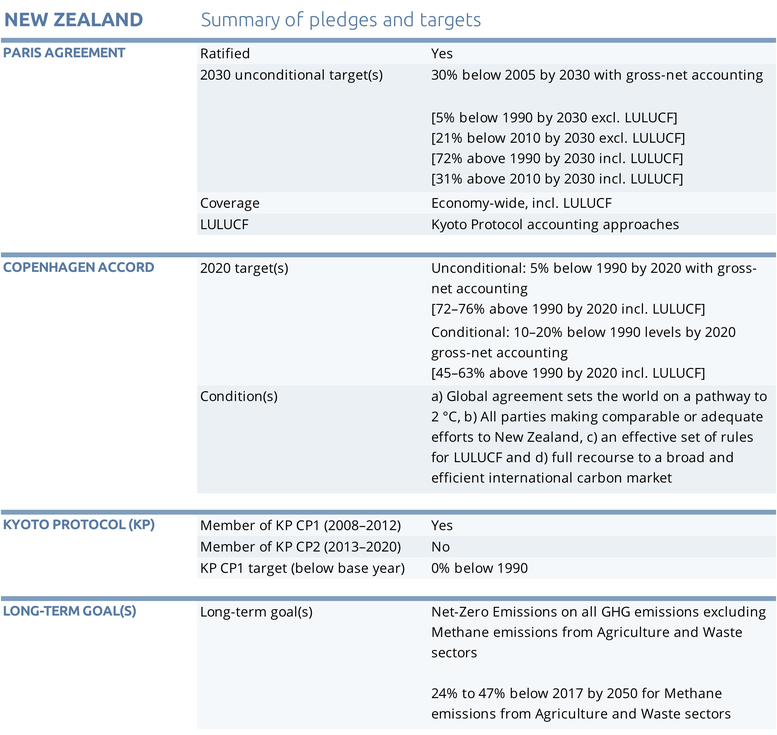

Summary table

Paris Agreement targets

New Zealand’s NDC contains an emissions reduction target of 30% reduction below 2005 levels by 2030 (New Zealand Government, 2016a). We estimate that the emission level excluding LULUCF targeted by the NDC is 62 MtCO2e in 2030.

New Zealand’s LULUCF accounting approach remains unclear: the statement that the 30% reduction below 2005 levels is equivalent to a reduction of 11% from 1990 levels, confirmed in the Third Biennial Report (Ministry for the Environment, 2017b), suggests that New Zealand is planning to exclude LULUCF emissions in the base year but account for them in the target year, which is known as a “gross-net” approach (see Assumptions section). The use of this approach raises many questions in terms of the environmental integrity of the target (Rocha et al., 2015). For indicative purposes, we also show the emissions levels that the NDC target would represent if using a net-net approach (42 MtCO2e in 2030).

Further uncertainty around the emissions levels that New Zealand could have in 2030 without missing its NDC target is added by the New Zealand Government’s statement that it is planning to meet its NDC target through a combination of domestic emissions reductions, participation in international markets, and removal of carbon dioxide by forests (Ministry for the Environment, 2017b). In the Zero-Carbon Act recently adopted, the government could use international market credits, however notes that it would only do so as a last resort. The Climate Commission, which will be set up under the Act, has been tasked with setting a limit on emission reduction credits that can be purchased from overseas mitigation actions.

We have further analysed the implications of New Zealand seeking to continue to apply a Kyoto-type accounting system as described in the NDC (New Zealand Government, 2015), despite having not signed up to the second commitment period (CP2), and to carry over surplus units from CP2 to the post-2020 period, even though their ability to do so in the Paris Agreement has been neither verified nor prohibited.

Using the information about Kyoto Protocol forestry activity credits in the CP2 provided in the 2018 net position update, we estimate that if New Zealand were able to apply its preferred accounting rules, its nominal 30% reduction from 2005 levels by 2030 pledge could, in reality, enable an increase in GHG emissions excluding LULUCF to 79MtCO2e, or 5% below 2005 levels by 2030. More clarity around the intentions of the government around the surplus units in the post-2020 period would be needed for an updated estimate of the impacts of the suggested approaches in the NDC target. For a more detailed description of the methodology and assumptions used in previous reports to estimate the potential impacts of a Kyoto-type accounting system for New Zealand’s NDC target see our 2015 country report.

2020 Pledge and Kyoto target

New Zealand's Kyoto Protocol target for the first commitment period (CP1) (2008–2012) was to return its GHG emissions excl. LULUCF to 1990 levels (QELRO of 100% of 1990 emissions).

Under the Kyoto Protocol accounting rules applicable to New Zealand in CP1, certain land-use change and forestry activities provided credits that were added to allowed GHG emissions, excl. LULUCF, to rise during this commitment period. In CP1, these activities resulted in extra emission allowances for New Zealand of, on average, 14 MtCO2e per year (equivalent to about 23% of base year emissions in 1990). As a consequence of its large volume of LULUCF credits, New Zealand had a substantial surplus of unused emission units at the end of CP1. In addition to LULUCF credits, New Zealand used a large amount of Emissions reduction Units (ERUs) of unclear environmental integrity to meet a significant part of its CP1 target (Sustainability Council of New Zealand, 2014).

As explained below, New Zealand proposes to use these surplus emission allowances from CP1, which are derived in part from Kyoto LULUCF credits and acquired emission units from other countries, to meet its 2020 reduction target under the Convention.

In 2013 New Zealand put forward an unconditional pledge to reduce GHG emissions excluding LULUCF by 5% below 1990 levels by 2020. This pledge is complemented by an earlier conditional pledge from 2009 to reduce emissions 10–20% below 1990 levels by 2020 (Government of New Zealand, 2013). The government provided further details, including its plans to apply Kyoto-type accounting rules governing the second commitment period (2013–2020).

New Zealand’s unusual decision to adhere to the Kyoto rules and subsequently ratifying the Doha amendments without signing up to the CP2 raises a number of legal issues, as the Protocol provides certain benefits only to Parties that have emission reduction commitments for CP2.1 If New Zealand were able to apply its preferred accounting rules, and use these units to offset its fossil fuel and industrial emissions, we calculate that its nominal 5% reduction from 1990 levels by 2020 pledge (around 64 MtCO2e in 2020) could, in reality, enable an increase in GHG emissions excluding LULUCF to 95–108 MtCO2e, or 44–64% above 1990 levels by 2020.

Its 2018 net position update shows that New Zealand is projected to meet its unconditional target to reduce emissions to 5% below 1990 levels by 2020 with a surplus of 92.4 million units, by making use of 31.4 million available units from CP1 (out of a total surplus of 123.7 million units) to meet its 2020 target, where one unit represents one tonne of greenhouse gas emissions as carbon dioxide equivalent (tCO2e) (Ministry for the Environment, 2018a).2

In addition to the use of Kyoto rules for meeting its 2020 target, New Zealand is considering a completely new type of LULUCF accounting rules, which include the accounting of an “average carbon stock” for any new forests planted. These alternative accounting rules could be used to avoid large future carbon liability hits when plantation forests are harvested (Young & Simmons, 2016). The set of rules was described in further detail under the ETS consultation (Forestry New Zealand, 2018) and is currently open to consultations under the Proposed Climate Change Forestry Regulations changes until December 2019 (Ministry of Primary Industries - New Zealand, 2019a). However, the lack of transparency around them means their effect on overall emissions is as yet unclear.

1 | The Kyoto rules New Zealand seeks to apply, broadly relate to: (i) The carry over of surplus emission units and allowances from the first commitment period; (ii) The ability to generate LULUCF credits during the CP2 period; (iii) The ability to purchase and sell Kyoto emission units from other Kyoto Parties during CP2; and (iv) Provisions relating to the carryover of any surplus from earlier commitment periods to the post-2020 period.

2 | The 2019 net position update shows a surplus of 96.8 million units, meaning that 27 million units would be used to meet its 2020 target (Ministry for the Environment, 2019). Future updates of the CAT will incorporate these figures.

Long-term goal

The Zero Carbon Act recently adopted proposes to achieve net zero emissions of all greenhouse gases, except for methane emissions from agriculture and waste (which it terms ‘biogenic methane’) by 2050 (Parliamentary Counsel Office of New Zealand, 2019). These methane emissions represent about 40% of New Zealand’s emissions today (Government of New Zealand, 2019a) and should be reduced by at least 24-47% below 2017 levels by 2050.

Previous analysis found that a net zero target for all domestic GHG emissions in 2050 could be consistent with the Paris Agreement (Hare, Schleussner, Schaeffer, & Nauels, 2018). An overwhelming majority of the 15,000 submissions received (91%) during the consultation process for this act had supported achieving net zero emissions for all greenhouse gases (Ministry for the Environment, 2018b).

The independent Climate Commission, established under the Act, will advise on five-yearly carbon budgets, future revisions of the 2050 target, the use of international credits and the extent to which emissions may be banked or borrowed from one budget to the next. The comparable climate advisory body in the UK unequivocally advised its government in February not to bank emissions from that country’s second carbon budget (UK Committee on Climate Change, 2019). New Zealand’s Climate Change Minister has called the practice “dodgy accounting” (Doherty, 2018). The Bill has been passed into law on November 6th, 2019 (Parliamentary Counsel Office of New Zealand, 2019).

The Act would allow the government to use international market credits; however, only as a last resort. The Climate Commission has been tasked with setting a limit on emission reduction credits that can be purchased from overseas mitigation actions.

The CAT provides an assessment of the 2050 target. Based on LULUCF sector emissions projections for 2050, published in Regulatory Impact Statement from the Ministry of Environment, we estimate the 2050 target translates to emissions levels of between 36-51 MtCO2eq in 2050 (Ministry of the Environment, 2019).

However, similar to the 2020 and 2030 targets, uncertainty is added by the accounting approaches suggested by New Zealand for the achievement of this target. The new act states that “Emissions budgets must be met, as far as possible, through domestic emissions reductions and domestic removals.” And that “offshore mitigation may be used if there has been a significant change of circumstance” (Parliamentary Counsel Office of New Zealand, 2019).

The Government has stated that “the 2050 target is based on New Zealand’s net GHG emissions and will take into account any removals or emissions arising from afforestation or deforestation since 1990 consistent with the Kyoto Protocol under the United Nations Convention Framework rules on climate change”(Government of New Zealand, 2011). The NDC text, as well as the 7th National Communication and 3rd Biennial Report, reiterate New Zealand’s intent to meet this target making use of Kyoto accounting rules.

The assumptions on sequestration and methodology accounting therefore have a huge impact on the expected remaining emissions by 2050. A new LULUCF emissions accounting methodology is under a consultation process until December 2020 under the proposed Climate Change Forestry Regulations changes and proposes to use the average accounting. This means that “forest owners who use the new 'averaging accounting' option will no longer need to surrender New-Zealand Units (NZUs) when they harvest (if they replant)”. This however will not apply to forest post-1989 already registered before 2019 under the Emissions Trading Scheme (Ministry of Primary Industries - New Zealand, 2019b).

The 2050 Long-Term Target has been quantified using projected LULUCFs emissions for 2050 based on the latest target analysis taken from four different scenarios presented in the Regulatory Impact Statement (Ministry of the Environment, 2019). The four scenarios model a split target based on an emissions reduction of biogenic methane, together with a net-zero target by 2050 of all greenhouse gases emissions excluding biogenic methane. The lower end is based on the higher sink from the estimated LULUCFs projections added to the remaining biogenic methane emissions after a 47% emissions reduction by 2050. The higher end is based on the lowest sink from the estimated LULUCFs emissions projections added to the remaining biogenic methane emissions after a 24% emissions reduction by 2050.

The Productivity Commission has undertaken modelling to examine pathways from current levels to two alternative long-term targets: a 60% reduction from 1990 levels (around 26 MtCO2e including LULUCF) and a more ambitious target of net-zero emissions by 2050. The main conclusion of the modelling exercise is that under all the scenarios modelled both targets are feasible, but immediate action is needed (Productivity Commission, 2018).

The findings of the Productivity Commission confirm previous results by other modelling groups that conclude that in order to be on a trajectory toward emission-neutrality around mid-century, substantial strengthened action in the agriculture and forestry sectors is needed in addition to efforts to decarbonise the energy system further (Vivid Economics, 2017).

Further analysis

Latest publications

Stay informed

Subscribe to our newsletter