Russian Federation

Policies & action

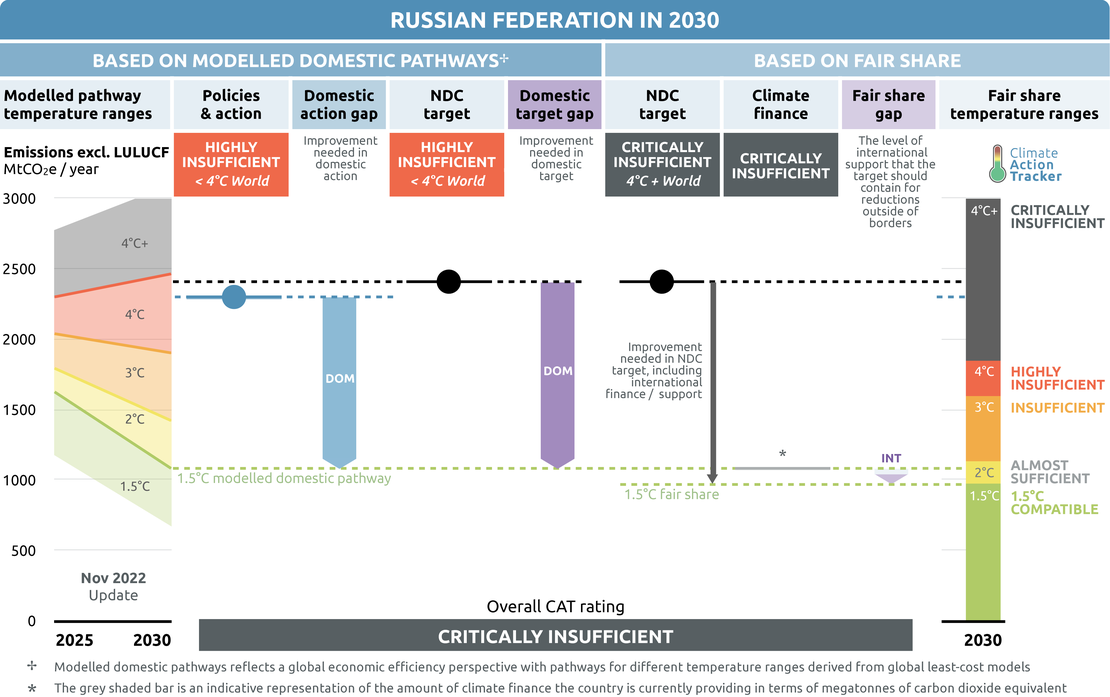

The CAT rates Russia’s current policies as “Highly insufficient” when compared to modelled domestic pathways. The “Highly insufficient” rating indicates that Russia’s policies and action in 2030 lead to rising, rather than falling, emissions and are not at all consistent with limiting warming to 1.5°C. If all countries were to follow Russia’s approach, warming could reach over 3°C and up to 4°C.

We do not observe any substantial change in Russia’s efforts to tackle climate change. Its few relevant policies are unambitious or have unclear expected effect on emissions. Russia's existing policies indicate no real commitment to curb emissions.

In June 2021, Russia adopted its heavily watered-down climate bill that, unlike the original iteration of the legislation, does not enforce emissions quotas nor impose penalties on large GHG emitters. Instead, its main provision simply requires companies to report their emissions from 2024. Considerable uncertainty remains in Russia’s renewable energy sector. Russia has no targets in place beyond its unambitious non-hydro generation target of 4.5% by 2024, which it will not meet.

In the transport sector, Russia has taken steps to promote the production and purchase of EVs. As part of its Transport Strategy Until 2030, Russia has also proposed measures to reduce transport emissions through low-carbon infrastructure and alternative fuels.

Though the CAT’s qualitative analysis does touch on some of the near-term implications of Russia’s illegal invasion of Ukraine, we have not quantified the long-term effect of the war, nor its numerous implications. The projections do not yet include, for example decrease in fossil fuel exports or potential economic decline in Russia.

Further information on how the CAT rates countries (against modelled domestic pathways and fair share) can be found here.

Policy overview

Under current policies, Russia’s economy-wide emissions are expected to continue rising to 2030, when they should be rapidly declining. According to our latest estimates, currently implemented policies would lead to emissions between 2,285 and 2,314 MtCO2e in 2030 (excluding LULUCF). This represents a 27–28% decrease in emissions below 1990 levels, a level that is below the unambitious NDC target for 2030, which amounts to a 24% decrease below 1990 levels (excluding LULUCF).

Recent legislative developments

In August 2021, Russia approved the Concept for the Development of Electric Vehicle Production which set a target of EVs constituting at least 10% of domestically produced vehicles by 2030 (Russian Federation, 2021b). In addition to promoting EV production, Russia plans to provide subsidies covering up to 25% of the price of domestically produced EVs to stimulate demand (Reuters, 2021).

In September 2021, Russia approved, for the first time, a law aimed at regulating emissions though it is a significantly watered-down version with very limited impact on Russia’s future emissions (The Moscow Times, 2021). Initially, this legislation aimed at limiting emissions by assigning quotas for Russia’s largest companies, a new national carbon trading system and penalties for companies who exceeded their quotas (The Moscow Times, 2019). However, due to resistance from the Russian Union of Industrialists and Entrepreneurs, all of these measures, except for the requirement of companies to report their emissions from 2024, were removed (The Moscow Times, 2019).

In November 2021, Russia released the Transport Strategy Until 2030. The strategy includes measures for energy-efficient or electric vehicles, low-carbon infrastructure, and alternative fuels intended to reduce transport emissions by 1.2% relative to total emissions in 2017 by 2030 (Russian Federation, 2021c) .

The EU’s proposed Carbon Border Adjustment Mechanism (CBAM), which seeks to place a levy on carbon intensive goods, is likely to substantially affect Russian exports, with a recent study estimating Russia were to face higher costs from the proposed mechanism than any other country (Assous et al., 2021). Prior to Russia’s illegal invasion of Ukraine, the EU was Russia’s largest trading partner. It remains to be seen how Russia-EU trade flows will develop in the coming years, but without implementing substantial measures to decarbonise the Russian industry sector, the economic costs of any future trade with the EU are likely to climb over time.

While 2021 saw some positive developments, in 2022 Russia has rolled back some environmental protection and emission reductions measures, for example, as of early May, Russian car makers no longer have to adhere to pollution control standards used by the European Union (Zelenaya, 2022).

Sectoral pledges

In Glasgow, a number of sectoral initiatives were launched to accelerate climate action. At most, these initiatives may close the 2030 emissions gap by around 9% - or 2.2 GtCO2e, though assessing what is new and what is already covered by existing NDC targets is challenging.

For methane, signatories agreed to cut emissions in all sectors by 30% globally over the next decade. The coal exit initiative seeks to transition away from unabated coal power by the 2030s or 2040s and to cease building new coal plants. Signatories of the 100% EVs declaration agreed that 100% of new car and van sales in 2040 should be electric vehicles, 2035 for leading markets. On forests, leaders agreed “to halt and reverse forest loss and land degradation by 2030”. The Beyond Oil & Gas Alliance (BOGA) seeks to facilitate a managed phase out of oil and gas production.

NDCs should be updated to include these sectoral initiatives, if they aren’t already covered by existing NDC targets. As with all targets, implementation of the necessary policies and measures is critical to ensuring that these sectoral objectives are actually achieved.

| Signed? | Included in NDC? | Taking action to achieve? | |

|---|---|---|---|

| Methane | No | N/A | N/A |

| Coal Exit | No | N/A | N/A |

| Electric vehicles | No | N/A | N/A |

| Forestry | Yes | No | Not clear |

| Beyond Oil and Gas Alliance | No | N/A | N/A |

- Methane pledge: Russia has not adopted the methane pledge. Methane, predominately from the energy sector, constituted 15% of Russia’s total GHG emissions (excl. LULUCF) in 2020. Russia does not propose quantifiable mitigation measures directed at reducing methane in its NDC.

- Coal exit: Russia has not adopted the coal exit. Russia does not plan to phase out coal. In 2021, Russia was the third largest coal exporter (17.9 % of global exports) in the world (BP, 2022).

- 100% EVs: Russia has not adopted the declaration on accelerating the transition to 100% zero emission cars and vans from COP26. Russia has set the target of EVs constituting at least 10% of domestically produced vehicles by 2030 and plans to provide subsidies covering up to 25% of the price of domestically produced EVs in order to stimulate demand.

- Forestry: Russia signed the Leaders' declaration on forest and land use at COP26, but this is not included in its NDC. Please see the forestry section below for more details on why Russia places significance on its LULUCF sector as a net carbon sink.

- Beyond oil and gas: Russia is not a member of BOGA. In 2021, Russia was the world’s largest exporter of fossil gas—with 23.6% of global exports—and the second largest exporter of oil (12.3% of total) (BP, 2022).

Energy supply

Russia’s illegal and unprovoked invasion of Ukraine has generated price shocks that have reverberated through global energy markets.

Russia’s continued reliance on fossil fuel energy and export revenues (contributing to 45% of Russia’s federal budget in 2021) poses a significant challenge to the Russian economy, now exacerbated by the sanctions placed on Russia by other governments in response to the Russian invasion of Ukraine. It also adds to the impacts Russia faces from the changing climate (IEA, 2022b).

In 2021, Russia was the world’s largest exporter of fossil gas—with 23.6% of global exports—and the second largest exporter of oil (12.3% of total) (BP, 2022). Since Russia invaded Ukraine on 24 February 2022, the global demand for Russian fossil fuels has declined as many governments, including the EU, have imposed economic sanctions (Myllyvirta et al., 2022).

The EU has set a partial embargo on Russian oil imports by the end of 2022, and on Russian oil products by the end of February, and it ended Russian coal imports in August (European Council, 2022a, 2022b; Myllyvirta et al., 2022). These sanctions will have a significant impact on the Russian economy as well as globally. For example, in the case of the EU, Russian fossil gas imports made up almost 40% of total EU consumption of fossil gas, Russian oil imports contributed to 25% of total EU oil imports, and 20% of the EU’s coal consumption in 2021 (BP, 2022).

These developments, combined with the banking sector’s increasingly unwillingness to finance fossil fuel projects seen as contributing to climate change, do not bode well for Russia’s plans to expand fossil fuel exports and will have substantial negative implications for Russia’s public finances (Associated Press, 2020; Ekblom, 2019; IEA, 2022a; Russian Federation, 2020a).

Estimating the trajectory of GHG emissions in the energy sector in the near future is difficult due to the major changes. The CAT projections therefore do not yet include, for example decrease in fossil fuel exports or potential economic decline in Russia, which would have much larger impact on emissions compared to any policies currently implemented.

In 2020, Russia committed to reducing its energy intensity of GDP by 30% by 2030 (Ministry of Economic Development of Russia, 2020). A 30% reduction from Russia’s 2019 energy intensity of 7.6 TJ per million USD 2015 GDP would put Russia’s energy intensity at 5.3 in 2030, which is still higher than the G20 average of 4.4 in 2019 (Climate Transparency, 2021).

With Russia’s energy sector accounting for nearly 80% of all emissions (excl. LULUCF) in 2020 (Russian Federation, 2022b), Russia should focus on further increasing its renewable energy generation to move towards a 1.5°C compatible pathway, avoid technology lock-in, and improve energy security, instead of relying on increasing its LULUCF sink to negate these emissions (see Forestry section below).

Energy Strategy to 2035

In June 2020, Russia adopted its long-delayed Energy Strategy 2035, confirming Russia’s intention to heavily support its fossil fuel energy sectors beyond the next decade (Russian Federation, 2020a). The strategy suggests that Russia will continue to sell oil, coal, and gas to the rest of the world, while everything that hinders this goal is considered to be a threat and a challenge (Zhelenin, 2020). This stands in blatant contradiction to the IEA’s recent finding that no investments in new oil and gas extraction projects should occur beyond 2021 (IEA, 2021a).

The strategy assumes that “until 2035 fossil fuels will continue to form the basis of the global energy sector with a gradual increase in the share of energy based on the use of renewable sources” (Russian Federation, 2020a). These assumptions underpin both scenarios outlined in the document, and accordingly, there is little focus on renewable energy technologies, and no long-term targeted increase in generation from this sector.

The intention behind Russia’s energy strategy has been signalled by recent government decisions supportive of fossil fuel companies. In 2021, Novatek, Russia’s largest independent fossil gas producer, requested access to more gas resources to support the construction of its third large-scale gas facility since 2017 (Persily, 2021).

The gas deposits Novatek wanted access to were within the boundaries of a nature reserve where industrial activities are prohibited, but after reportedly requesting that the Kremlin instruct the regional government to adjust the boundaries to allow the facility to proceed, the regional government obliged in May 2021 and the boundaries were changed (Persily, 2021). In addition, President Putin in August 2021 ordered the introduction of amendments designed to allow Russian Railways and coal miners to agree on expanding eastward coal exports (The Coal Hub, 2021).

Other key elements of Russia’s energy strategy include advocating for the development of clean-coal technology and for minimising the flaring of fossil gas as key measures to address climate change in the energy sector.

Fossil gas and flaring emissions

Fossil gas made up 54% of Russia’s total primary energy supply in 2020 and this is projected to remain consistent under stated policies through 2030 (IEA, 2021b). Russia’s Energy Strategy to 2035 forecasts a 5-9% growth in fuel production by 2024 compared to 2018, including at least a doubling in the production of liquefied natural gas (LNG) (Russian Federation, 2020a, 2020b). This continued investment in the production of and reliance on fossil gas is problematic, as gas does not have a place in long-term 1.5°C compatible scenarios and still produces significant GHG emissions in both its production and consumption (IPCC, 2018).

Despite a stated goal of minimising flaring and the introduction in 2012 of a 5% limit on flaring of gas as a proportion of total production, Russia still struggles to contain gas flaring (Korppoo, 2018; Russian Federation, 2009). In 2015, Russia reached the lowest level of flaring at around 12%, but since then flaring has been increasing and reached 17.4% in 2020 (Reuters Staff, 2021).

Russia’s Energy Strategy to 2035 introduced an even less ambitious target of 10% by 2024 and 5% by 2035 (IEA, 2022a; Russian Federation, 2020a). This target is not quantified because Russia does not appear to be taking steps toward achieving it. In 2021, Russia maintained its position as the world’s largest gas flaring nation by volume (Global Gas Flaring Reduction Partnership (GGFR), 2022). At 25 billion cubic metres, Russia flared about 30% more gas in 2021 than the next highest country, Iraq (Global Gas Flaring Reduction Partnership (GGFR), 2022).

Renewable Energy

Installed renewable power generation capacity sat at approximately 56 GW in 2020, equivalent to 21% of the country’s total power generation capacity, with hydropower representing by far most of the installed renewable energy capacity (52 GW) (IEA, 2021b).

Under stated policy projections, there is a slight upward trend in the share of renewable sources in total primary energy supply from around 3.4% in 2020 to 4.4% by 2030 (IEA, 2021b).

In 2009, Russia established a 4.5% renewable electricity generation target, excluding large hydropower, by 2020 with its Energy Strategy to 2030 (IRENA, 2017). In 2013 this target was revised down to at least 2.5% by 2020 through the State Programme for Energy Efficiency and the Development of the Energy Sector, and the original 4.5% renewable electricity target was pushed back to 2024 (IRENA, 2017).

Russia missed its 2020 target and will not meet it 2024 target, given that in 2021 only 0.47% of Russia’s electricity came from non-hydro renewables (BP, 2022; Proskuryakova, 2022). This extremely low share stands in contrast to the global average of over 10.2% (BP, 2022). The lack of projected progress on increasing uptake of renewable energy in Russia is shown below. The figure includes electricity generation from large hydro.

Share of renewable electricity generation

Transport

Russia’s long-term climate strategy includes a commitment to achieve a modal shift for passenger and freight transport to less carbon intensive modes of transport (Russian Federation, 2022c). In addition to this commitment, Russia also took concrete steps to decarbonise its transport sector.

Electric vehicles (EVs) sales in Russia in 2021 have tripled to 2,254 (Bouckley, 2022). In an attempt to continue a trend of increased EV demand, in August 2021 the government approved an EV concept that targets the construction of 9,400 charging stations and local manufacturing of at least 25,000 EVs by 2024, reaching at least 72,000 charging stations and a 10% EV share of total vehicle manufacturing by 2030 (Kalinin et al., 2021; Russian Federation, 2021b).

However, the current economic sanctions imposed on Russia have limited its ability to import key technological components, such as semiconductors, causing the domestic production of automobiles to plummet because of the shortages (Bogdanova, 2022). Along with measures promoting EV production, the government plans to stimulate demand by providing subsidies covering up to 25% of the price of domestically produced EVs (Reuters, 2021).

In November 2021, Russia released the Transport Strategy Until 2030. The strategy includes measures for energy-efficient or electric vehicles, low-carbon infrastructure, and alternative fuels intended to reduce transport emissions by 1.2% relative to total emissions in 2017 by 2030 (Russian Federation, 2021c). The CAT has not quantified this target. This target is not ambitious enough given the level of decarbonisation expected for key benchmarks in the transport sector (Climate Action Tracker, 2020).

However, there are no measures targeting other areas; there are no plans to phase out sales of fossil fuel passenger cars or heavy duty vehicles, while there are also no fuel efficiency standards in place.

Russia’s land use, land use change and forestry (LULUCF) sector has been a large sink since the mid-1990s, reaching a maximum of -720 MtCO2e in 2010 (36% of total non-LULUCF GHG emissions) (Russian Federation, 2022b). This has since declined to -569 MtCO2e in 2020 (Russian Federation, 2022b). In its recently submitted long-term climate strategy, Russia projects its removals in 2050 to reach -1,200 MtCO2e from -539 MtCO2e in 2030. These removals are projected to be achieved via LULUCF sinks, but there is no information available in the strategy to substantiate such an enormous increase.

In February 2021, Russia’s Environment Ministry announced it would be changing its accounting method for calculating the size of Russia’s forestry sink in its favour, intending to include unmanaged “reserve” forests alongside managed forests in its GHG inventory (Light, 2021). This violates a key element of international climate reporting, with the UN’s IPCC guidelines stating that only managed forests may be included in carbon accounting practices (IPCC, 2006). The Ministry claims that enacting this accounting change could increase absorption by almost 500 MtCO2 annually (Light, 2021). This could partially explain why the LTS assumes Russia’s LULUCF sink will be twice as high in 2050, but no explanation is provided in the LTS.

It would also, assumedly, include the large scale emissions caused by forest fires that have been intensifying in recent years due to unprecedented heat waves in Northern regions, including a record 18.8m ha of forest destroyed in 2021 alone and at least three million hectares in 2022 (The Moscow Times, 2022a, 2022b). Nevertheless, Russia’s Fourth Biennial Report projects a LULUCF sink of -246 MtCO2e in 2030 under a “with measures” scenario or a maximum sink of -509 MtCO2e in 2030 “with additional measures”(Russian Federation, 2019b). A decline in forestry removals would make the government’s 2060 net zero emissions target significantly more difficult to achieve.

Further analysis

Latest publications

Stay informed

Subscribe to our newsletter