Australia

Country summary

Overview

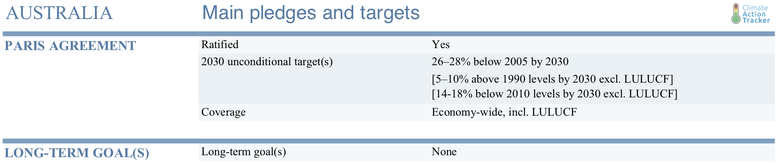

NDC update: In December 2020, Australia recommunicated its NDC. Our analysis of its recommunication is here.

The decline in economic activity in Australia due to the COVID-19 pandemic results in lower greenhouse gas (GHG) emissions projections for 2030, although Australia has not implemented an effective climate policy. The Australian government has initiated a gas-led recovery rather than a green recovery, and has continued to signal its support for the coal industry. The government has shown no intention of updating its Paris Agreement target nor adopting a net-zero emissions target, with the Prime Minister specifically ruling this out. The Government is focusing on what it calls a “technology neutral” approach, which is contradicted by its focus on gas. Renewable energy investments have dropped to 2017 levels due to the uncertainty in government policy direction. There is a lack of climate action, despite rising climate impacts such as the catastrophic bushfires that enveloped several states in late 2019 and early 2020. The CAT rates Australia’s Paris Agreement target as “Insufficient”.

We expect that GHG emissions in financial year 2020 will be 10% to 11% lower than 2019, with an expected economic downturn of 8% to 9%. The two periods of lockdown within parts of Australia to date have temporarily reduced the activity of road users, and transport emissions. April 2020 saw a drop in petroleum consumption, down 12.7% from April 2019. The lockdown measures did not have a substantial impact on electricity sector emissions during the first wave of the pandemic, as mining and mineral processing operations continued.

The Australian government has not initiated a green recovery, instead using the pandemic as a justification to support expansion of the gas industry. The Prime Minister announced the government will invest in the acceleration of gas basin development and also government intervention in the energy market through building a government owned 1 GW gas generation plant, creating confusion and uncertainty for investors. Within days he back peddled on the 1 GW gas generation plant, creating further confusion and uncertainty. The power industry is by and large opposed to this intervention and is focused on renewables and large scale storage to replace the retiring Liddell coal plant in New South Wales.

The government appointed key fossil fuel and mining stakeholders to its national COVID-19 Commission Advisory Board, including a member of the Saudi Aramco Board. Unsurprisingly the Commission supports a gas-led recovery recommending the government underwrites gas pipelines, and increases both domestic gas supply and subsidies for gas-fired power generation. The government has ignored the opportunities from green recovery, in particular an accelerated transition to renewable energy. The Commonwealth Government has pledged AUD 213.6 billion to respond to the economic consequences of the pandemic, targeting funds to welfare recipients and providing wage subsidies for businesses. The stimulus funds are not targeted at a green recovery.

The government has shown no sign of scaling up climate action and is not planning to enhance its 2030 NDC target nor to adopt a net zero or any other stronger emissions reduction target. The government plans to meet its 2030 Paris Agreement NDC target by using carryover surplus emissions units from the Kyoto Protocol, significantly lowering actual emissions reductions, while other countries have ruled out using carryover.

Investments in renewable energy are in decline: the second quarter of 2020 saw the lowest investment in large-scale renewables since 2017, dropping 46% from the previous quarter. Renewables represented 21% of Australia’s total electricity generation in 2019, up from 19% in 2018. The 2020 renewable energy target was met last year and there have been no subsequent policies nor updated targets.

The government’s “technology neutral” approach has translated into increased support for the fossil fuel industry. The Technology Investment Roadmap Discussion Paper published in May 2020 advocates for natural gas and carbon capture and storage (CCS) technology, without ruling out support for coal and nuclear. In a further retrogressive step, the government has proposed to change the remit of the two government organisations that facilitate research and the flow of finance into the renewables sector (the Australian Renewable Energy Agency, ARENA, and the Clean Energy Finance Corporation, CEFC), towards a more technology neutral mandate, including carbon capture and storage. The government has expended AUD 233 million on the National Low Emissions Coal Initiative and allocated AUD 1 billion on the CCS Flagships program (expiring in 2020), yet there is no CCS in the power sector. There is only one CCS project operational in Australia and that is aimed at capturing reservoir CO2 from natural gas for LNG production. This plant, Chevron’s Gorgon gas CCS project, has experienced delays in start-up, and captures lower levels of carbon than contractually agreed, and is presently offline due to serious structural problems.

Meanwhile, at state level, governments continue to embrace renewable energy, with the Australian Capital Territory (ACT) and Tasmania being the latest to commit to strong targets. Only two states have no renewables targets.

The government continues to rely on ineffective policies such as the Climate Solutions Fund and the Safeguard Mechanism without any incentives for large industrial emitters to reduce emissions and even allowing for increasing baseline emissions. Australia is planning new coking coal mines for coal export mainly from the Bowen Basin in Queensland, increasing coal production by 4% from 2020 to 2030; LNG production is expected to increase by 6% over the same period.

In contrast, an alliance of leaders from business, industry and environmental organisations have issued a statement calling on the government to adopt a target of net-zero emissions by 2050.

The CAT’s emissions projections for Australia are 10% to 11% lower in 2020 and 11% to 14% lower in 2030 compared to our previous projections in December 2019, largely due to the impact of the pandemic on emissions. This projected drop in emissions would enable Australia to meet its 2020 target that it would otherwise not have been able to meet under the current policy scenario prior to the pandemic. However, this is not a sustained reduction in GHG emissions, and Australia is still not on track to meet its 2030 target despite the expected reductions due to the pandemic.

The CAT rates the existing Australia target under the Paris Agreement “Insufficient”, as it is not stringent enough to limit warming to 2°C, let alone 1.5˚C.

According to our analysis, Australia will need to implement additional policies to reach its 2030 target, even with the expected emissions reductions resulting from the COVID-19 pandemic. Emissions reductions are the result of declining economic activity rather than substantial climate policy. Australia’s economic recovery is not ‘green’, but follows a gas-led recovery and continues support for fossil fuels through a so-called ‘technology-neutral’ approach.

Government support for the fossil fuel industries is detrimental to a low carbon future. The Prime Minister has sent mixed messages, first stating the government will build a gas power plant if the electricity market does not commit to 1 GW of dispatchable power by April 2021, to replace the Liddell coal-fired power plant due for retirement in 2023. There was no evidence to support 1 GW of gas was necessary, considering new announcements of large battery and renewable energy zone projects. A few days later, the Prime Minister backtracked on this statement, but the mixed messages and threat of competing with a government subsidised company creates uncertainty for investors. The government appointed a National COVID-19 Commission Advisory Board to provide a business perspective on economic recovery. The board included fossil fuel and mining industry stakeholders. The Commission recommended underwriting a trans-Australian gas pipeline as well as increasing national domestic gas supply and subsidies for gas-fired power generation.

The gas-led recovery ignores warnings from business, industry and environmental organisations to support a green recovery in particular the opportunities for employment through accelerated investment in renewable energy and energy efficiency. The government will change the remit of government-owned financial and research organisations to be technology neutral when they were designed to support clean energy. The government also intends to underwrite investments into fossil fuel capacity and is financing a study into new coal fired power generation. Government projections from 2019 show Australia is on track to ramp up coal production from 634 Mt in 2020 to 659 Mt in 2030, and natural gas production from 82 Mt in 2020 to 87 Mt in 2030.

The reductions in energy-related emissions due to COVID-19 are mainly temporary or with a small impact. The temporary lockdown measures reduce road users and associated emissions while the measures are in place. The first two waves of COVID-19 causing lockdown in several states did not cease the operations of emissions -intensive industries such as mining and mineral processing.

Electricity data from the first wave of COVID-19 demonstrates only a small reduction in electricity consumption. In March 2020 there was a 2.4% power consumption reduction in the National Energy Market (NEM) compared to the previous year. The reduction was a result of changes in behaviour related to COVID-19 (such as working from home) but also related to other factors such as weather. One subsector with an expected long-term impact on emissions is the aviation industry, due to the reduction in the demand for flights while state borders restricted the movement of people, and because people are less inclined to fly due to risk of virus transmission.

Renewable energy has significantly increased in recent years, but has declined in 2020, with Q2 2020 investment into large-scale renewables seeing a 46 per cent fall from the previous quarter and 52 per cent lower than the quarterly average for 2019: the lowest since 2017. In 2019, renewables represented a 21% electricity generation share, compared to 19% in the previous year. Australia had a renewable energy target to ensure 33 gigawatt hours (GWh) of electricity is from renewable sources by 2020. However, since the renewable energy target was met in 2019, investment in renewables is dropping due to policy uncertainty, regulatory risks, issues related to grid connectors, and the lack of network investment. Investments and government policy support in the gas industry will lock Australia into an emissions intensive future, and likely lead to stranded assets.

Australia’s emissions excluding the land use, land use change and forestry (LULUCF) sector have increased 5% since 2014, when the federal government repealed the carbon pricing system. The government intends to achieve its target mainly through the use of Kyoto carryover — a move that a number of other countries with such carryovers have explicitly rejected. These carryover units make up more than half of the abatement task based on current government projections (not taking into account the impact of the pandemic).

There is a lack of climate policy across all sectors. Australia is one of the few G20 countries without mandatory emissions or fuel efficiency standards for cars. Nor does it have any policy to reduce emissions from freight trucks. It has not yet developed a strategy to support electric vehicles. It relies on ineffective mechanisms such as the Emissions Reduction Fund and the Safeguard mechanism that do not provide incentives for emissions reductions in the industry sector.

In contrast, the reality on the ground at the state level, in public opinion, across the business sectors and research organisations is very different. All states (and in addition, the Northern Territory and ACT) now have either aspirational or legislated zero-emissions targets, and some have strong renewable energy targets as well as green/renewable energy hydrogen strategies in place. Recent studies highlight the large employment benefits, economic recovery opportunities, through creation of new jobs while transitioning to renewable energy.

In August 2020, a forum comprised of business, farming, investment, union, social welfare and environmental sectors issued an extraordinary statement calling for the government to adopt a target for net-zero emissions by 2050. A recent poll from June 2020 found that 70% of Australians expect the government to protect the environment as part of the economic recovery efforts. Another poll found 72% of Australians view the bushfires of November 2019 to January 2020 as a wakeup call on the impacts of climate change, with 73% agreeing that the Prime Minister should lead on climate change action. A federal-level commitment to zero emissions and a Paris Agreement consistent 2030 target as well as a renewable energy target beyond 2020 are necessary to ensure a consistent federal framework for a fast transition to a zero-carbon future.

Further analysis

Latest publications

Stay informed

Subscribe to our newsletter