EU

Country summary

Assessment

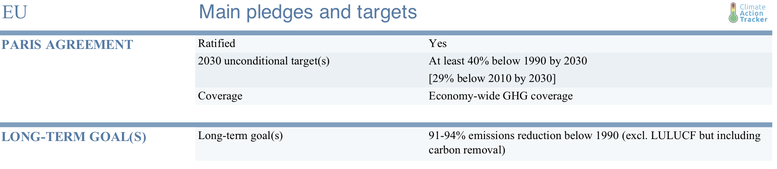

NDC update: In December 2020, the EU submitted an updated NDC to the UNFCCC. Our analysis of its new target is here.

Since our last update in December 2019, the EU271 has made a big step to regain its position as the climate leader in the area of climate action. While its climate actions are not yet compatible with the Paris Agreement, it stands out in comparison with other countries in terms of making climate action the driver of economic recovery. The EU’s major weakness remains the outdated and severely inadequate 2030 emissions reduction goal of “at least 40%”. In September, the Commission recommended that the EU increase its target to at least 55% (incl LULUCF); however, this does not go far enough. An increase of this goal to 65%, accompanied with funding climate action abroad, would make the EU the first region with commitments compatible with the Paris Agreement. As these changes are not yet reflected in a significant increase of the EU’s emissions reduction goal, the CAT rates the EU27 as “Insufficient”.

The EU27 has made climate mitigation one of the three main priorities in its COVID-19 recovery. In July 2020 member state leaders agreed that at least 30% of its multi-annual budget and recovery fund agreed in July 2020 is to be spent on achieving the EU’s climate neutrality goal by 2050 and meeting its increased 2030 emissions reduction goal. However, the EU has still not agreed on the exact level of that goal. In the framework of the European Green Deal the EU is planning to revamp almost all of its climate legislation and complement it with additional measures. This includes strengthening the role of the European institutions, especially the European Commission, in setting the EU’s emissions trajectories post-2030.

We expect that GHG emissions in 2020 will be 10% to 11% lower than 2019. While this significant reduction in emissions is mostly driven by the COVID-19-related restrictions and subsequent recession, to some degree it is also a continuation of an ongoing trend. After a decrease of 2.1% in 2018, CO2 emissions from energy combustion, constituting 75% of all GHGs emissions, decreased in 2019 by 4.3%. This emissions reduction was mainly driven by the power sector. Early estimates indicate an acceleration in the rate of decrease from 6.5% in 2018 to 15% in 2019. In the Q1 of 2020, emissions from this sector decreased by 20%.

The EU considers climate action as one of the drivers of post-COVID-19 economic recovery. Achieving the goal of spending 30% of the EU’s multiannual budget and recovery fund, as agreed by the European Council in July 2020, would amount to at least €547 billion being spent on climate mitigation. This goal still needs to be confirmed by the European Parliament, which can increase it further. In most cases, this funding will leverage additional resources from member states or private sector.

This offers the opportunity to accelerate the major transformation of the European economy away from fossil fuels. Moving from combustion cars and planes to (rapid) trains will be an important part of this transformation. Additional potential for economic growth and job creation lies in the area of energy efficiency, especially in the buildings sector. The Commission’s ‘Renovation Wave’ initiative, to be published in September 2020, offers the potential to merge the EU’s three priorities of climate mitigation, digitalisation, and resilience, while at the same decreasing the EU’s energy dependence and energy poverty, and improving air quality.

The implementation of the European Green Deal involves revamping of the EU’s climate legislation and complementing it with new measures. This creates an opportunity for the EU to wean its economy off fossil fuels, reduce energy imports, and also to create new jobs in areas most affected by the COVID-19-induced economic crisis.

The Commission has already tabled strategies for decarbonising the EU’s industry, integrating different sectors, and jump starting a hydrogen economy. The proposal of the European Climate Law provides the Commission with the authority to determine an emissions reduction pathway consistent with the EU “climate neutrality” goal. However, it fails to increase EU’s emissions reduction goal for 2030. In September, the Commission recommended that the EU adopted a domestic emission reduction of at least 55% below 1990 levels by 2030 including LULUCF. This recommendation is below the 60% emissions reduction goal adopted by the European Parliament’s ENVI Committee in September 2020. The proposal of the European Parliament’s rapporteur for Climate Law, Jytte Guteland, to also assess increasing the EU’s emissions reduction goal to 65% has not been taken into consideration.

The upper range of the CAT’s EU emissions projections for 2030 reflecting policies already implemented by the member states (and the UK) is 4 percentage points below the pre-COVID-19 estimates. This would result in a combined emissions reduction of 37% below 1990 levels. This is mainly due to the impact of the COVID-19-induced economic crisis. Implementation of the EU's renewable energy and energy efficiency goal would reduce emissions by up to 48%. This would not be affected by the crisis – the achievement of this goal would be much easier due to the decrease in energy demand.

The CAT rates the existing EU target under the Paris Agreement “Insufficient”, as it is not stringent enough to limit warming to 2°C, let alone 1.5˚C.

1 | The UK withdrew from the EU on 31 January 2020. Due to the lack of data it was not possible to complete this update using EU27 data only. Moreover, it is unclear how the EU NDC will be calculated post-Brexit. Therefore, the data used in the assessment and the NDC rating is based on the EU27+UK; however, the analysis of current policies focused on the EU27. We have referred to the EU27 and EU27+UK throughout the assessment as appropriate.

Due to the COVID-19-induced lockdown and economic recession, EU emissions in 2020 are expected to decrease by between 10% and 11% lower than 2019. This would result in an overall reduction of between 34 -35% in 2020 below 1990 levels. The economic rebound in 2021 is projected to result in emissions increasing by 2% in comparison to 2020. The already-implemented measures at the national, member state level will result in emissions decrease in 2030 by around 37% below 1990 levels. The achievement of the renewable energy and energy efficiency goals adopted at the European level, will result in an emissions reduction of 48% in 2030. This indicates that the EU is very close to reaching - or even exceeding - its current, inadequate emissions reduction goal for 2030. Significant strengthening of this goal is thus not only feasible, but also necessary to fulfil the Paris Agreement’s requirement of reflecting “the highest possible ambition”.

The fastest emissions reduction of all sectors took place in the power sector. Between 1990 and 2019 emissions from this sector decreased by 44%. The lockdown and the economic recession are expected to further reduce the emissions from the power sector. They will be accompanied by a continued deployment of renewables driven by their decreasing costs and the increasing price of emissions allowances in the framework of the EU’s Emissions Trading Scheme (EU ETS). Despite the economic slowdown, the price of emissions allowances rebounded in mid- 2020 and reached €30 – its highest level in 14 years.

Coal has increasingly been replaced by renewables. In 2019 the share of renewables in power generation increased by 1.8 percentage points and reached 34.6%. At the same time, the share of coal in electricity generation decreased in the EU27+UK to 14.6% - almost 4.4% less than in 2018. The share of coal will continue to fall in 2020 as Sweden and Austria became coal-free in April. Spain has switched off seven coal power plants, which had a combined installed capacity of 4.6 GW – almost half of the EU’s total installed coal capacity.

Emissions from the industry sector fell by around 2% in 2019. A much more significant decrease can be expected in 2020 as a result of the COVID-19 induced recession. However, this decrease is only temporary. Emissions are likely to rise as the economy recovers. The New Industrial Strategy and European EU Hydrogen Strategy presented by the European Commission in the first half of 2020 creates the opportunity to put this sector on the path to permanent decarbonisation.

Emissions from the road transport sector remained relatively stable in 2018, countering the trend of decreasing emissions in the other sectors. In 2019, the share of new EVs registered in the EU27+UK increased to 3% - 1% higher than in 2018. A much higher increase took place in the first quarter of 2020, with the share of electric vehicles at 6.8%. However, it remains to be seen to what degree this increase resulted from a fall in the sale of combustion vehicles due to the COVID-19 crisis.

While electro mobility in the EU is gaining momentum, the EU and its member states are not taking full advantage of promoting a modal switch. A number of EU countries failed to mention expansion and modernisation of railways in their National Energy and Climate Plans. The funding to be made available on climate action in the framework of the Multiannual Financial Framework and NextGenerationEU Recovery Fund presents the opportunity to replace domestic and, in some cases, intra-EU flights with rapid train connections.

The EU’s new Energy Performance in Buildings Directive (EPBD), adopted in 2018 obliged each member state to submit a long-term renovation strategy leading to fully decarbonising its building stock by 2050. To increase the renovation rate, the Commission is planning to launch its ‘Renovation Wave’ initiative in September 2020. It remains to be seen whether this will help address the issue of the low rate of deep renovation of the existing building stock. An increase of the renovation rate to 3.5% would be necessary to make emissions from the EU building sector compatible with the 1.5°C temperature increase limit (Climate Action Tracker, 2020b).

Further analysis

Latest publications

Stay informed

Subscribe to our newsletter