Singapore

Country summary

Assessment

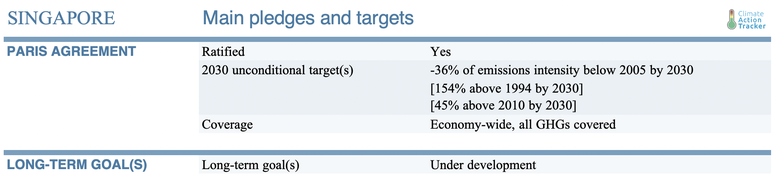

Despite its high economic capacity, Singapore has a very weak climate target, which we rate as “Highly insufficient”, and is likely to over-achieve it without implementing any additional policies. Singapore has signalled it will “enhance” its target to an absolute target for COP26, but the updated NDC target does not raise ambition. The NDC update will convert the emissions intensity target to an absolute emissions target in 2030 of 65 million tonnes of CO2 which is 58% above 2014 emission levels. Singapore needs to substantially strengthen its target.

While renewable energy capacity has expanded, gas remains the dominant energy source in the power sector, accounting for 96% of electricity generation. At a speech to the Singapore International Energy Week in October 2019, the Minister for Trade and Industry noted that natural gas would continue to play a role in meeting the country’s energy needs for the next 50 years. At the same time, he unveiled a new 2 GW by 2030 target for solar energy.

In 2019, Singapore began implementing a carbon tax for industrial facilities of $5 SGD/tCO2e (roughly 3.7 USD/tCO2e). This low starting level is unlikely to generate the right incentives for a large-scale switch to carbon-free generation technologies in the medium term that would set emissions reductions on a trajectory compatible with the Paris Agreement. The carbon tax will remain at $5 SGD/tCO2e until 2023. The government has indicated it plans to increase the tax to $10-15 SGD per tonne by 2030.

The government conducted public consultations on its long term low emissions strategy in mid-2019, and announced the strategy will be submitted to the UNFCCC in 2020. The strategy will have a target to halve its peak 2030 emission levels by 2050, and only achieve net zero emissions in the second half of the century.

In April 2019, the government-controlled Development Bank of Singapore (DBS) announced it would stop funding new coal-fired power stations globally, yet it continues to be involved in several proposed coal power plants in Southeast Asia.

In the transport sector, energy demand and associated emissions are expected to flatten out as a result of multiple measures to promote public transport, modal shifts, and improve the emissions intensity of road transport.

To raise awareness of waste issues and the need to recycle resources Singapore declared 2019 as “Year Towards Zero Waste”. Singapore published the Zero Waste Masterplan with a target of reducing waste sent to Semakau Landfill by 30% by 2030.

Singapore’s Nationally Determined Contribution (NDC) emissions target is very weak compared to currently implemented policies. Even without any additional policies, Singapore will overachieve its NDC target, but absolute emissions will continue to rise at least until 2030.

We rate Singapore’s NDC 2030 target “Highly insufficient”, meaning that Singapore’s climate commitments are not in line with any interpretation of a “fair” approach to the former 2°C goal, let alone the Paris Agreement’s 1.5°C limit.

Emissions in Singapore are dominated by the energy and industry sectors. Energy and transformation industries represent 38% of total emissions, industrial processes 4%, fuel combustion from industry 40%, and fugitives 2% in 2014 (National Environment Agency, 2018). Transport represents 14% of emissions, LULUCF 0.1%, buildings 0.1% and 0.6% of emissions are from waste (National Environment Agency, 2018). Our current policy projections indicate Singapore’s emissions will increase to 57 MtCO2e by 2030, a 12% increase from 2014.

The carbon tax, targeting upstream emissions from large emitters, started at 5 SGD/tCO2e from 2019 and will be reviewed by 2023 with the intention of increasing it to between 10 SGD/tCO2e and 15 SGD/tCO2e by 2030. A tax could encourage more renewable energy in place of fossil fuel energy by adding a price for the emitted carbon. However, higher tax levels are likely needed to encourage a significant shift to decarbonising the power sector.

Singapore’s implemented mitigation policies have focused on replacing oil in the electricity generation sector for less carbon intensive fossil fuels, resulting in natural gas representing over 96% of electricity generation in 2016, with around 1% coal and around 3% municipal waste and solar. To diversify its energy mix, Singapore has expanded its solar energy capacity in recent years, going from 26 MW of installed Solar-PV capacity in 2014 to 202 MW in Q2 2019.

Additional policies in the power sector include multiple incentives to increase the share of renewable generation and the expansion of Waste-to-Energy (WTE) capacity. The Public Utilities Board (PUB), Singapore’s National Water Agency, launched a floating solar PV testbed at Tengeh Reservoir in October 2016, and has plans for floating solar projects at reservoirs. The SolarNova programme that forms part of Singapore’s plan to reach 350 MW of installed solar PV capacity by 2020, has accepted three tenders with more to come.

However, Singapore’s energy mix is likely to remain very uniform in the future, resulting in a prolonged dependence on fossil-fuels.

Outside the power generation sector, Singapore’s mitigation efforts almost exclusively consist of measures aimed at further improving energy-efficiency through programmes like Green Mark standards for buildings, green procurement, public transport, fuel efficiency standards, home appliance efficiency standards, industrial energy efficiency, and waste management. However, with a fossil fuel dependent energy mix, the effect of these policies in emissions is limited and does not compensate for the overall increase in energy demand.

Singapore has been moving to promote modal shifts towards public transport and to improve the emissions intensity of road transport. In 2014, the transport sector made up 13.6% of total emissions.

Singapore’s plans to increase the length of the rail network from 230 km in 2019 to about 360 km by 2030 will enable eight in ten households to be within a ten-minute walk of a train station. Singapore’s target for the public transport modal share during morning and evening peak hours is to reach 70% by 2020 and 75% by 2030, up from 59% in 2008 and 67% in 2017.

Since February 2018, the growth of private vehicles has been effectively capped, when the permissible growth rate of private vehicle population was reduced from 0.25% to 0%.

Further analysis

Latest publications

Stay informed

Subscribe to our newsletter