Switzerland

Policies & action

This assessment includes our analysis for Switzerland from 30 November 2020 translated into our new rating methodology. We have not undertaken new analysis of Switzerland’s climate policies, though our current policy projection now reflects the last historic emissions (2019) and more recent GDP estimates for the extent of the COVID impact. We have also noted the potential impact of the June 2021 referendum on Switzerland’s climate legislation. We will analyse Switzerland’s profile fully in the coming months, at which time the rating may change.

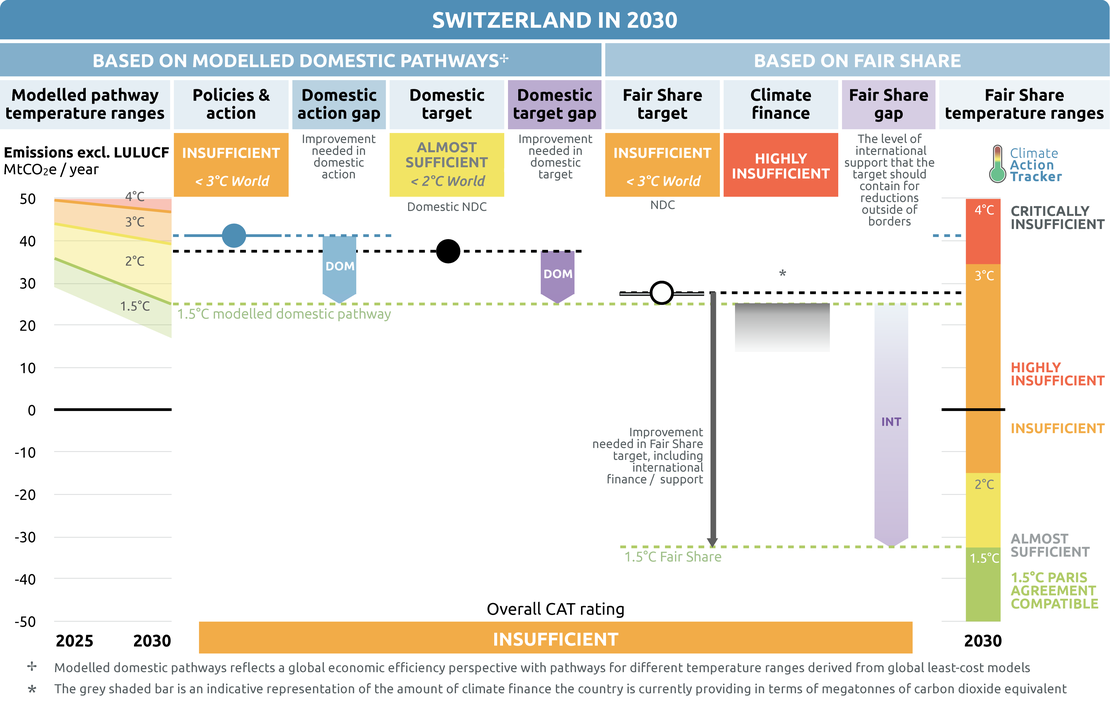

Switzerland’s efforts to tackle climate change were struck a blow in 2021 after the failure of its amended CO2 Act to pass in a June referendum. Under its planned policies scenario, in which many of the policies from the amended CO2 Act were contained, Switzerland would have met its now rejected domestic emissions target. Under current policies, however, Switzerland is projected to miss even its less ambitious previous domestic target of a 30% reduction below 1990 levels. The CAT rates Switzerland’s current policies as “Insufficient” when compared to modelled domestic pathways. The “Insufficient” rating indicates that Switzerland’s climate policies and action until 2030 need substantial improvements to be consistent with the Paris Agreement’s 1.5°C temperature limit. If all countries were to follow Switzerland’s approach, warming would reach over 2°C and up to 3°C.

Further information on how the CAT rates countries (against modelled pathways and fair share) can be found here.

Policy overview

Switzerland’s 2020 emissions are estimated to have been 44 MtCO2e and are expected to reach around 41 MtCO2e by 2030 (excluding LULUCF), under its current policies. This projected reduction is lower than previous estimates as a result of the COVID-19 related economic slowdown, and are equivalent to an 18% and 23% reduction below 1990 levels, respectively (excluding LULUCF). Thus, Switzerland is not projected to meet its current target of a 30% reduction in domestic emissions below 1990 levels under current policies. However, its overall NDC of a 50% reduction below 1990 levels may be partially met through the use of carbon credits from international mechanisms.

In Switzerland’s 4th Biennial Report, released in December 2019, the implementation of all planned policies including the updated CO2 Act is projected to lead to a 35% reduction in total GHGs by 2030, enough to meet its current domestic target.

The recently rejected CO2 Act stated that its purpose was to limit the average increase in global average temperature to well below 2°C and pursue efforts to limit the temperature rise to 1.5°C. However, the emissions reduction targets included in this updated law were not aligned with what would be a fair-share effort to achieve this outcome.

In October 2020 Switzerland and Peru signed a carbon credit agreement where Switzerland will finance emission reduction projects that are designed to contribute to sustainable development in Peru while the emissions reductions would count towards the Swiss NDC (Lo, 2020). In order to ensure environmental integrity, both Peru and Switzerland would have to apply robust accounting systems so that the reductions are only counted once. The rules and oversight provisions for such transfers have not yet been agreed under Article 6 of the the Paris Agreement.

Switzerland’s most relevant cross-sectoral climate policy is the carbon levy charged on fossil fuels. Due to a slower than expected decrease in emissions, the fee was increased in 2018 from CHF 84 (USD 92) to CHF 96 (USD 106) per tonne of CO2, and remains at this price in late 2020, however three political parties are calling for an increase to the levy to CHF 120 from 2021 (Federal Office for the Environment, 2019; Graf, 2020). The combustion of different fossil fuels is charged depending on their emissions intensity, e.g. light heating oil is charged with CHF 254.40 for 1,000 litre whereas natural gas is charged 255.40 for 1,000 kg of natural gas (Schweizerische Eidgenossenschaft, 2020a). The amended CO2 Act allowed for an increase of the levy to CHF 210 (USD 231) if the country is not on the path to achieve its emissions reduction goals (Schweizer Parlament, 2020a).

The majority of the proceeds from the levy is reimbursed to the citizens. Under the previous version of the CO2 Act, CHF 300 million (USD 330 million) of the remaining annual revenue is spent on emissions reduction in the building sector, and a further CHF 25 million (USD 27.5 million) on the Technology Fund (Der Bundesrat, 2012). In the updated version of the CO2 Act these two streams of funding were to be merged into the Climate Fund that will support emissions reduction measures across a number of sectors including buildings, transport and the governments of Switzerland’s cantons and local municipalities. The Climate Fund was to be capped at CHF 450 million (USD 495 million) annually (Schweizer Parlament, 2020a).

Another cross-sectoral instrument influencing greenhouse gas emissions is Switzerland’s emissions trading scheme. Companies participating in the emissions trading are excluded from the obligation to pay the emissions levy. In March 2019, after two years of negotiations, the Swiss Parliament adopted a law linking the Swiss emissions trading scheme with the European EU ETS which came into effect on 1 January 2020. While both systems continue to function separately, the emissions certificates can now be used interchangeably between the two systems (Bundesamt für Umwelt, 2019b). The higher prices of emissions allowances under the EU ETS than under the Swiss emissions trading - EUR 25 versus EUR 12.65 (average auction price in 2019), respectively – will accelerate emissions reductions by the emitters responsible for a third of emissions resulting from the combustion of fossil fuels (EEX, 2019; Swiss Federal Audit Office, 2017). In November 2019, the Federal Council expanded the scope of the Swiss ETS to include civil aviation and fossil-thermal power plants (ICAP, 2020).

Energy supply

In 2019, roughly 96% of electricity in Switzerland was generated from renewable (58%, mostly hydro) or nuclear (36%) sources of energy (IEA, 2020). As a result, the Swiss electricity sector has a very low carbon intensity of roughly 36 gCO2/kWh – significantly below that of the EU average (315 gCO2/kWh in 2015, see Figure 1). A recent development is the inclusion of the Swiss power sector in the ETS from 1 January 2020, but this only affects a small number of operators given the sector’s highly decarbonised nature.

In response to the COVID-19 crisis, waiting times for subsidies to solar PV projects have been shortened with the intent of protecting the development of such renewable energy sources (Bundesamt für Energie, 2020c). A total of CHF 46 million (USD 51 million) has been made available to project planners, installers and local planning bodies. In addition, an exemption has been introduced for projects that would have been subjected to a lowering of remuneration rates from April 1 2020 due to COVID-19-related delays.

Electricity emissions intensity

A May 2017 referendum adopted the Energy Strategy 2050, a package of measures aiming at increasing energy efficiency, reduction of CO2 emissions, and steadily replacing nuclear energy by renewables (Bundesamt für Energie, 2018a). Many of these measures were included in the reform of the Energy Law that went into effect in January 2018.

According to the law, nuclear energy is set to be steadily replaced by renewables, with the first nuclear plant having already been shut down in December 2019. By 2035 electricity generation from hydro power plants should remain at the current level of around 37.4 TWh. Electricity generation from non-hydro renewables should increase from around 3.3 TWh to 11.4 TWh in the same period. The law also sets the goal of decreasing energy consumption by 43% and electricity consumption by 13% below 2000 levels by 2035. It also introduces some changes to feed-in tariffs for renewables, including shortening the period during which installations receive the tariffs from 20 to 15 years (Die Bundesversammlung der Schweizerischen Eidgenossenschaf, 2018; VSE, 2019).

Industry

Most GHG emission reduction policies and measures affecting the industry sector are implemented under the CO2 Act and cover CO2 emissions from fossil fuel use. These include the CO2 levy on heating and process fuels, the Swiss emissions trading scheme, and the negotiated reduction commitments. A number of key non-CO2 emissions, however, are not covered under the Act, and have been targeted separately. For example, a number of provisions relating to substances stable in the atmosphere cover all F-gases and are expected to result in a reduction of roughly 1.1 MtCO2e in emissions of such gases in 2020 (Schweizerische Eidgenossenschaft, 2020c).

Similar to the EU, Switzerland also uses an emissions trading scheme (ETS) to lower emissions from large energy intensive entities. However, the Swiss ETS is much smaller than the European ETS, not only because of the smaller market but also due to the fact that the emissions generated by 54 companies in the power, cement, pharmaceutical, refinery, paper, district heating, and steel sectors covered by the scheme represent only 10% of the country’s emissions. Emissions from the sector were capped in 2013 at 5.63 MtCO2, and required to be reduced by 1.74% per year in order to reach a target of 4.91 MtCO2 in 2020 (13% reduction on 2013 levels) (Mission of Switzerland to the European Union, 2017).

An examination by the Swiss Federal Audit Office came to the conclusion that, in its current form, the Swiss ETS “generates hardly any incentives for reductions”. The audit office found several regulatory shortcomings, calling the impact of the ETS into question. A high number of emissions allowances allocated free of charge decreased the willingness of companies to invest in energy efficiency. An annual decrease of the cap by 1.74%, which was below the overall emissions reduction, has led to an oversupply of allowances and consequently low prices. Without any reforms, the audit office found the oversupply of allowances would reach 4.5 million certificates in 2020, equivalent to 95% of the overall cap in 2013 (Swiss Federal Audit Office, 2017). The small size of the market further worsens the oversupply of allowances in case of an unexpected production stoppage or increase, and the resulting sudden changes in demand or supply of allowances.

To deal with the allowances’ price volatility, in 2011 the European Commission and Swiss government opened negotiations on linking both carbon markets. While the price of allowances has been increasing in the EU ETS and averaged over EUR 25 in 2019, the price of Swiss allowances fell from CHF 40 (USD 44) in 2014 to CHF 8 (USD 8.8) in 2018. In March 2019 the Swiss Parliament adopted a law linking the Swiss emissions trading scheme with the European EU ETS (Bundesamt für Umwelt, 2019b), and as a result, the price of Swiss allowances rose to CHF 18.2 (USD 20) by the end of 2019 (Schweizerische Eidgenossenschaft, 2020b). The schemes were officially linked on 1 January 2020 and this is likely to ensure high allowance prices in the Swiss ETS moving forward.

Transport

Emissions from the transport sector are responsible for over 32% of Switzerland’s total GHG emissions (excl. LULUCF), and until 2008, emissions from this sector increased to 13% above 1990 levels (Federal Office for the Environment, 2020). Since then, they have been steadily decreasing but in 2018 were still 1.6% higher than 1990 levels.

In response to the COVID-19 crisis, the aviation industry has received bank guarantees of almost CHF 2 billion with the requirement that the aviation companies cooperate in the development of future climate policy (Schweizer Parlament, 2020b). The Federal Council failed to pass other, more stringent and binding regulations. For example, a stipulation that airlines must reduce their emissions in line with the goals of the Paris Agreement was rejected, as was a condition that emergency funds received must be used in a way that contributes towards the achievement of net-zero emissions. A proposal requiring airlines to participate in the development of sustainable e-fuels was also rejected.

The inclusion of domestic and international aviation between Switzerland and member states of the European Economic Area (EEA) into Switzerland’s ETS since 1 January 2020 is a significant policy development, with emissions from the sector in the scheme to be capped at 2018 levels (Schweizerische Eidgenossenschaft, 2020c). In addition, starting from 2020 for new designs, and from 2023 for in-production models, aircraft in Switzerland will be subject to CO2 emission targets. Switzerland has indicated its intention to participate in the carbon offsetting and reduction scheme for international civil aviation (CORSIA), under which emissions are capped at 2019 levels. Applicable standards and recommended practices for the scheme are currently being prepared by the International Civil Aviation Organisation, with the pilot phase beginning in 2021. This scheme has significant shortcomings, meaning it is unlikely to deliver the substantial reductions needed to achieve the ICAO’s aspirational goal of carbon neutral growth from 2020.

In 2012, Switzerland adopted a regulation that included the goals of reducing emissions for newly-registered passenger cars to 130 gCO2/km, in alignment with EU vehicle emissions regulations (Swiss Federal Office of Energy, 2019). Starting in 2020, as with the latest EU regulations, the emissions of new cars cannot exceed 95 gCO2/km. The emissions reduction goal for vans and light trucks is 147 gCO2/km from 2020 onwards. The amendment of the CO2 Act introduced an emissions reduction target for the period after 2025: between 2025 and 2029 emissions of passenger vehicles should be 15% lower than in 2020. By 2030 this reduction should – like in the case of the EU – decrease by 37.5% below the 2021 value, with vans and light duty trucks required to be 31% below the 2021 value. Emissions from heavy duty vehicles should decrease by 30% between 2020 and 2030 (Schweizer Parlament, 2020a). Car importers exceeding those limits were to be required to pay a penalty of between CHF 95 and 152 for each gCO2/km they exceed. It is not clear what will be carried forward in subsequent legislation.

After a continuous decrease in average emissions intensity of passenger cars from 198 gCO2/km in 2002 to 133.6 gCO2/km, 2017, 2018 and 2019 saw slight increases – by 0.5, 3.7, and 0.3 gCO2/km respectively to sit at 138.1 gCO2/km in 2019 (Bundesamt für Energie, 2020a). The emissions intensity of light commercial vehicles continued to decrease from 227 gCO2/km in 2008 to 181.5 gCO2/km in 2019. Both values are significantly above that of the European passenger and light commercial vehicles of 122.4 and 158.4 gCO2/km, respectively (European Commission, 2020a).

Despite the clear need to take more action to reduce emissions from passenger and commercial vehicles, the penalty for exceedance of emissions limits was decreased for the fourth and each following gCO2/km of exceedance from CHF 142.50 to 104.50 (Bundesamt für Energie, 2018b). This will reduce the costs of purchasing inefficient and carbon-intensive vehicles. Although the average cost of exceedance was reduced in this manner, the total penalties paid by importers has risen dramatically since 2017 due to the increasing average fuel consumption of new vehicles. In 2017, total penalties paid by importers was CHF 2.9 million, rising to CHF 78.1 million in 2019, with the average penalty per vehicle in 2019 totalling CHF 252 (Bundesamt für Energie, 2020b).

Given the very low emissions intensity of Switzerland’s power sector, a shift to electric mobility has a disproportionately high impact on overall emissions reductions. The uptake of electric vehicles in Switzerland is faster than the EU average. In the first half of 2020, 9.8% of all vehicles sold in Switzerland were electrically chargeable vehicles, which includes battery-only (5.5%) and plug-in hybrid (4.3%) vehicles (ACEA, 2020). H1 2020 saw a significant increase in the share of battery-only sales (+44% year-on-year), while plug-in hybrid vehicle sales as a share of total sales rose dramatically (+540% year-on-year). Although the uptake of electric vehicles is accelerating, their share of new sales in Switzerland remains significantly below that of some countries with a comparable level of income that make electric cars more affordable (e.g. 26% in Sweden, 15% in Finland, 68% in Norway in H1 2020).

In December 2018, in response to consultations with stakeholders from the auto and electricity industries, buildings sector, and local authorities, the Swiss government adopted its Roadmap for Electric Mobility 2022. It includes a goal of increasing the share of electric vehicles in new vehicles to 15% by 2022 (Bundesamt für Energie & Bundesamt für Strassen., 2018). Measures announced by the federal government to achieve this goal so far include the development of a fast-charging network along the national highways, the introduction of green zones for EVs, and real-time signalling of free charging points at rest stops and rest areas.

Such a goal, however, is unambitious as it represents a lower rate of increase than that observed between 2018 (3.2% of all registered cars electrically chargeable) and 2019 (5.6% of all registered cars electrically chargeable) (ACEA, 2019b, 2019a). The rate of increase in the share of electric vehicles needed to achieve a 15% share by 2022 is less than 2 percentage points per annum, far slower than what’s needed to phase-out the sale of combustion cars altogether by 2035, a goal considered compatible with the Paris Agreement (Kuramochi et al., 2018). Also, instead of any mechanism designed to decrease the role of combustion vehicles, the Roadmap instead suggests a public relations approach of “awakening of positive emotions” which may result in even more vehicles per person. With 539 vehicles per 1,000 inhabitants in 2018, Swiss car ownership is around 1.7% higher than the EU27 average (European Commission, 2020b).

The share of freight transported by rail in Switzerland in 2018 was, at 37%, much higher than in the EU (19%). However, it was significantly below the share of freight transported by rail in this country in the 1980s (around 53%). This decreasing trend was especially clearly noticeable in 2017 when the number of products transported by rail decreased by 7% while the number of products transported by road increased by 1.5% (Bundesamt für Statistik, 2018).

The revision of the CO2 Act introduced a levy on airplane tickets at between CHF 30 (USD 33) and CHF 120 (USD 132). Were it adopted, the levy would have been determined by the flight distance and class (Schweizer Parlament, 2020a). Similar to the levy on fossil fuels, the revenue from the aviation levy would have largely been reimbursed to all citizens, with some share of it flowing into the Climate Fund.

Buildings

In 2018, the buildings sector, including services and households, was responsible for roughly 24% of Switzerland’s total GHG emissions (excl. LULUCF), a decrease compared to 1990 when they represented around 32% of the country’s emissions. This has been the result of emissions in this sector decreasing much faster – by 33% between 1990 and 2018 - than in the case of the overall emissions (Bundesamt für Umwelt, 2020). However, this decrease is still not enough to meet the goal of a 40% reduction in emissions below 1990 levels by 2020 that was adopted in the 2012 CO2 Regulation, meaning substantial further effort is needed (Der Bundesrat, 2012).

The recently rejected CO2-Act, included an extension of this target, requiring cantons to develop building standards for new and existing buildings to ensure total buildings emissions are 50% below 1990 levels by 2026/27 (Schweizer Parlament, 2020a). In addition to this, fossil fuel heating systems were to be banned for use in new buildings from 2023, while replacement heating systems in 2023 would not have been permitted to emit more than 20kgCO2/m2 of building space, which was to be further reduced by 5kgCO2/m2 in each subsequent year.

Energy efficiency standards for buildings are decided at the regional level, while municipalities are allowed to introduce even stricter standards (Immopro, 2017). In 2014, the regional governments agreed on a new standard - called MuKEn14 – to be implemented by all regions before 2018, which became binding in 2020. For new builds, the standard amounts to 35 kWh/m2 for single and multi-family houses. For warehouses, the standards are even stricter and should not exceed 20 kWh/m2. Each house should also be equipped with a renewable source of power amounting to at least 10 W/m2 of the living space (EnFK, 2014).

These targets have already been met by some of the buildings complying with the Swiss “Minergie” standards. There are three major categories: Minergie houses should not consume more than 55 kWh/m2 for new single houses and 90 kWh/m2 for renovations. For Minergie-P the standards are 50 kWh/m2 and 80 kWh/m2 respectively. For Minergie-A the standards are 35 kWh/m2 for both, new builds and renovations. By April 2017, there were a total of 47,253 Minergie certified buildings in Switzerland (Minergie, 2019).

The Energy Strategy 2050 will allocate up to 450 million Swiss francs (USD 467 million) from the Cantons and the CO2 levy to reduce buildings’ energy use. It plans to achieve this by allowing an option for allocating energy-efficiency investment costs to the two following tax periods, and a tax deduction of demolition costs when replacing older buildings (Federal Office of Energy, 2017).

Agriculture

Emissions from the agriculture sector in 2018 constituted around 13% of total emissions (excluding LULUCF) – representing a roughly constant share of total emissions as they have been decreasing at around the same pace as overall emissions (Federal Office for the Environment, 2020). The Climate Strategy Agriculture aims to reduce agricultural emissions by at least one third by 2050 with technical, operational and organisational measures, and by another third with measures influencing food consumption and production (Schweizerische Eidgenossenschaft, 2020c). It includes both mitigation and adaptation to climate change in the agricultural sector.

Switzerland’s Agricultural Policy 2014-2017 and 2018-2021 contains the abolition of unspecific direct payments (livestock subsidies, general acreage payments), additional funds for environmentally-friendly production systems, and for the efficient use of resources (e.g. increase in nutrient efficiency and ecological set-aside areas, reduction of ammonia emissions). It is expected to result in reductions of 0.2 MtCO2e in 2020.

Forestry

Except for a few select years, forestry constitutes a sink of emissions in Switzerland of between 1-4 MtCO2 annually (Schweizerische Eidgenossenschaft, 2020c). Under current policies, however, this is expected to change, with the sector projected to become a source of emissions between 2020 and 2030 of roughly 1 MtCO2e per year. In 2018, 31% of Switzerland’s total area was covered by forests (Bundesamt für Umwelt, 2019a).

The Forest Policy 2020, adopted in 2011 and updated in 2017, aims to coordinate the ecological, economic and social demands on forests, managing forests in a sustainable manner. It includes a long-term target of a CO2 balance between forest sink, wood use and wood substitution effects. Given the current age structure of Swiss forests, this implies aiming at increased harvesting rates over the coming years. The expected mitigation impact of the Forest Policy 2020 is 1.2 MtCO2e in 2020 (Schweizerische Eidgenossenschaft, 2020c).

A renewal of the Forest Act in 2017 included both measures addressing the need for adaptation to climate change, as well as a stipulation that, where suitable, the construction of Swiss government buildings is to be done with the use of sustainably sourced Swiss timber (Schweizerische Eidgenossenschaft, 2020c).

Waste

Emissions from the waste sector in Switzerland made up roughly 1.4% of total GHG emissions (excluding LULUCF) in 2018 and registered an absolute decrease of almost 37% between 1990 and 2018 (Federal Office for the Environment, 2020). Since 2000, the disposal of untreated municipal waste into landfill has been prohibited, with an increase in the capacity of waste incineration plants implemented to accommodate this ban (Schweizerische Eidgenossenschaft, 2020c). These incineration plants have substantially reduced methane emissions from Swiss landfills and produce roughly 2% of Switzerland’s total energy consumption.

A further measure in the waste sector is the ordinance on the avoidance and management of waste, implemented in 2016, which promotes closed-loop material flows. While a large proportion of Switzerland’s municipal solid waste is already recycled (53% in 2015), further improvements could be made in the reduction of environmental pollution and strengthening the reliability of the waste removal system as a whole (Schweizerische Eidgenossenschaft, 2018).

Further analysis

Latest publications

Stay informed

Subscribe to our newsletter