China

Country summary

Overview

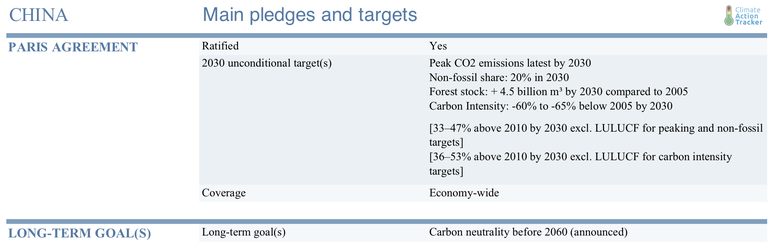

NDC update: In December 2020, China proposed updated NDC targets. Here is our analysis of the announcement.

President Xi Jinping has announced in September 2020 that China will strengthen its 2030 climate target (NDC), peak emissions before 2030 and aim to achieve carbon neutrality before 2060. China’s COVID-19 response contains elements of a green recovery, showing an improved strategic deviation from the post-2008 financial crisis, but as yet lacks the policies and direction to set China on a low-carbon trajectory.

Positively, the government has issued broader stimulus packages to double down on existing priorities transitioning industry and labour force towards a modernised digital economy rather than restarting traditional infrastructure strategy, and remains committed to accelerated penetration of renewable energy systems and electric vehicles.

However, recovery activities remain carbon-intensive and require high energy demand from a system run primarily on fossil fuels, while the phasing out of supply-side incentives has affected the growth of renewables and electric mobility in recent years. Most worryingly, China remains committed to supporting the coal industry while the rest of the world experiences a decline, and is now home to half of the world’s coal capacity. The CAT keeps its rating of China as “Highly insufficient”.

Economic uncertainty under COVID-19 has led to the government dropping its GDP target for the first time since 1990 and decrease its energy consumption per GDP target for 2020. Our analysis shows that the economic downturn from the pandemic has lowered China’s emissions trajectory despite its coal consumption, cement, and other heavy industries recovering faster than other sectors over the year.

In the last few years, there had been hopeful signs that China's CO2 emissions were flattening. However, CO2 emissions rose in 2018 and 2019, and we estimate 2020 GHG emissions will increase by 0.8% in our upper bound and decrease by 7.7% in our lower bound compared to 2019 levels, with most of the drop due to the pandemic.

China’s coal activities remain a large concern and are inconsistent with the Paris Agreement. It would need to phase out coal before 2040 under 1.5˚C compatible pathways, but it appears to be going in the opposite direction. After lifting a previous construction ban on new coal plants in 2018, China has rolled back policies restricting new coal plant permitting in each of the last three years. By mid-2020 China had permitted more new coal plant capacity than in 2018 and 2019 combined, bringing its total coal capacity in the pipeline to 250 GW, and brought 10 GW of new plants online. China is going against the global shift away from coal and now possesses roughly half of the world’s coal power capacity as well as coal-fired power plants in development.

China is the world’s largest financier and builder of both fossil fuel and renewables infrastructure worldwide. Of all coal-fired plants under development outside of China, one quarter, or 102 GW of capacity, have involved funding from Chinese financial institutions and/or companies. However, COVID-19 has – for now - curbed China’s investments on fossil infrastructure overseas, and its share of investment into foreign renewable projects has reached its highest-ever values.

China’s pandemic stimulus package will reach upwards of CNY four trillion (USD 565 billion) over 2020, approximately 4.5% of the country’s GDP, with figures expected to reach up to CNY 17.5 trillion by 2025 to support its New Infrastructure Plan. The recovery package is a clear display of China’s dedication to its existing leading industry strategies and targets to develop cutting-edge technologies and digital infrastructure. The package also includes budgets for electric mobility projects such as charging infrastructure and public transit as well as national high-speed rail. While this is an improvement from its post-GFC recovery package a decade earlier, where stimulus targeted hard infrastructure construction and caused a multi-year boom in emissions, the post-COVID-19 package still cannot be considered climate-friendly.

COVID-19 has increased uncertainty in the direction of China’s emissions to 2030. In the upper bound of China’s current policies under a COVID-19 scenario, the CAT’s projections show China’s GHG emissions would rise until 2030, although the rate of increase is projected to slow towards the end of the 2020s; in the lower bound, our analysis suggests it is possible that China’s emissions already peaked in 2019.

Consequently, China is on track to achieving its 2030 peaking target and overachieving its carbon intensity and non-fossil fuel share NDC targets without showing significant progression in its climate action. To date, many sectors have already rebounded to near pre-pandemic production levels, and emissions have responded accordingly. It is therefore critical that China uses further stimulus in Q3 and Q4 to clamp down on what may be the start of a new coal boom and dedicate recovery efforts to low-emissions infrastructure and clean energy projects, particularly ahead of finalising the 14th Five-Year Plan next year.

China’s emission projections from current policies have been revised downward during the ongoing COVID-19 pandemic. If implemented, current policies would result in GHG emission levels of 12.9-14.7 GtCO2e/year in 2030. With these policies, China is expected to achieve its 2020 pledge and 2030 NDC targets. Out of the three NDC targets, emissions expected from the carbon intensity target (emissions/GDP) have also been revised downward by -3 to -8% to 14.4-16.9 GtCO2e/ in 2030 due to new GDP projections in the ongoing global pandemic. China’s NDC and national actions are not yet consistent with limiting warming to below 2°C, let alone 1.5°C, unless other countries make much deeper reductions and comparably greater effort than China. During the EU-China summit in September 2020, the EU urged China to match its climate ambitions by peaking CO2 emissions by 2025, reaching net zero by 2060, and halting all investments into coal-fired power plants both domestically and abroad.

At the United Nations General Assembly a week later, President Xi Jinping partially answered the EU’s calls by announcing China would aim to peak emissions before 2030 and to achieve carbon neutrality before 2060. In addition, he announced that China will also enhance its NDC by adopting “more vigorous policies” and also called on other countries to pursue green economic recovery in a post-COVID-19 era. As the largest global GHG emitter and one of the most influential economies, China and its increased show of climate leadership is welcomed by the CAT. As China’s NDC targets have yet to be formulated and its carbon neutrality pledge yet to be officially announced, the CAT keeps its rating as “Highly insufficient.”

Before COVID-19, our analysis showed China’s current policy projections reaching total greenhouse gas (GHG) emissions between 13.7–14.7 GtCO2e/year in 2030. Our prior analysis also showed China achieving its 2020 and 2030 pledges. Under the most optimistic assumptions before COVID-19, the share of non-fossil fuels in China’s primary energy supply grows to 29% in 2030; under more pessimistic assumptions, the country’s share of non-fossil fuels grows to 23%. CO2 emissions continued to rise in both cases, albeit with low growth rates in the optimistic scenario. With the continuation of the global pandemic, China’s current policy projections to 2030 were revised downward by 1-9% or 0.2-1.2 GtCO2e/year.

China suffered many shocks in the first months of the pandemic. Satellite data showed pollution levels (NO2, PM2.5) were reduced by up to 30% in February 2020 compared to the same point in 2019, due to reduced industry and transport activity. Coal consumption was at its lowest point in four years, with demand for both energy and carbon-intensive industry activities (oil products, cement) also dropping heavily. As the economy contracted, the government dropped an annual GDP target for the first time since 1990 due to the high economic uncertainty, and banks were pressured to increase lending and hold up soft borrowing policies. By mid-2020, many sector indicators had largely recovered to pre-COVID-19 levels, including coal consumption, oil demand, cement, and construction demand. Deployment of renewables has even rebounded despite the ongoing phase-out of subsidies.

As COVID-19 impacts in China began to subside, international concerns were raised as to whether the government would follow previous economic stimulus strategies by supporting dirty industry and infrastructure. The Ministry of Finance has so far announced stimulus totalling more than CNY four trillion (USD 565 billion) in 2020 for infrastructure and transportation projects, much of which is in the form of local government special bonds.

Applications for new coal-fired power plant permits spiked in the following months, leading to over 40 GW of new proposed plants and 17 GW of new plants permitted before July in 2020. This is a clear discrepancy with global trends, as coal capacity outside China has been decreasing since 2018. While global coal generation fell by over 8% in the first half of 2020, China’s only fell by 2% meaning it generated over half of the world’s coal-fired electricity. Despite top-down statements discouraging coal plant projects from ministries and supervising agencies, a strong indication the government does not intend to stimulate the economy through carbon-intensive industries as it did in the post-financial crisis era of 2009; the trend reinforces other structural national policy issues around coal.

The government later issued plans to focus on “neo-infrastructure construction” including digital transformation, artificial intelligence, public transport, and electric vehicle projects. While China’s economic stimulus programme is an improvement from the financial crisis, the lack of direct guidance from Beijing on funding specific project types coupled with greater provincial influence on expenditure means a “Green Deal” for China is unlikely.

China is implementing many significant policies in multiple sectors that have implications for climate change, yet policy direction still implies a medium-term fossil fuel lock-in. While China’s 13th Five-Year Plan (FYP) (2016-2020) stipulates a maximum 58% share of coal in national energy consumption and 15% share of primary energy consumption from non-fossil sources in 2020, the country sees continued expansions of fossil infrastructure.

The 14th FYP, due next year, is expected to carry new caps for coal and benchmarks for renewables; the energy policies it contains could have the largest medium-term implications for the global energy portfolio from any single legislative document. The government issued a draft of its first-ever Energy Law in 2020, which highlights the importance of energy efficiency and renewables without making concrete commitments. China’s new nationwide emissions trading system (ETS), starting in 2020, should, in theory, accelerate the phase-out of inefficient coal-fired power plants, although the governing ministry has recently proposed loosening carbon-intensity benchmarks.

In the last two years, the Chinese government had begun to phase out subsidies for solar and wind energy projects, aiming to have them completely removed by 2021. In a race to connect renewable projects to the grid before the subsidy deadline at the end of 2020, the growth in solar and wind installations has kept up with - and even surpassed – the installation rate in 2019, despite COVID-19 setbacks for grid connections. The government had also intended to phase out subsidies and tax exemptions for new energy (electric) vehicles this year, but has decided to extend them through 2022 after the sector was hit hard in the pandemic. China has signalled further investments in electric mobility and aims to increase the market share of new energy vehicles to 20% in 2025, in an apparent prioritisation of this sector in economic recovery.

Further analysis

Latest publications

Stay informed

Subscribe to our newsletter