China

Country summary

Overview

China is the world’s largest greenhouse gas emitter, and its actions both at home and abroad have an enormous impact on global greenhouse gas emissions. Discouragingly, increased fossil-fuel consumption drove an estimated 2.3% increase in Chinese CO2 emissions in 2018, a second year of growth after emissions had appeared to level out between 2014 and 2016.

China is simultaneously, and almost paradoxically, the world’s largest consumer of coal and the largest solar technology manufacturer, and the choice it makes between the technology of the past versus the future will have a lasting effect on the world’s ability to limit warming to 1.5oC.

The IPCC Special Report on 1.5°C found that coal needs to exit the power sector by 2050 globally if warming is to be limited to this level, and efforts by China to reduce coal in the next few years will be critical to this. In global cost-optimal, Paris Agreement-consistent pathways, China phases out coal by 2040. China’s emissions, like the rest of the world’s, need to peak imminently, and then decline rapidly. Discouragingly, China started construction of 28 GW of new coal-fired power capacity in 2018 after a previous construction ban was lifted, bringing its total coal capacity under construction to 235 GW.

With current policies, China’s greenhouse gas emissions are projected to rise until at least 2030. Under optimistic renewables growth assumptions, energy-related CO2 emissions could level off over the next few years, but these emissions continue to grow in our upper-bound scenario.

China’s actions abroad will also have an important impact on future global greenhouse gas emissions, and China is financing and building both fossil-fuel and renewables infrastructure worldwide. Of all coal plants under development outside of China, one quarter, or 102 GW of capacity, have committed or proposed funding from Chinese financial institutions and companies. That’s roughly double Germany’s current coal capacity.

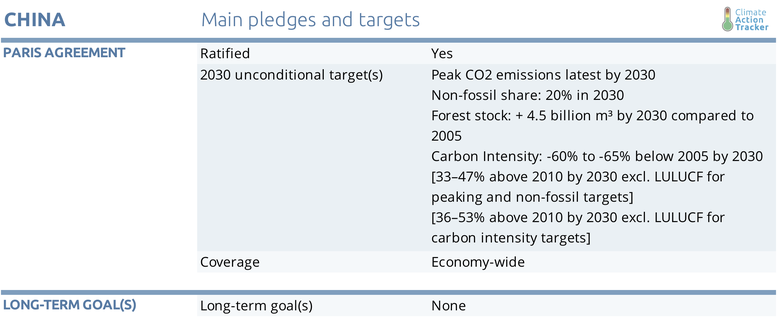

China is on track to meet or overachieve its 2030 Nationally Determined Contribution (NDC) , which the CAT rates “Highly insufficient.” China’s NDC is not ambitious enough to limit warming to below 2°C, let alone to 1.5°C as required under the Paris Agreement, unless other countries make much deeper reductions at comparably greater effort. Under current policies, China is also likely to achieve its 2020 pledge. Given that China is on track to achieve or overachieve its climate targets, its next step could be to set an example by submitting a strengthened NDC to the Paris Agreement by 2020. (For details on China’s NDC, see “pledges and targets” section). China has indicated that it is working on updating its NDC.

China has policies in place to reach the targets set in its NDC. If reached, they would result in GHG emission levels of roughly 14.4–16.6 GtCO2e/yr in 2030. The NDC carbon intensity targets on their own would lead to 2030 emission levels of 14.7–16.6 GtCO2e/yr. As the intensity targets are likely to be reached automatically if the non-fossil targets are achieved, and our rating is based on achieving all NDC targets, we do not address the intensity targets separately here. (China’s intensity target on its own would also result in a “Highly insufficient” rating.)

However, this range also implies that China’s NDC and its national actions are not yet consistent with limiting warming to below 2°C, let alone 1.5°C unless other countries make much deeper reductions and comparably greater effort than China. We therefore rate the emission levels estimated for 2030 resulting from the most ambitious aspects of the NDC as “Highly insufficient.”

Our analysis shows that China will achieve both its 2020 and 2030 pledges. Current policy projections show that total greenhouse gas emissions will rise to between 14.4–15.8 GtCO2e/yr in 2030. Under the most optimistic assumptions where the share of non-fossil fuels in primary energy supply grows to 30% in 2030, CO2 emissions (including process emissions) could flatten between now and 2030, under more pessimistic assumptions where the share of non-fossil fuels grows only to 21%, they will continue to rise, reaching between 10.8 and 12.2 GtCO2/yr in 2030.

China is implementing significant policies in multiple sectors to address climate change, and also aiming to restrict coal consumption. China’s 13th Five-Year Plan stipulates a maximum 58% share of coal in national energy consumption by 2020 (NDRC, 2016), among other energy related targets. China is implementing an emissions trading system, with first trades expected in 2020, and has also announced a mandatory renewable energy certificate scheme that sets targets for renewable energy for each province individually.

However, the Chinese government abruptly reduced subsidies for solar projects in 2018 and lifted a two-year ban on new coal-fired power plant construction.

China has not yet implemented sufficient policies addressing non-CO2 GHG emissions (CH4, N2O, HFCs etc.) Under current policy projections, 23 – 25% of China’s GHG emissions in 2030 will be non-CO2 emissions. As the NDC acknowledges that addressing these gases is important, further policy action may be expected to address non-CO2 emissions as well.

Over 1.1 million electric vehicles were sold in China in 2018—a 2018 market share of 4.2% - achieving an aim of the transport section of the formerly called “Made in China 2025” policy initiative two years early. (Chinese officials have backed away from the “Made in China 2025” name over the past months after international criticism, but the underlying initiative appears to still stand). China has both subsidies and tax exemptions that apply to new energy vehicles, which are expected to make up 10% of annual sales in 2019 and 12% in 2020.

The China 6 emissions standards for passenger vehicles that go into effect on July 1, 2020 will be one of the most stringent emissions standards in the world. Its new emissions standards for heavy duty vehicles, once in place, will be in line with standards in the US, Canada, Japan, and EU, although they apply to atmospheric pollutants like NOx and particulate matter, but do not regulate CO2 specifically.

Further analysis

Latest publications

Stay informed

Subscribe to our newsletter