Japan

Current Policy Projections

Economy-wide

Currently implemented policies will lead to emissions levels of between 1,230 and 1,250 MtCO2e/yr (2–3% below 1990 levels) in 2020 and 1,040 and 1,100 MtCO2e/yr (14–18% below 1990 levels) in 2030, excluding LULUCF. The results indicate that Japan is on track to meet its NDC target under current policies, although the uncertainty range of emissions remains fairly large due to the status of nuclear power.

The range of the projections depends partly on the future of nuclear power. The lower end projection is from a scenario in which all nuclear reactors that applied for restart as of November 2019 would be approved and the difference in nuclear power generation compared to the IEA WEO 2019 Current Policies Scenario (IEA, 2019) is balanced by coal and gas power.

The upper end projection, by contrast, is from a scenario where there is no additional nuclear power generation in 2020 and 2030, except for 15 reactors (plus one under construction) which are approved for restart after the necessary additional safety measures are taken, and the electricity supply gap is filled by renewables and fossil-fired power (coal and gas), proportional to the technologies’ shares for 2030 projected in the WEO 2019.

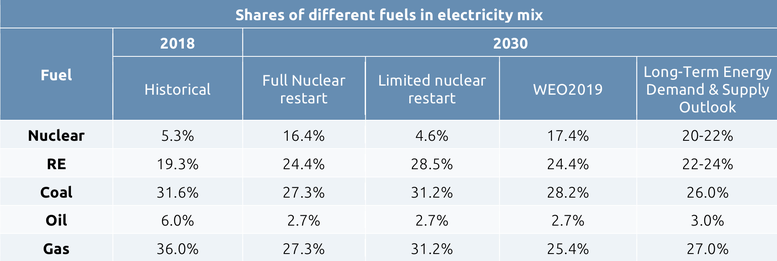

The table below illustrates the fuel mix in the power sector in 2018, and under different assumptions for our projections, in comparison to the WEO 2019. Our upper end projection of renewable electricity share in 2030 (28.5%) is higher than that projected in the WEO 2019’s Current Policies Scenario (24.4%).

Before the recently-initiated transformation of the electricity supply sector, Japan had already introduced effective policies for energy efficiency in transport, industry, and buildings. One longstanding policy is the Energy Conservation Act, the main energy efficiency law implemented in 1979. To achieve the energy savings target under the NDC, an amendment to the Energy Conservation Act was enforced in 2018 (METI, 2018a). The amendment establishes a new certification system which allows for an inter-business initiative to enhance systemic energy savings, in addition to energy savings at individual operator level, and ensures the coverage of e-commerce retailers under the Act.

Other policies include the Global Warming Tax, an upstream environmental tax, with a maximum price of JPY 289 (about USD 3) per tCO2 in 2016, which is low. The government expected the impact to be 6–24 MtCO2/yr by 2020, on a baseline of 1,115 MtCO2/yr for energy related emissions (MOEJ, 2017a). There is no ex-post impact assessment on this tax scheme available to date.

Energy supply

After the 2011 Great East Japan Earthquake and tsunami, the Japanese Government revised its energy policy in which the country committed to reducing its reliance on nuclear energy. In 2011, all nuclear power plants stopped operating and were not allowed to restart until they complied with higher safety standards. The 2014 Basic Energy Plan called for a resumption of nuclear energy (METI, 2014). As of November 2019, 25 reactors in 15 nuclear power plants have applied for a restart (and two in construction applied for operation) under new, more stringent safety standards—15 reactors with a total of 15.4 GW have passed the safety examination and have been approved for restart (under the condition that the plans for the construction work are approved by neighbouring local governments and the required safety measures are properly installed), of which nine are currently in operation (JAIF, 2019).

In 2018, the Japanese government adopted its new Basic Energy Plan (METI, 2018d). The new plan provides no vision nor strategy on how Japan can go beyond its 22–24% by 2030 renewable electricity target, which is likely to be achieved with existing policies. Instead, it focuses on whether new nuclear reactors could be constructed toward 2050 and how to reduce the economic costs resulting from the renewable electricity support scheme. A more positive sign is that the documents refer to renewables as “main power sources”—this suggests an important policy shift from the current 2014 Basic Energy Plan’s “important low-carbon and domestic power source”. Nuclear power remains as an “important power source” in the 2018 plan.

The electricity mix for 2030 assumed in Japan’s NDC is based on the 2015 Long-Term Energy Demand and Supply Outlook. The Outlook foresees that 20–22% of electricity will be supplied by nuclear energy, 22–24% by renewable energy and the remaining 56% by fossil fuel sources. The 2018 Basic Energy plan reiterated the 2015 Outlook target. This strategy stands in strong contrast to what would be compatible with a long-term, 2°C‑compatible strategy, let alone a 1.5°C strategy.

Two important aspects highlight why this is the case:

First, the energy strategy foresees a relatively large share of base load power plants (i.e. nuclear and coal fired power plants) of 46–48% in 2030 of total electricity production. Decarbonisation strategies in most countries foresee a significant increase of variable renewable energy resources, which requires a paradigm shift in how energy systems are structured and managed, and will increase their complexity. Such shifts take time and require the development and rollout of new technologies such as differently designed distribution networks (see e.g. (Bloomberg, 2015)).

Second, in the Outlook, fossil fuel power plants would play an important role in Japan’s energy mix in 2030 (56%), with 26% of total electricity generation expected to come from coal-fired power plants. This share could increase even further as the strong public opposition to nuclear power in the wake of Fukushima brings a challenge to predict the future course of nuclear power. There have already been a few district court rulings to halt the operation of the restarted reactors (JAIF, 2018). We project that the coal share would remain at the current 32% in 2018 if the nuclear reintroduction fails and without a further push for renewables.

For coal-fired power, a total of 13 GW, that would together emit around 75 MtCO2e annually, is currently being planned (Kiko Network, 2019). The Japanese government has also shied away from committing to completely phase out coal-fired power generation even in the long-term; the recently-published long-term strategy only commits to phasing out inefficient coal-fired power plants and reducing reliance on fossil fuel-fired power as much as possible.

It is uncertain how much of the 13 GW of new capacity (none of which is CCS ready) currently being planned would actually be built because new coal-fired power plant constructions are becoming increasingly difficult in Japan. One reason is economic – in April 2018, J-POWER, an electric utility, cancelled its plans for two coal fired power plants due to decreasing electricity demand in the region (J-POWER, 2018).

Similarly, in January 2019, two additional plants were cancelled for “being uneconomic” by a business consortium of major energy companies (Kyushu Electric Power, 2019). Another reason is the stricter environmental regulation: the mandatory environmental impact assessment (EIA) process, under which the consistency with the NDC achievement is an important criterion, has also been functioning to some extent as a safeguard against additional construction of new coal-fired power plants.

The environment minister’s opinion statements following the EIA results have significant importance in the planning process, even though the final say remains with METI. Some that received negative EIA results in recent years were forced to cancel (e.g. Ichihara and Soga) (Chugoku Electric Power, 2018; Kanden Energy Solution, 2017), while others (Taketoyo No. 5 and Misumi No. 2) were ultimately built (MOEJ, 2018; Oi, Ito, & Tanimoto, 2017).

In March 2019, MOEJ announced three new actions towards decarbonisation of the power sector (MOEJ, in Japanese), the most significant of which being the stricter enforcement of Environmental Impact Assessments (EIAs) – cancellation requests would be issued to new coal-fired power plant construction plans without the following: (i) justification for the need for the plant other than economic feasibility, or (ii) a clear explanation of the role the new power plant would play towards achieving the 2030 electricity mix target. Coal-fired power plants already under construction will not be affected by this action.

Japan has also been a major funder of coal-fired power plants overseas, alongside China and South Korea (CoalSwarm, 2018); it has even included coal-power plant support in its climate finance commitments in the past (Nakhooda et al., 2013). While Japan’s public finance institutions haven’t changed their stance on coal, the private sector is showing a sign of change.

There has been a series of announcements from major banks, insurance companies and trading companies since May 2015 to shift away from investing in coal power plants (Renewable Energy Institute, 2018). While many of the announcements do not rule out all types of investment into coal-fired power plants, these are important signs that the private sector is taking climate change mitigation and its implications on business into serious consideration.

Renewable electricity generation has grown steadily in recent years. In 2012, the Renewable Energy Act was introduced to support Japan’s stated NDC renewable electricity share target of 22–24% by 2030. It institutes a feed-in tariff (FIT) and general funding for distribution networks. The FIT has provided very favourable rates, particularly for solar PV, which led to a large increase in PV installations. The share of renewable energy in total electricity generation has increased considerably from 10% in 2010 to 16% in FY2017 (IEA, 2018). However, the generous PV tariff rates has meant significantly increased costs particularly for households, and many FIT-certified companies also purposefully delayed installation of PV systems until prices dropped. Also no significant growth was observed for other renewables, such as wind and geothermal (Renewable Energy Institute, 2017a).

Effective from April 2017, the Ministry of the Economy, Trade and Industry (METI) revised the FIT scheme for the first time with a stated intention of avoiding a “solar bubble” and to achieve a more balanced growth of renewable energy while minimising the costs (METI, 2016). An important new instrument is the auctioning system for solar PV installations larger than 2MWe. The auction has been conducted four times to date, and has shown some success in lowering the FIT prices, yet often resulted in the insufficient new capacity contracted due to a lack of bidders (Bellini, 2019). The government is now planning to further revise the FIT scheme largely by shifting it into a feed-in-premium (FIP) scheme, a trend observed in several European countries, such as Germany and France, which spearheaded the introduction of FIT policy in the early 2000s (METI, 2019b).

March 2017 also saw a last-minute rush of biomass project applications before the tariff rates were lowered – the total biomass capacity approved under the FIT scheme to date amounts up to more than 12 GW (METI, 2017b). If all the approved capacity is implemented, though unlikely, the total biomass capacity would reach 16 GW (METI, 2017b), which is more than double the amount expected under the 2030 electricity mix target (Government of Japan, 2017). Many of the approved projects plan to co-fire imported palm oil with coal, raising concerns about the overall environmental integrity of Japan’s renewable energy policy (METI, 2017b; Renewable Energy Institute, 2017b). Although it is technically possible to produce palm oil with low indirect land use-change (ILUC) risks (Peters et al., 2016), an increased use of palm oil will likely result in strong ILUC emissions increase, even when the palm oil is accompanied by a strong sustainability certificate (Valin et al., 2015).

Another push was made to support the development of offshore wind power by introducing the Development of Power Generation Facilities Using Maritime Renewable Energy Resources in April 2019 (METI, 2019a). The government has so far identified 11 areas as potentially suitable for developing offshore wind farms and announced that wind and geological surveys will be immediately carried out in four of the areas (METI, 2019c).

Transport

CO2 emissions (including indirect emissions from electricity use) from the transport sector accounted for 18% of Japan’s total energy-related CO2 emissions in 2017 (GIO, 2019). Compared to 1990, the emissions in this sector have increased by 3%, but have been on a decreasing trend since 2001 and the emissions have since reduced by 19% (GIO, 2019). This trend stands out from the rest of the Annex I countries (excluding those with economies in transition), which showed an average reduction of 0.6% over the same period (UNFCCC, 2018).

Regarding vehicle decarbonisation, the current government target for ‘new generation’ vehicles (including hybrids, plug-in hybrids, battery electric vehicles, fuel cell electric vehicles, as well as ‘clean diesel’ vehicles and gas-powered vehicles) has been set at 50-70% of new sales by 2030 (METI, 2018d). On the fuel economy of passenger vehicles, Japan has been one of the best performers over the last few decades with the average CO2 intensity of 115 gCO2/km (normalised to NEDC) (ICCT, 2018), but no post-2020 performance standard has yet been set.

For the longer term, a panel under METI compiled an interim report on the long-term strategy for car manufacturing (METI, 2018c). This document included targets of reducing tank-to-wheel CO2 emissions by 80% below 2010 levels by 2050 for all new vehicles produced by Japanese car manufacturers and 90% by 2050 for new passenger vehicles, with the latter assuming a near 100% share of electric vehicles (including hybrids, plug-in hybrids, battery electric vehicles and fuel cell electric vehicles).

While these targets are described in the strategy document to be consistent with the Beyond 2°C scenario of the IEA Energy Technology Perspectives 2017 report (IEA, 2017), it is not consistent with the benchmark for 1.5°C identified by the Climate Action Tracker analysis (Kuramochi et al., 2018), i.e. last fossil fuel passenger car sold by 2035, because the expected shares of conventional and plug-in hybrids under the proposed targets are not clear.

While the proposed targets are not as ambitious as those set in some European countries (e.g. Norway 2025, France 2040 and the UK 2040) (DEFRA & DfT, 2017; Ewing, 2017; Staufenberg, 2016), Japan will become the largest car manufacturing nation (headquarters-based) to date to set a long-term phase-out strategy for conventional internal combustion engine (ICE) vehicles. The final strategy document will be based largely on this interim report. The outcomes of this METI panel are significant not only because of the ambition of the proposed targets, but also because the panel members include CEOs of major car manufacturers (Toyota, Nissan, Honda and Mazda).

Accordingly, the new fuel economy standards were set for trucks and buses to improve by 13-14 % by 2025 compared to the 2015 levels, and for passenger cars to improve by 32% by 2030 compared to the 2016 levels (METI; MLIT, 2019a, 2019b).

Industry

CO2 emissions from the industry sector (including indirect emissions from electricity use as well as emissions from industrial processes) accounted for 39% of Japan’s total energy-related CO2 emissions in 2017 (GIO, 2019). Within the sector, the iron and steel, the chemical, and the cement industries are the three largest emitters, which respectively emitted 36%, 13% and 6% of industrial emissions in 2017 (GIO, 2019). In 2017, emissions in the sector have reduced by 19% below 1990 levels (11% below 2005 levels) (GIO, 2019). A progress report for 2017 (Keidanren, 2019) shows that the industry CO2 emissions from the member companies of Keidanren, the most influential business association in Japan, including indirect emissions from electricity use in 2017 was 11.2% lower than in 2015; the same report also reports that the large majority of the emissions reductions (8.7%) was due to the changes in industrial activity levels.

The main GHG emissions reduction effort in the Japanese industry is Keidanren’s Commitment to a Low-Carbon Society (Keidanren, 2015), a voluntary action plan which has monitoring obligations under the Plan for Global Warming Countermeasures (MOEJ, 2016b).

In November 2018, the Japanese Iron and Steel Federation (JISF) published a long-term decarbonisation vision, which draws global emissions pathways reaching zero in 2100 to achieve the 2°C temperature goal (JISF, 2018). While the JISF should be commended for developing such a strategy document, the document perhaps intentionally misinterprets the Paris Agreement’s long-term temperature goal as “2°C” and hence developing emissions pathways that are not ambitious enough for the Paris Agreement’s “well below 2°C” / 1.5°C target.

As of November 2019, no such concrete visions beyond 2030 have been developed by the other major emitters such as the chemical or cement industries. However, it is worth mentioning that in 2017 the cement industry reduced its emissions by 32% below 1990 levels, compared with much smaller reductions achieved in the iron and steel (6% reduction) and the chemical (5%) industries (GIO, 2019).

Buildings

CO2 emissions (including indirect emissions from electricity use) from the commercial and residential building sectors together accounted for 33% of Japan’s total energy-related CO2 emissions in 2017 (GIO, 2019). Compared to 1990, the emissions in these two sectors have increased by 60% and 42%, respectively (GIO, 2019). Although these significant increases are partially attributable to the increased electricity CO2-intensity post-Fukushima, there’s an urgent need for strengthened action on the demand side in the building sector.

An important development here is the revised building energy efficiency standards that entered into force on April 2017 under the Buildings Energy Efficiency Act (MLIT, 2016). Under the revised standards, new non-residential buildings larger than 2000 m2 floor area must meet the energy efficiency standards, and the plan is that all new builds including residential buildings must meet the standards from 2020 onward. The lower limit was accordingly revised to 300 m2 in May 2019 (MLIT, 2018). This is a major step forward in improving energy efficiency in the building sector because the standards were not previously mandatory: in 2015, the compliance rate for residential buildings was 46% (MLIT, 2017). It should, however, also be noted that the effective stringency of the standards for residential buildings is the same as the previous 1999 standards, which is lax compared to those in other developed countries, such as France, Germany, Sweden, the UK, and the United States (MLIT, 2013).

Under the 2014 Basic Energy Plan, and remained unchanged in the 2018 version, Japan also aims to reduce the average net primary energy consumption of newly constructed buildings and houses to zero by 2030 (METI, 2014). Japan’s targets for Zero Energy Houses (ZEHs: for residential buildings) and Zero Energy Buildings (ZEBs: for commercial buildings) may not be as ambitious as the EU Energy Performance of Buildings Directive (European Parliament and the Council of the European Union, 2010), which requires all new buildings to be nearly zero energy by the end of 2020 (European Parliament and the Council of the European Union, 2010), even though the definitions of “near zero energy” vary across EU Member States (BPIE, 2016). The share of ZEHs and “Nearly -ZEHs” (more than 75% reduction in net primary energy consumption) in total new residential buildings in 2017 was 10.5% (Sustainable open Innovation Initiative, 2018b), compared to the 50% target for 2020 also set in the 2014 Basic Energy Plan. The deployment of ZEBs is still in an initial phase (Sustainable open Innovation Initiative, 2018a).

F-gases

Japan aims to reduce F-gas emissions through enhanced management of in-use stock and regulating consumption levels. On the management of in-use stock, under the Plan for Global Warming Countermeasures (MOEJ, 2016b), Japan aims to increase the recovery rate of hydrofluorocarbons (HFCs) from end-of-use refrigeration and air conditioning equipment up to 50% by 2020 and 70% by 2030. The Act on Rational Use and Proper Management of Fluorocarbons (“F-gas Act”; last amended in 2013) addresses this, but the recovery rate has stagnated: the recovery rate of refrigerants in 2017 was only 38% (METI; MOEJ, 2019). To resolve this, the F-gas Act has been further amended (the bill passed the Diet in May 2019 and will enter into force in April 2020) (House of Councillors, 2019), including several penalty and obligatory measures to increase the F-gas recovery rates up to the targeted 50% by 2020 (MOEJ, 2019; Yoshimoto, 2019).

To meet the HFC reduction target under the NDC and the targets under the Kigali Amendment of the Montreal Protocol, the Ozone Layer Protection Act was amended in 2018 and measures took effect in April 2019. The amendment sets a ceiling on the production and consumption of HFCs, establishes guidelines to allocate production quota per producer as well as regulates exports and imports (METI, 2018b). The consumption levels are projected to be below the Kigali cap at least until 2029, when the Kigali cap lowers significantly. Since there is some time lag between consumption and emission, we assume that the amended Ozone Layer Protection Act will not affect HFC emission levels up to 2030 (METI, 2018b).

Further analysis

Latest publications

Stay informed

Subscribe to our newsletter