Japan

Assumptions

Historical emissions

Historical emissions data were obtained from the UNFCCC GHG inventory and cover the period from 1990 to 2018 (UNFCCC, 2020).

Pledges and targets

2020 pledge

Target emission level for 2020 was calculated from 2005 emissions data from the GHG inventory data submitted to the UNFCCC in 2020 (UNFCCC, 2020). We calculated Japan's LULUCF accounting quantities in 2020 for afforestation, reforestation and deforestation based on the accounting rule under the second commitment period of the Kyoto Protocol. Net removal by forests (38 MtCO2e/year), revegetation (1.2 MtCO2e/year) and agricultural soil sinks (7.7 MtCO2e/year) is taken into account for 2020 (Government of Japan, 2019a).

NDC

The target for 2030 was calculated using Japan’s NDC and the UNFCCC GHG inventory data submitted in 2020 (UNFCCC, 2020).

Long-term goal (2050)

Since the 2050 target does not specify the reference year, we calculate the emission levels using 1990 and 2005 emissions as references.

Current policy projections

Energy-related CO2 emissions

For the analysis of current policy projections, we used the IEA World Energy Outlook (WEO) 2019 Current Policies Scenario (CPS) (IEA, 2019), which covers various climate related policies implemented as of 2019 and their impact on energy-related CO2 emissions, as a basis. The GDP in absolute terms for 2030 assumed in the IEA WEO 2019, based on World Bank and International Monetary Fund estimates, is 16% lower than that assumed in the NDC.

The IEA WEO 2019 foresees a relatively large share of electricity generation from nuclear energy in 2030 (17%). While this is overachieved by the current assumptions of the government (Basic Energy Plan), it is not completely supported by the rate of restart of currently shut down nuclear power plants. We explored “low emission” and “high emission” cases with varying shares of renewable and nuclear power generation. For both cases we assumed that the recent announcement on the phasing out of old and inefficient coal-fired power plants would be fully implemented (METI, 2020a, 2020g). Based on our assessment of the announcement, it was estimated that the share of coal in total electricity generation in 2030 would be kept at 26% as targeted under the NDC.

In the low emissions case, we assumed that:

- Full nuclear restart (same assumptions as in the December 2019 update): all 25 nuclear reactors (plus two allowed to resume construction) that have applied for restart as of August 2020 will be approved, restart by 2025 and complete their extended 60-year lifetime (with an average 6500 hours/year operation, comparable to about 7000 hours/year assumed for 2030 in IEA WEO 2019 scenarios). For the two reactors under construction, the Ohma reactor is assumed to start operating in 2026 and the Shimane No. 3 reactor in 2021 (Renewable Energy Institute, 2020);

- Coal and oil power shares kept to the NDC target (coal: 26%, oil: 3%);

- Renewable electricity generation reaches 301 TWh/year in 2030 as estimated by Asano and Obane (2020), which would lead to a 27.5% share according to our own calculations using the total generation projection under the WEO 2019 CPS), exceeding the NDC target;

- Natural gas power fills the remaining gap, resulting in 25% compared to 36% in 2018.

In the high emissions case, we assumed that:

- Limited nuclear restart with low capacity factor (same assumptions as in December 2019 update): only 15 reactors that have been allowed to restart as of August 2020, after additional safety measures were implemented, would be in operation up to 2030 (some with a 60-year extended lifetime) but at a much shorter 3250 hours/year operation on average, taking into account the possible court cases and unplanned inspections.

- Coal power share kept to 26% and oil to 3% as per NDC target;

- Renewable energy share reaches 24% (as per IEA WEO 2019 Current Policies Scenario, meeting the upper range of the NDC target);

- Gas power reaches 40% to fill the remaining gap.

We also revised the average CO2 emission factor of electricity from coal-fired power plants following the announcement to phase out old and inefficient plants. For 2030, we assume a 5% reduction in average CO2 emission factor per kWh in 2030 compared to 2018 levels as a result of phasing out old and inefficient coal-fired power plants. This estimate is based on the following considerations:

- Ultra-supercritical (USC) and Integrated Gasification Combined Cycle (IGCC) plants account for roughly 40% of total coal power generation today (authors’ estimate for 2017 based on the USC and IGCC capacities presented above, 80% capacity factor and the IEA 2019 World Energy Balances);

- Existing USCs are roughly 10% to 15% more efficient than the non-USC (43%–45% compared to 37%–41%, based on the Japan Coal Plant Tracker database). New USCs under construction or planning are expected to be even more efficient;

- Considering that some non-USCs remain in 2030, the share of coal-fired autogeneration remains constant, and that the IEA WEO Current Policies Scenario on which the CAT projections are based includes power generation from coal-derived products, we estimated that, on average, the CO2 emission factor will improve by about 5%.

After the recalculation of the 2030 electricity mix, CO2 emissions were calculated—CO2 emission factors per technology were assumed to be identical to those in the WEO 2019 CPS. Finally, the growth rates of energy-related CO2 emissions up to 2030, recalculated based on the IEA WEO 2019 CPS, were applied to the 2018 historical energy related CO2 reported in the national GHG inventory report submitted to the UNFCCC.

We do not use “With measures” emissions projection provided in Japan’s Fourth Biennial Report (BR4) as reference. The BR4 “With measures” scenario is an NDC achievement scenario, which takes into account, not only the policy measures already implemented in FY2013, but also those to be implemented by FY2030 (Government of Japan, 2017). The assumed GDP growth rates are also very high—on average 1.7% per year for 2013-2030 based on the government's growth target (METI, 2015).

Other emissions

For the emissions of non-energy CO2, CH4 and N2O, we linearly extrapolated historical trends of two different emission intensity indicators: per unit GDP and per capita, into future years. For both intensity indicators, the historical trends observed between 2007 and 2018 were linearly extrapolated to 2030. The pre-COVID-19 GDP growth projections up to 2030 were taken from IEA (IEA, 2019) and population projections were taken from UN Population Prospects (medium fertility variant) (UN DESA 2019). The 2030 projections using different emission intensity indicators were similar.

For F-gas emissions, the expected impacts of the Act on Rational Use and Proper Management of Fluorocarbons (2013 amendment) to enhance management of F-gas use and the Ozone Layer Protection Act (‘F-gas Act’, 2018 amendment) to regulate the production and imports of F-gases to comply with the Kigali Amendment were also considered. Our calculations show that the HFC emission levels are projected to fall far short of the levels targeted under the NDC (Government of Japan, 2015; MOEJ, 2012; MOEJ & METI, 2014).

As described in the current policy projections section, the F-gas Act has not been successful in improving the recovery rate of refrigerants from end-of-life refrigeration and air conditioning equipment in 2017 was only 38% (METI; MOEJ, 2019). Based on the historical trends reported in METI and MOEJ (METI; MOEJ, 2019), we assume that the HFC recovery rate will not improve over time (40% for 2020-2030). We also assume that the leakage rates for the in-use stock will also not improve under current policies. Regarding the 2018 amendment of the Ozone Layer Protection Act, the business-as-usual consumption levels are projected to be below the Kigali cap at least until 2025 (METI, 2018b); the Kigali cap for Japan becomes significantly lower only in 2029. Since there is some time lag between consumption and emissions, we assume that the amended Ozone Layer Protection Act will not affect the HFC emission levels up to 2030.

The point of departure for the revised F-gas emission projections is the business-as-usual (BAU) projections provided in the background document of the Plan for Global Warming Countermeasures (MOEJ, 2016a)–the Plan projects F-gas emissions to increase from 39 MtCO2e/year in 2013 to 77 MtCO2e/year in 2030 under a BAU scenario. The three measures: (i) enhanced recovery from end-of-life equipment, (ii) avoidance of leakage from in-use equipment, and (iii) switch to lower GWP F-gas and non-F-gas refrigerants are expected to reduce emissions to the NDC target level of 29 MtCO2e/year in 2030. In our assessment, we assume that only part of the NDC implementation plan, i.e. the switch to lower GWP F-gas and non-F-gas refrigerants, would be achieved.

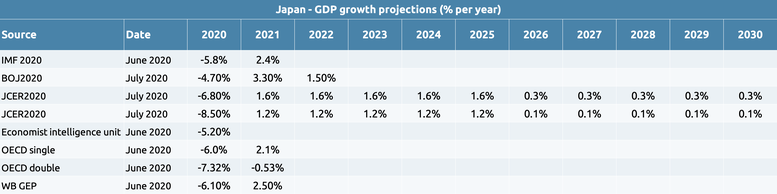

COVID-19 impact

We applied a novel method to estimate the COVID-19 related dip in greenhouse gas emissions in 2020 and the deployment through to 2030. The uncertainty surrounding the severity and length of the pandemic creates a new level of uncertainty for current and future greenhouse gas emissions.

We first update the current policy projections using most recent projections, usually prepared before the pandemic. We then distil the emission intensity (GHG emissions/GDP) from this pre-pandemic scenario and apply to it most recent GDP projections that take into account the effect of the pandemic. To capture a wide range, we compiled GDP growth projections from IMF (2020–2021) (IMF, 2020), OECD (two scenarios for 2020–2021) (OECD, 2020a, 2020b), World Bank (2020–2021) (World Bank, 2020), Bank of Japan (2020–2022) (Bank of Japan, 2014), Economist Intelligence Unit (2020) (The Economist Intelligence Unit, 2020) and Japan Center for Economic Research (JCER; 2020–2030) (Kobayashi et al., 2020b, 2020a). All projections considered in the analysis were published after June 2020. For the years following the projection period of the aforementioned forecasts up to 2030, we use the GDP growth rates that were used as a basis for the original pre-pandemic current policy scenario, i.e. projections from the IEA WEO 2019. For 2030, the upper bound GDP projection was based on the Bank of Japan forecast and the lower bound projection was based on the JCER’s “Nightmare scenario”.

Global Warming Potential values

The CAT uses Global Warming Potential (GWP) values from the IPCC's Fourth Assessment Report (AR4) for all its figures and time series. Assessments completed prior to December 2018 (COP24) used GWP values from the Second Assessment Report (SAR).

Further analysis

Latest publications

Stay informed

Subscribe to our newsletter