South Africa

Policies & action

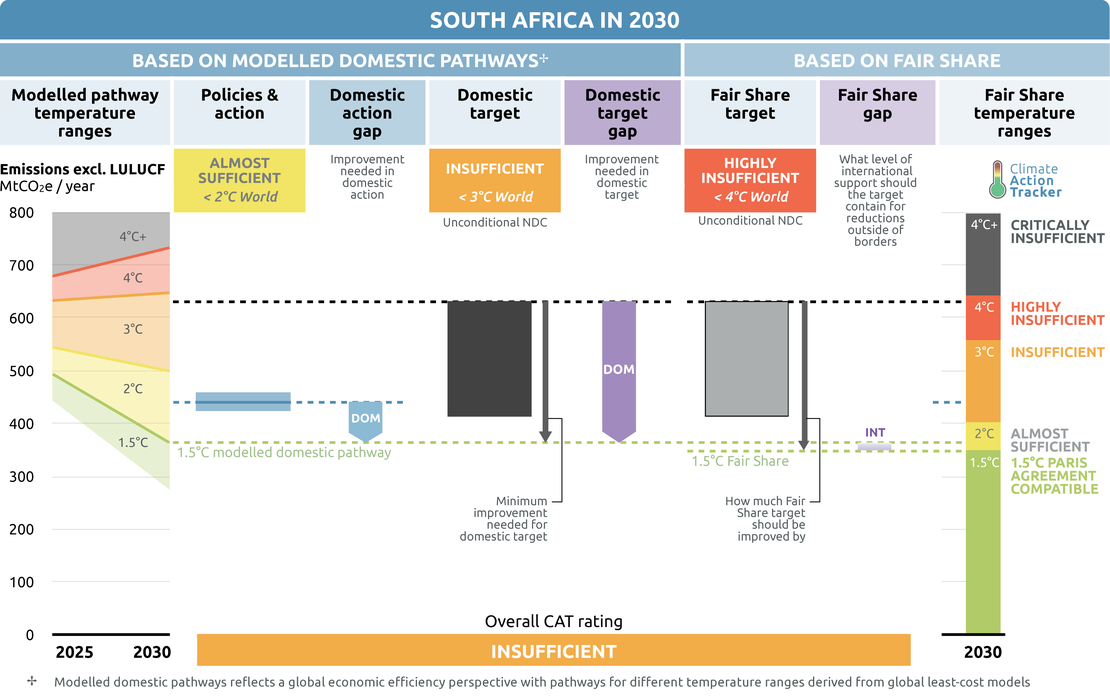

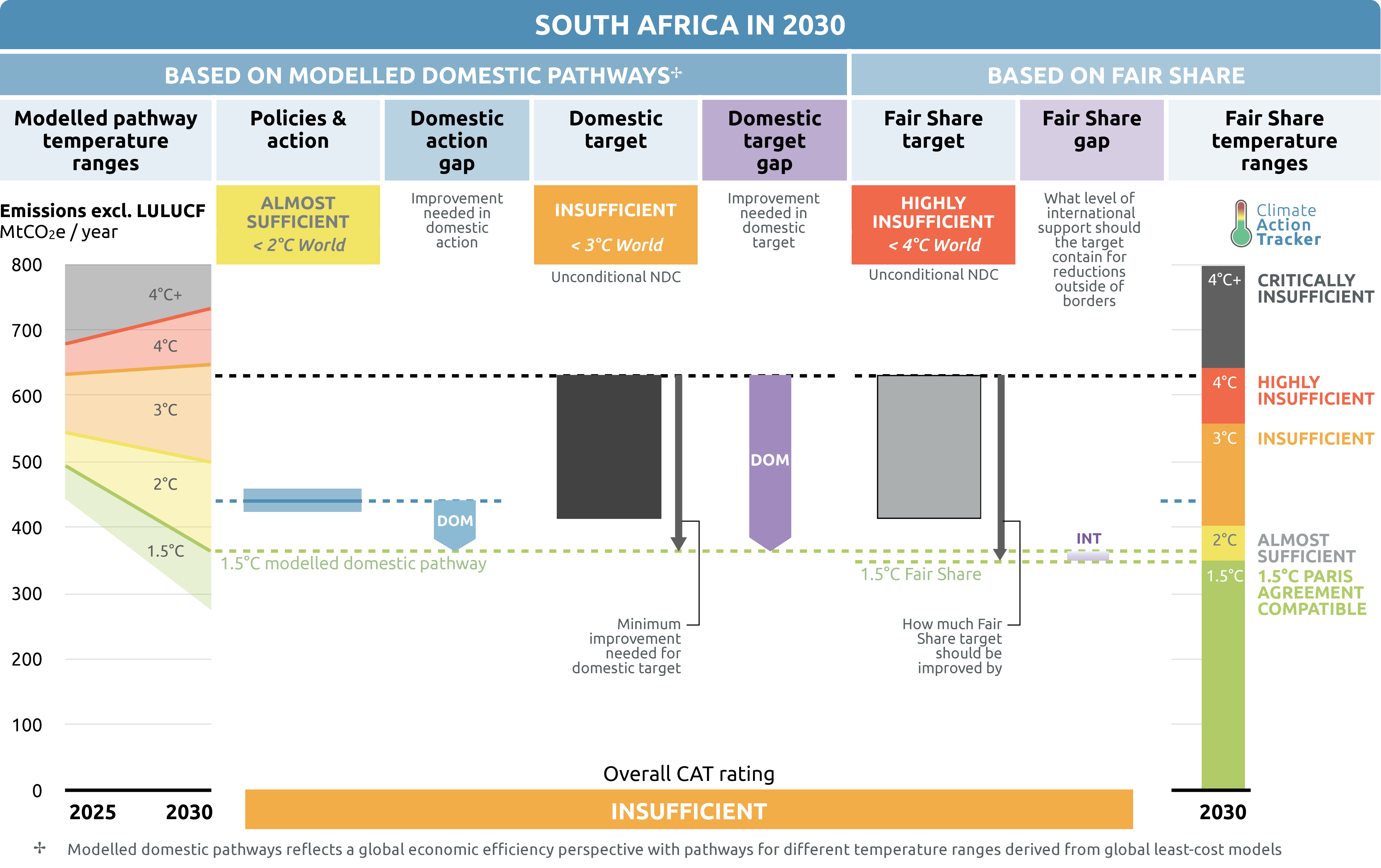

We rate South Africa’s policies and actions as “Almost sufficient”. The “Almost sufficient” rating indicates that South Africa’s climate policies and action in 2030 are not yet consistent with the Paris Agreement’s 1.5°C temperature limit but could be, with moderate improvements. If all countries were to follow South Africa’s approach, warming could be held at—but not well below—2°C. Both the fair share rating framework and the modelled domestic pathways framework suggest that stronger reductions are necessary in South Africa for a 1.5°C Paris Agreement pathway.

Our updated projections under currently implemented policies estimate that South Africa’s emissions trajectory for 2030 would decrease by around 5-6% below 2010 levels but would end up at around 36% to 38% above 1990 levels (excluding LULUCF).

These emissions projections for 2030 are well above the upper bound of the updated target range for 2030 set in the updated NDC of 2021. The modest decrease in emissions towards 2030 could be further strengthened and sustained if the government were to implement more stringent climate policies.

Almost two years into the COVID-19 pandemic, it also remains challenging to project the eventual impact of the ongoing pandemic on future emissions. South Africa has largely not prioritised a ‘green’ economic recovery and included several carbon-intensive investments in its COVID-19 recovery plans. This particularly presents a missed opportunity considering the urgent need to invest in the low-carbon transitions outlined in existing sectoral policies.

South Africa continues to experience recurring instances of rolling blackouts implemented by Eskom, South Africa’s only state-owned electricity utility. Constant operational problems at its power plants add to overall concerns on future reliability and sustainability of South Africa’s electricity supply and the successful implementation of the Integrated Resource Plan (IRP2019).

The IRP2019 aims to decommission over 35 GW (of 42 GW currently operating) of coal-fired power capacity by 2050. To be in line with the Paris Agreement goals, South Africa would need to adopt more ambitious climate action beyond the IRP2019, such as further increasing renewable energy capacity by 2030 and beyond, stopping the planned commissioning of 1.5 GW of new coal capacity, fully phasing out coal-fired power generation by 2040 at the latest, and avoiding investing in natural gas.

Uncertainty around Eskom’s financial solvency also contributes to ongoing delays in expanding renewable energy capacity. Despite some progress on renegotiating electricity prices for already grid-connected renewables projects and completing a long-awaited bid round for renewable energy projects, the Government of South Africa, together with Eskom, has not yet found a viable solution for a sustainable turnaround strategy for Eskom’s structural financial and operational problems.

The South African government implemented a carbon tax in 2019, although recent analysis indicates that the immediate impact is likely to be very limited given there are tax exemptions for up to 95% of emissions during the first phase until 2022.

Policy overview

The CAT estimates South Africa’s emissions, accounting for the potential impact of the COVID-19 pandemic, to be 484-488 MtCO2e excluding LULUCF by 2030, equivalent to a 3–23% increase above 1990 levels excluding LULUCF. Under these current policy projections, South Africa’s emission levels in 2030 will be well above the upper bound of the updated target range for the same year (around 48-52 MtCO2e higher).

Our latest projections of October 2021 are around 31-61 MtCO2e in 2030 higher compared to our projections considering the impact of COVID-19 in the first year of the pandemic. The change is both due to a higher-than-expected economic rebound in 2021 and 2022 and methodological changes (see ‘Assumptions’ section).

The COVID-19 pandemic’s impact on emissions in South Africa remains subject to uncertainty. South Africa has faced the world’s 17th highest cumulative COVID-19 caseload as of October 2021 (WHO, 2021). The COVID-19 pandemic has exacerbated South Africa’s health, social and economic challenges.

The CAT estimates a drop in emissions in 2020 of 6% below 2019 levels due to a drastic slowdown of domestic economic activity and international trade (compared to initial estimates of 9% to 11% in the 2020). For example, mining activity decreased by 21.5% in the first quarter of 2020 (SA News, 2020).

After an economic downturn of 7% of GDP in 2020, the South African Reserve Bank foresees a recovery of 4.6% of GDP in 2021 (SARB, 2021). This forecast is in line with estimates by other institutions such as the African Development Bank, the International Monetary Fund, and the World Bank (AfDB, 2021; IMF, 2021; World Bank, 2021).

The government introduced several support programmes and emergency funds in direct response to the immediate COVID-19 health and economic crisis (IMF, 2020). The South African government released its ‘Economic Reconstruction and Recovery Plan’ in October 2020 (Government of South Africa, 2021a), including a range of low-carbon and high-carbon recovery measures for implementation within a 12-month timeframe. High-carbon measures include the procurement of emergency electricity capacity in a technology-neutral auction, several measures to promote mining operations without specific conditions for low-carbon operations, and promotion of its liquefied petroleum gas (LPG) infrastructure. Low-carbon measures include further support for energy efficiency retrofits and promotion of low-carbon urban public transport.

South Africa’s response to the COVID-19 pandemic overall stands in contrast to domestic and international calls for a ‘green’ and low-carbon economic recovery (Climate Action Tracker, 2020; IEA/IMF, 2020). As of October 2021, the South African government has spent only around 4% of all recovery spending totalling to USD 2.5bn on deliberately low-carbon measures (Energy Policy Tracker, 2021; Global Recovery Observatory, 2021).

These findings show the South African government has missed the opportunity to make use of a ‘green’ recovery to directly support the National Development Plan (NDP) providing a 2030 vision on sustainable development, eliminating poverty and reducing inequalities (National Planning Commission, 2012). There are various sectoral plans, of which the Integrated Resource Plan (IRP) for electricity is South Africa’s main policy affecting GHG emissions (see ‘Energy supply’ section below).

Recent analyses by South African research institutions confirms once more that investments in renewable energy coupled with storage and peak technologies presents the cost-optimal and reliable energy supply choice (Roff et al., 2020; Wright & Calitz, 2020). These investments in low-carbon technologies would enable substantial opportunities for ‘green’ stimulus, value chain localisation, job creation, and local air pollutant reduction, especially to support vulnerable coal mining regions in their just transition efforts.

South Africa adopted a carbon tax in February 2019 covering fossil fuel combustion emissions, industrial processes and product use emissions, and fugitive emissions such as those from coal mining (Climate Home News, 2019; Reuters, 2019). The tax was implemented in June 2019 (KPMG, 2019).

Recent analysis indicates that the carbon tax currently does not effectively contribute to emission reductions given the low levy in comparison with other carbon prices, generous basic allowance and other available exemptions such as the use of offset credits (Szabo, 2021).

A basic tax-free threshold for around 60% of emissions and additional allowances for specific sectors would result in tax exemptions for up to 95% of emissions during the first phase until 2022. While the full carbon tax rate is proposed to be R120/tCO2e (US$ 8/tCO2e), after exemptions, the effective tax rate is expected to be between R6–48/tCO2e (US$ 0.4–3/tCO2e) (KPMG, 2019). The Carbon Tax implementation will be accompanied by a package of tax incentives and revenue recycling measures to minimise the impact of the first phase of the policy (up to 2022) on the price of electricity and energy intensive sectors including mining, iron and steel (EY, 2017, 2018).

South Africa released a draft Climate Change Bill in June 2018, which was open for public consultation until the beginning of August 2018 (Climate Change Bill, 2018: For Public Comment, 2018). This process has been delayed and the cabinet just submitted the bill to Parliament in October 2021 (Government of South Africa, 2021d).

The draft law aims to establish a Ministerial Committee on Climate Change to oversee and coordinate the activities across all sector departments. Under the proposed legislation, the Minister responsible for Environmental Affairs together with the Ministerial Committee on Climate Change would have to set sectoral emission targets (SETs) for each GHG emitting sector in line with the national emission target every five years and carbon budgets would be allocated to significant GHG emitting companies. Carbon budgets would put a cap on emissions and make it mandatory for companies to constrain their emissions.

Energy supply

One of South Africa’s key policies to reduce emissions is through increased deployment of renewable energy. At the end of 2019, installed renewable capacity totalled 9.6 GW (IRENA, 2021).

Originally introduced in 2010, the Integrated Resource Plan (IRP) 2010–2030 is the government’s capacity expansion plan for the electricity sector until 2030 (Department of Energy, 2011), which contains targets for all technologies, including renewable energy technologies.

The IRP sets an overall emissions constraint of 275 MtCO2/year for electricity generation after 2024, meaning that the total emissions from electricity generation should not be higher than this threshold; this has been an important instrument supporting the inclusion of renewable energy capacity targets.

In October 2019, the Cabinet passed the IRP2019 update (Department of Energy, 2019). The approval of the IRP in 2019 is a very positive signal to actively shape the future of South Africa’s power sector, after struggling for years to update the original document from 2010.

The revised plan aims to decommission over 35 GW (of 42 GW currently operating) of Eskom’s coal generation capacity by 2050. Interim steps are 5.4 GW by 2022 and 10.5 GW by 2030. The 5.7 GW of coal capacity currently under construction would be completed and another 1.5 GW of new coal capacity would be commissioned by 2030. Recent analysis suggests that these planned coal power plants will be significantly more expensive than their low-carbon alternatives (Ireland & Burton, 2018; Paton, 2018).

Coal capacity additions are not in line with a decarbonisation of the global power sector to meet the Paris Agreement targets. Recent analysis by the Climate Action Tracker shows that the share of unabated coal-fired power in the South African electricity sector should reach a maximum of about 35% in 2030 with coal power completely phased out by 2040 to be compatible with the Paris Agreement. The significant volume of coal capacity to be decommissioned marks a significant shift away from previous planning.

The Government’s IRP2019 capacity planning until 2030 includes no new nuclear capacity procurement but suggests extending the operational lifetime of the Koeberg nuclear power plant by 20 years, which was earlier expected to retire in 2024. Policy Position 8 of the IRP2019, however, emphasises the need for a nuclear build programme to the extent of 2.5 GW, which is not reflected in the actual capacity planning until 2030. The Government launched a Request for Information (RFI) to commence preparations for a new nuclear build programme in June 2020 (Eberhard, 2020). Uncertainty remains on the Government’s intentions to support nuclear capacity in the future.

At the same time, the IRP2019 increases the target for installed renewable capacity five-fold by 2030 compared to today, to 31.2 GW (an additional 15.8 GW for wind and 7.4 GW for solar by 2030). This figure is about a third of total electricity generation in 2030 (Department of Energy, 2019).

In 2012, the government replaced its feed-in-tariff scheme with the Renewable Energy Independent Power Producer Procurement Programme (REIPPPP). By October 2021, the REIPPP procured a total of 6.4 GW of renewable projects through the Bid Window 1 to Bid Window 4 (Independent Power Producers Office, 2019; Pinto, 2021).

Despite the success of the REIPPPP in generating interest in renewable energy project development—with all bidding rounds significantly over-subscribed—there have been considerable delays in connecting the procured renewable projects to the grid over time. The Department of Mineral Resources and Energy in 2020 announced a refinancing initiative for grid-connected renewables projects by independent power producers to lower the wholesale electricity price (Arnoldi, 2020). Eskom’s ongoing financial solvency issues still expose the future of the REIPPP and PPAs to high uncertainty.

The latest bid round for renewable energy projects of Bid Window 5 with a combined capacity of 2.6 GW, closed in August 2021 (Department of Mineral Resources and Energy, 2021b), originally intended for November 2018. At the same time, the Independent Power Producers Office sought technology-neutral procurement of 2 GW of emergency capacity under their Risk Mitigation Power Purchase Programme (RMPPP) to fill an immediate supply gap outlined in the IRP2019 (Creamer, 2020a). The final preferred bidders present a mix of fossil-based and renewable technology projects (Department of Mineral Resources and Energy, 2021a, 2021c). With financial closure outstanding until at least January 2022, grid connection may be delayed by almost six years after inception of the emergency programme and provide comparatively expensive electricity (Eberhard, 2021a).

Apart from additional procurements, the Department of Mineral Resources and Energy implemented a long-awaited increase of the licensing threshold for embedded generation projects from 1 MW to 100 MW in June 2021 (Government of South Africa, 2021b). This regulatory change is expected to increase distributed generation capacity, especially solar PV.

For South Africa, the share of renewables in total electricity generation would need to reach a minimum of 45% by 2030, 85% by 2040, and 98% by 2050 to be compatible with the Paris Agreement according to recent analysis by the Climate Action Tracker.

Eskom’s substantial financial, structural, and operational challenges led President Ramaphosa to appoint an Eskom Sustainability Task Team in December 2018 (Reporter, 2018). The task team is responsible for reviewing Eskom’s turnaround strategy, assessing the appropriateness of the current Eskom business model and structure, and providing recommendations on resolving the debt burden and how to reposition Eskom going forward. In July 2020, Eskom warned of continuous load-shedding for the coming 18 months until emergency capacity is procured (Creamer, 2020b). Eskom has also publicly communicated a current electricity generation capacity deficit of 4 GW (Eberhard, 2021b).

Eskom has continuously received government bailouts over the last several years, receiving around USD 3.8bn for FY 2020/2021 (National Treasury of South Africa, 2021). The current level of debt amounts to more than USD 27bn (Eberhard, 2021b), putting the sustainability of Eskom to ensure stable energy supply and successfully manage the transition to a low-carbon electricity system at high risk.

A post-2015 National Energy Efficiency Strategy (NEES) is under consideration to replace the first NEES adopted in 2005 (Department of Energy, 2016). This strategy aims to build on the achievements of the first NEES, which saw higher than targeted improvements in energy intensity, by stimulating further energy efficiency improvements through a combination of financial incentives, legal and regulatory frameworks and enabling measures. It is expected to reduce economy-wide final energy consumption by 29% below 2015 levels by 2030.

Industry

Policy and planning documents for the South African industry sector generally address sustainable industrial economic development but barely mention mitigation targets for the industry sector or concrete measures for implementation. The post-2015 draft National Energy Efficiency Strategy (NEES) proposes industrial sector targets that would reduce the weighted mean specific energy consumption in manufacturing by a meagre 16% by 2030 and to realise a total of 40 PJ in cumulative annual energy savings by 2030, arising from specific energy saving interventions undertaken by mining companies (Department of Energy, 2016). Energy use from the mining and quarrying sector amounted to 185 PJ in 2015 (IEA, 2017).

The South African government intends to achieve these targets through implementing several proposed measures such as the National Cleaner Production Centre South Africa (NCPC-SA) that promotes energy efficiency measures, its associated Industrial Energy Efficiency Project (IEE) that promotes energy management systems, or the Green Fund South Africa that financially supports green technology research and implementation. However, these measures may only induce small emissions reduction impacts.

There are no signs of policy-driven emissions reductions in the near future for emissions-intensive subsectors such as steel production and mining. Recent analysis by the Climate Action Tracker indicates that the steel industry’s emissions intensity would need to be reduced by about 30% in 2030 and by about 90%-100% by 2050 to be compatible with the Paris Agreement.

Transport

The Department of Transport published the country’s first Green Transport Strategy (GTS) 2018–2050 in 2018 (Department of Transport South Africa, 2018), proposing a list of measures that should be implemented to transition the sector to a low carbon future. Recent analysis by the Climate Action Tracker indicates that the share of zero emissions fuels (biofuels, electricity and hydrogen) of the total domestic transport sector demand would need to increase to 20% by 2030, 50-60% by 2040, and 80%-90% by 2050 to be compatible with the Paris Agreement.

The Biofuels Industrial Strategy, which falls under the Petroleum Products Act, mandates biofuel blending of 2%–10% for bio-ethanol and a minimum of 5% for biodiesel from 2015 onwards. The Government only passed Biofuels Regulatory Framework (BRF) to implement the Biofuels Industrial Strategy in February 2020 (WWF, 2020). Uncertainty remains on the socio-economic benefits to be achieved through the BRF and the uptake of first and second generation biofuels over time. Due to the ongoing uncertainty of implementation, the mandatory blending of biofuels has not been included in our current policy projections. If the minimum policy targets of 2% blending for first generation biofuels were to be met, they would lower emissions by up to 0.7 MtCO2e/a from 2025 onward.

South Africa introduced other road transport-related policies such as vehicle fuel economy norms for newly manufactured passenger and commercial vehicles (in 2005), vehicle labelling scheme (in 2008), and a carbon emissions motor vehicles tax as an environmental levy on passenger vehicles with emission levels above certain thresholds (in 2010). Under the GTS 2018–2050, the Department of Transport currently states its intention to revise the level of vehicle fuel economy standards (Department of Transport, 2017b).

South Africa’s Electric Vehicle Industry Roadmap (2013) aims to introduce electric passenger vehicles. However, as of August 2020, no local manufacturing or purchasing incentives for local manufactures have been introduced under the roadmap. The total number of such vehicles sold in South Africa remains marginal, with only around 550 vehicles sold in South Africa in 2019 (Kuhudzai, 2020). Most recently, in May 2021 the Government of South Africa released the ‘Auto Green Paper’ for public consultation (Department of Trade Industry & Competition, 2021). The strategy aims to define South Africa’s framework for a comprehensive and long-term automotive industry transformation plan on low-carbon vehicles. No final policy proposal had been approved by Cabinet, as of October 2021.

Recent analysis by the Climate Action Tracker shows that the electric vehicle share in annual vehicle sales in South Africa would need to increase to 50-95% by 2030 and 90-100% by 2040 to be compatible with the Paris Agreement.

Recently introduced Bus Rapid Transit Systems (BRT) have initiated the main switch in modal share of passenger transport in urban areas. These have commenced operation or are currently under consideration in public transportation planning in several South African urban areas (Department of Transport, 2017a). Initiatives to implement and expand BRT systems are currently taking place in eight cities and municipalities.

Buildings

South Africa has implemented several building regulations and codes on energy efficiency and usage in buildings for new buildings and major refurbishments of old buildings (Sustainable Energy Africa, 2017). The government has introduced some energy efficiency and labelling requirements for household applications and a five-year retrofit project to retrofit 1,450 buildings with energy efficient installations (Grantham Research Institute on Climate Change and the Environment, 2017). The draft Post-2015 National Energy Efficiency Strategy foresees reductions of the final energy consumption by 33% in the residential sector and 37% in the public and commercial sector by 2030, compared to the 2015 baseline (Department of Energy, 2016).

South Africa has made significant improvements by increasing the buildings energy efficiency per square metre, while the buildings emissions intensity per capita is only slowly decreasing. The move away from biomass use for cooking and heating towards the use of more modern appliances that require electricity, which, in turn, is largely generated by fossil fuels, might significantly increase indirect emissions.

Recent analysis by the Climate Action Tracker suggests that the buildings emissions intensity would need to decline by 50% for residential buildings by 2030 in comparison to 2015 values, 90% by 2040, and 100% by 2050 to be compatible with the Paris Agreement.

Although retrofitting rates in the residential and commercial buildings sector are still comparatively low, green retrofitting of existing buildings is expected to be the largest sector of the green building industry in South Africa within the next three years (World Green Building Council, 2016a). It is expected that the proportion of green buildings in South African building activity will increase over the next years due to cheaper operations costs and higher returns on investments compared to conventional buildings (GBCSA, 2017; World Green Building Council, 2016b). The trend towards more energy efficient buildings has been accelerating. A pending regulation on stricter building and appliances standards and certifications could potentially further stimulate this trend (Sustainable Energy Africa, 2017).

The government released a regulation for mandatory energy performance certificates in 2020 (Department of Mineral Resources and Energy, 2020). The regulation applies to four different classes of larger-scale buildings with a requirement that all buildings must to be compliant until the end of 2022 (Smith, 2021).

Agriculture

There is a limited number of policies in South Africa’s agricultural and forestry sector targeted at climate change mitigation. The Second Biennial Update Report specifies two Long Term Mitigation Strategy (LTMS) measures on enteric fermentation and reduced tillage (Department of Environmental Affairs, 2017; Winkler, 2007). However, there is no information on their state of implementation.

The National Climate Change Response Policy further names climate smart agriculture (CSA) as a practice “that lowers agricultural emissions, is more resilient to climate changes, and boosts agricultural production” (Government of South Africa, 2011). A number of CSA activities are already in place in South Africa (Nciizah & Wakindiki, 2015), but their expected or actual mitigation impacts are not reported.

Agriculture emissions intensity in South Africa (GHG emissions per value added) has been declining significantly over the last decade and reached 1.73 tCO2e/thousand USD in 2014 compared to 3.13 tCO2e/thousand USD in 1995 (Climate Action Tracker, 2018). However, emissions intensity is still significantly above the world average of 1.25 tCO2e/thousand USD in 2014. Total GHG emissions from livestock declined by 5.6% between 2000–2012, attributed to the decline in cattle populations. However, the total livestock population over this period increased by 29.8% due to large growth in the poultry industry with low enteric fermentation emissions (Department of Environmental Affairs, 2016). Domestic meat production of 159 g/cap/day in 2013 remains comparatively high compared to the world average of 117 g/cap/day in 2013.

Forestry

There are only a limited number of mitigation related policy measures in South Africa’s forestry sector. The 2nd Biennial Update Report lists work programmes on fire prevention, water, and wetlands, as well as a Long Term Mitigation Strategy (LTMS) measure on afforestation to plant an additional 760,000 ha of commercial forests by 2030 (Department of Environmental Affairs, 2017; Winkler, 2007). No information on their state of implementation is provided.

According to national data, the forestry sector has been a net sink over the period from 2000 to 2012, no official national data is available for later years (Department of Environmental Affairs, 2016), nor are projections.[1] In the inventory, crops and grasslands are sources of emissions, however, those are overcompensated by a sink from forest lands. Opposed to national data, FAO Statistics show a small emissions source for the land use sector in total, stable over the last two decades at around 2 MtCO2e (FAOSTAT, 2017).

Given the importance of the timber industry, the area of woody crops has almost doubled since the early 1990s, and stabilised over the last decade (FAOSTAT, 2017). However, at the same time, the overall forest area has continuously decreased (Department of Environmental Affairs of South Africa, 2014; FAOSTAT, 2017). The planted trees are non-domestic species, and concerns about their negative impacts on water resources have been raised (Bosch & von Gadow, 1990).

The reason forests are a net sink despite decreasing forested area may be that the carbon content of the planted forests compared to the deforested area is higher. However, with different and contradicting data sources available, it is unclear whether this is the reason for this apparent mismatch, or whether there are methodological issues in the inventory.

[1] South Africa’s Greenhouse Gas Mitigation Potential Analysis excludes the sector and states “there is not sufficient evidence to be able to predict a change in either case so no sequestration is provided for (positive or negative)” (Department of Environmental Affairs, 2014).

Further analysis

Latest publications

{kind=link}

Stay informed

Subscribe to our newsletter