United Kingdom

Policies & action

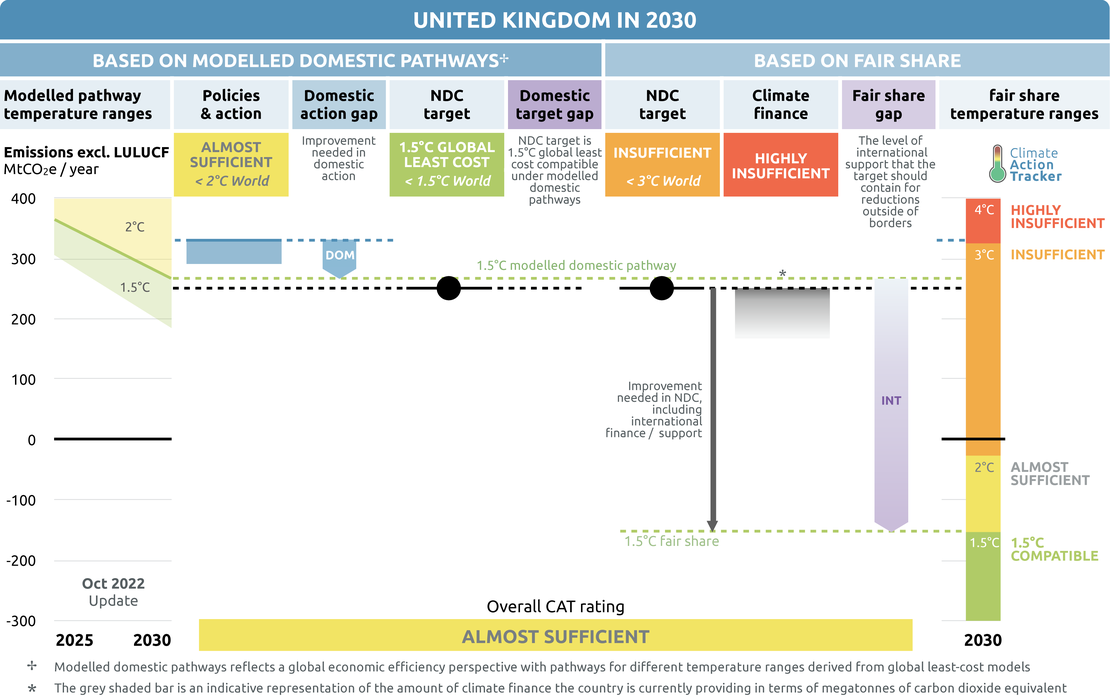

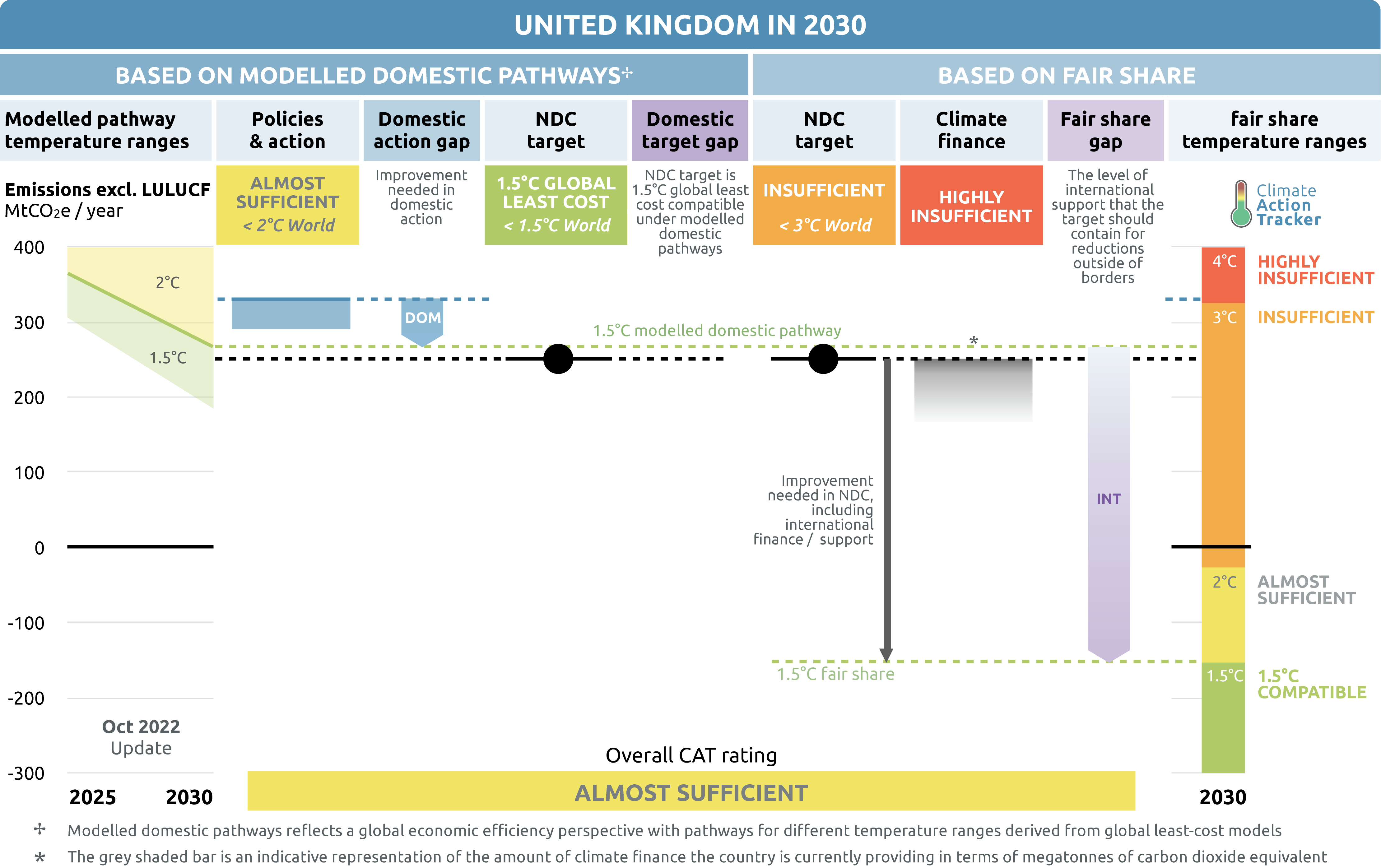

We rate the UK’s current policies until 2030 as ”Almost sufficient”, when compared to modelled domestic pathways. Current policies are expected to reduce emissions to 293–331 MtCO2e/yr in 2030, or 58–63% below 1990 levels (excl. LULUCF). In some areas there are clear policies with credible delivery mechanisms and funding. However, critical gaps remain, particularly around energy efficiency and demand reduction.

The UK is not on track to achieve its current climate targets. The “Almost sufficient” rating indicates that the UK’s climate policies and action are not yet consistent with limiting warming to 1.5°C but with moderate improvements could align with a 1.5°C modelled domestic pathway. If all countries were to follow the UK’s approach, following a consistent globally cost-effective pathway, warming could be held below—but not well below—2°C.

Further information on how the CAT rates countries (against modelled domestic pathways and fair share) can be found here.

Policy overview

Since passing the net zero target in June 2019, the UK has brought forward a wide range of policies and plans to help achieve this goal. This includes sectoral decarbonisation plans for transport, buildings, industry and hydrogen, as well as commitments on tree planting, peatland restoration and others.

In October 2021, the Net Zero Strategy was released, which provides the fullest picture to date on how the government intends to achieve its climate targets. This incorporates all the previous sectoral plans and makes some additional commitments. Since then, the UK has also released an energy security strategy, in response to the energy price crisis and Russian invasion of Ukraine, as well as the Jet Zero strategy, which outlines the Government’s approach to reducing aviation emissions (UK Government 2022c, Department for Transport 2022b).

The Net Zero strategy failed to quantify the impact of the individual plans and policies contained within it. This makes it very challenging to ascertain whether the strategy provides sufficient measures to achieve the UK’s climate targets. This lack of quantification was found to breach the UK’s legally binding Climate Change Act (Justice Holgate 2022, Royal Courts of Justice 2022). The UK High Court ordered the Government to provide an updated strategy by March 2023, which clearly communicates the estimated impact of the UK’s climate policy.

If the world is to move from the era of target setting to the era of delivery, transparency will be essential to enable accountability and policy scrutiny. It is therefore vital that the UK provides greater detail on the expected impact of its policies in future.

The UK’s current policies have recently been reviewed by the Climate Change Committee (CCC), in its annual progress report (CCC 2022b). This review identified that, although substantial progress has been made in developing UK climate policy, significant policy gaps remain.

In particular, the Government’s current policy lacks ambition on energy efficiency, ignores measures to reduce consumer demand for high-carbon activities such as consumption of red meat and aviation, and has no coherent strategy for agriculture or land-use.

The lack of focus on energy efficiency is particularly problematic, as efficiency measures are a key strategy to reduce consumer bills in the current price crisis and reduce the need for additional energy supply. The UK also has the least energy-efficient housing stock in Western Europe (Tado 2020).

However, the UK’s response to the energy crisis has been almost entirely focused on the supply side, with commitments to expand nuclear power generation and increased support for domestic fossil fuel extraction (UK Government 2022c). Support for fossil fuels includes a windfall tax which contains 90% tax relief for companies which investing in new domestic oil and gas extraction. This risks accelerating both fossil fuel profits and global warming. The UK has also lifted the ban on fracking for shale gas (Stallard 2022). New fossil fuel supply is incompatible with the Paris Agreement and, as gas is traded on international markets, will not noticeably reduce energy prices in the UK. The UK should instead be focusing on rapidly accelerating deployment of wind and solar, which are now paying money back to consumers (Luke 2022), and reducing gas reliance via energy efficiency and buildings electrification.

With limited ambition on energy efficiency and demand reduction, the Government’s approach also relies strongly on technological progress instead, including large-scale CO2 removal to achieve net zero GHGs by 2050. Many of these technologies are not currently available at scale, and so large-scale reliance on them therefore represents a substantial delivery risk to the UK’s climate targets.

The CCC highlights that there are significant risks to delivery in the UK’s current climate policy, with only 39% of the gap between the current projections and the UK’s climate targets covered by credible policy. The CCC suggests that a further 24% could be closed by policies which are broadly credible but contain some risks. Using this data, and converting to the CAT emissions standard (AR4 GWPs excl. LULUCF), we calculate that under current policies, the UK’s emissions in 2030 would be between 293–331 MtCO2e/yr. This is 58–63% below 1990 levels, leaving an emissions gap of 42–80 MtCO2e that needs to be addressed by additional climate policy.

Sectoral pledges

During COP26 in Glasgow in 2021, a number of sectoral initiatives were launched to accelerate climate action. At most, these initiatives may close the 2030 emissions gap by around 9%—or 2.2 GtCO2e, though assessing what is new and what is already covered by existing NDC targets is challenging.

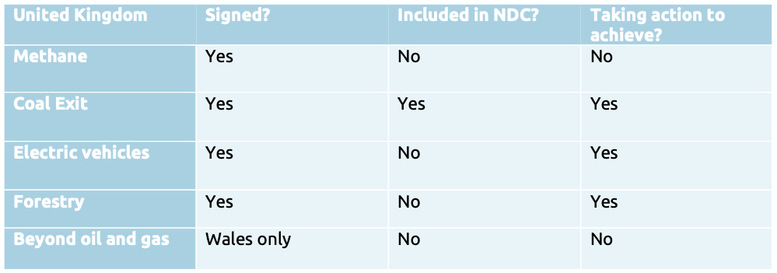

For methane, signatories agreed to cut emissions in all sectors by 30% globally over the next decade. The coal exit initiative seeks to transition away from unabated coal power by the 2030s or 2040s and to cease building new coal plants. Signatories of the 100% EVs declaration agreed that 100% of new car and van sales in 2040 should be electric vehicles, 2035 for leading markets. On forests, leaders agreed “to halt and reverse forest loss and land degradation by 2030”. The Beyond Oil & Gas Alliance (BOGA) seeks to facilitate a managed phase out of oil and gas production.

NDCs should be updated to include these sectoral initiatives, if they’re not already covered by existing NDC targets. As with all targets, implementation of the necessary policies and measures is critical to ensuring that these sectoral objectives are actually achieved.

- Methane pledge: The UK signed the methane pledge at COP26. Methane represented 13% of the UK’s GHG emissions in 2020 and is concentrated in the agricultural and waste sectors. While policies exist to reduce methane emissions from the waste sector, there is no current policy framework to reduce agricultural emissions (UK Government 2022h).

- Coal exit: The UK signed up to the coal exit pledge at COP26 and aims to phase out coal in the power sector by 2024. In 2021, coal provided only 2% of UK electricity generation, compared to 40% a decade ago (BEIS 2022c).

- 100% EVs: In the run-up to COP26, the UK confirmed that it aims to phase out the sale of petrol and diesel cars and vans by 2030, and all hybrids by 2035. The UK has a broad range of policies to incentivise EV uptake, and sales are accelerating rapidly (see ‘Transport’ section below) (Department for Transport 2021b).

- Forestry: The UK signed the forestry pledge at COP26. The UK has one of the lowest levels of forest cover in Europe, at 13% in 2021 (Woodland Trust 2021). The UK aims to more than double tree-planting rates by 2035, to 50,000 hectares/y (UK Government 2021e). This would lead to forest cover of 18% in the UK by 2050 (CCC 2020).

- Beyond oil and gas: The UK Government is not a signatory of the Beyond Oil and Gas Alliance. The Welsh Government is a signatory, although current oil and gas extraction in Wales is minimal. In contrast, the UK Government is currently approving new oil fields in the North Sea and envisages non-negligible oil and gas production remaining until to 2050 and beyond (BEIS 2022a, Thomas 2022b, Tidman 2022).

Energy supply

The UK electricity sector has been rapidly decarbonising in recent years, as consistent and coherent policy has supported renewables deployment and driven coal out of the electricity mix. Power sector emissions fell by 63% between 2011–2021 (BEIS 2022d). Coal provided only 2% of electricity generation in 2021, down from 40% a decade ago (BEIS 2022c). Meanwhile generation from zero carbon sources (renewables and nuclear) reached 55% in 2021, with 40% of this coming from renewables.

The UK’s contract for difference (CfD) scheme has provided price stability for renewable generators and encouraged large-scale investment into renewables deployment, particularly offshore wind. This has led to rapid deployment and falling costs. The CfD scheme will continue to be a central plank of the Government’s strategy in the power sector, but needs to be complemented with policies to support flexible low-carbon generation and storage, as well as a detailed plan on how unabated fossil gas will be phased out by 2035. Overall, 72% of the emissions reductions required to achieve the Government’s targets in the power sector are covered by credible policies (CCC 2022b).

Current UK policy on fuel supply is lacking ambition, and more could be done to reduce emissions involved in oil and gas extraction. The Government is also continuing to approve new oil and gas fields, which are incompatible with 1.5°C, risk becoming stranded assets, and will not address the current energy price crisis. Between 2022 and 2025, up to 46 new oil and gas projects could be approved, producing up to 900 MtCO2e (Greene 2022). This is more than two years of the UK’s annual emissions. Only 26% of the emissions reductions required in the fuel supply sector are currently covered by credible policies (CCC 2022b).

Electricity

In mid-2021, the UK confirmed it will bring forward the date for the phase-out of coal-fired power by one year to 2024. A 2024 phase-out makes the UK a world leader in this regard, and is well ahead of the 2030 phase-out date for OECD countries required to limit global warming to below 1.5°C (IEA 2021).

In the Net Zero Strategy, the UK committed to achieving 100% clean electricity by 2035, subject to security of supply (UK Government 2021e). While this is to be welcomed, detailed policy to phase out unabated gas generation by 2035 is still lacking (CCC 2022b). There is still over 16 GW of gas-fired power capacity in the pipeline in the UK (Global Energy Monitor 2022). This will either need to be cancelled, converted to run on hydrogen, or operate only as emergency reserves, to be consistent with the UK’s ambition for a decarbonised power sector by 2035.

The UK has a range of policies to support renewables deployment. The central policy is the Contract for Difference (CfD) scheme, which offers a guaranteed price to renewable generators over their lifetime, with the price set by reverse auctions. This has encouraged competition and innovation in the sector and driven large-scale investment and deployment. Wind capacity tripled in the past decade to 27 GW in 2021, while solar capacity grew from 2 GW in 2012 to 14 GW (IRENA 2022). The latest auction secured 11 GW of renewables, including 7 GW of offshore wind at a price of GBP 37/MWh (UK Government 2022b) – a third of the price just five years before.

The Government recently increased the frequency of CfD auctions to occur annually (UK Government 2022j), and will now allow onshore wind and solar to compete for funding again (BEIS 2020). This is a positive step, as deployment fell rapidly after these technologies were excluded from the scheme in 2015 (Unwin 2019). However, the planning system in England for onshore wind is still very restrictive, and will likely prevent substantial deployment unless revised (RenewableUK 2022).

The UK electricity system has seen a large increase in biomass consumption over the past decade. Bio-electricity provided 13% of generation in 2021, up from 3% a decade earlier (BEIS 2022c). This has been partly due to the Drax power plant, which has switched from burning coal to burning biomass. Widespread concerns have been raised about both the carbon neutrality and wider sustainability of biomass as an energy source (Energy Transitions Commission 2021). After ongoing public criticism of the sector, Drax, the UK’s largest biomass plant, updated its sourcing policy in 2019 to ensure the biomass it uses meets Forestry Commission sustainability recommendations (Drax 2020, Matthews et al 2015). However, the UK still provides over GBP 1bn a year in subsidies to UK biomass energy producers via a fee on energy bills, and there is growing pressure to redirect this money to other forms of renewable energy (Ember 2020).

The Government envisages that nuclear will play a key role in decarbonising the electricity system. In the Energy White Paper, the Government committed to bringing at least one large-scale nuclear plant to final investment decision by the 2024 (UK Government 2020a). The UK is also investing in the development of advanced nuclear technology, with a public investment of up to GBP 385m in an Advanced Nuclear Fund (UK Government 2021e). This government’s nuclear ambitions were supercharged in the Energy Security Strategy, which set an ambition to source up to 25% of electricity from nuclear in 2050 (BEIS 2022b). Historically, construction of nuclear power stations in the UK have been over budget and behind schedule (Chuter 2022). The cost of these power plants will also be placed on energy bills via the regulated asset base model (Department for Business Energy and Industrial Strategy 2022). If the government’s nuclear aspirations are to be realised successfully without excessively burdening consumers, new nuclear plants will need to be built within budget and to schedule.

Fuel supply and hydrogen

Achieving the UK’s climate targets will require strong and sustained reductions in oil and gas production, as well as improvements to the emissions intensity of any remaining extraction. Oil and gas demand will need to fall around 30% by 2030 to achieve the UK’s NDC (CCC 2020). The CCC also suggested that the emissions associated with oil and gas extraction should fall 68% by 2030, through electrification of processes and reducing fugitive emissions (CCC 2020).

The UK’s North Sea Transition plan aims to reduce emissions associated with fuel extraction by 50% in 2030 (BEIS 2021). This is lower than the CCC benchmark, and is also voluntary (Merrick 2022). The Government is also continuing to support new oil and gas extraction in the North Sea, recently approving the Abigail and Jackdaw fields (Tidman 2022, Thomas 2022b), and is actively aiming to further expand domestic oil and gas consumption (Thomas 2022a).

A new licencing round will be held in autumn 2022, where projects will have to pass a ‘climate compatibility checkpoint’ to be approved (BEIS 2022b). Up to 46 projects could be approved by 2025, generating 900 MtCO2 of cumulative emissions (Greene 2022). This is in stark contradiction to the IEA’s conclusion that to achieve net zero emissions by 2050, no new fossil fuel projects should be approved from now on (IEA 2021).

The UK aims to use low-carbon hydrogen to support decarbonisation in sectors where electrification is more challenging. The Government recently doubled its 2030 ambition to 10 GW of low-carbon hydrogen production, with at least half of this coming from electrolysis (BEIS 2022b). This is broadly comparable in ambition to the EU27’s REPowerEU strategy.

Transport

The transport sector is the largest source of emissions in the UK, representing 24% of territorial emissions (UK Government 2022h). The UK government has made a range of commitments and policies to help decarbonise transport. This includes ending the sale of fossil fuel cars and vans by 2030 and fossil fuelled heavy goods vehicles (HGVs) by 2035–40 (Department for Transport 2021b), support to make bus services faster and more reliable, and support for cycling infrastructure. As a result, 46% of the emissions reductions required to align with the UK’s climate targets is now covered by credible policy in the transport sector (CCC 2022b), with particularly strong policy to support electric vehicle uptake. Battery electric vehicles represented 12% of UK car sales in 2021, which is above the Government’s own projections of the deployment rates needed to achieve the UK’s climate targets (SMMT 2022, CCC 2022b).

At the same time, there are a range of areas where Government ambition is lacking. The UK 2020 budget included GBP 27.4 bn for road building (UK Department for Transport 2020), which could lead to an additional 20 MtCO2e of emissions between 2020 and 2032 (Sloman & Hopkinson, 2020). Fuel duty rates for petrol and diesel remain frozen since 2010, which is estimated to have increased UK carbon emissions by as much as 5% over the past decade (Evans 2020).

Finally, the UK’s latest strategy for reducing aviation emissions explicitly rejects curbing aviation demand as a mitigation strategy, relying instead on unprecedented roll-out of sustainable aviation fuel and CO2 removal to balance any remaining emissions (Department for Transport 2022b). This runs contrary to the CCC’s recommendations and represents a considerable delivery risk to the UK’s climate targets.

Road transport

The UK will ban sale of fossil fuelled cars and vans by 2030. This makes the UK a global front-runner in this regard and brings it into line with the CCC’s advice (CCC 2020). Sales of hybrid vehicles will be banned from 2035, and only those with ‘significant zero-emissions capability’ will be able to be sold post-2030.

This policy is supported by a zero emissions vehicle (ZEV) mandate, which sets legally binding targets for sales of ZEVs from 2024 (Department for Transport 2021b). The UK has also set out a strategy to achieve 300,000 public charging points by 2030 (UK Government 2021f). However, accompanying policies to reduce emissions from fossil fuelled vehicles are too weak and need strengthening.

The Government has also committed to end the sale of fossil fuel heavy goods vehicles (HGVs) by 2040, with sales of smaller trucks banned by 2035 (UK Government 2021e). The Government has already allocated GBP 19m to support small-scale trials of different zero-carbon HGV options and announced an additional GBP 200m to support a three-year programme of further trials (UK Government 2022a).

Active and public transport

The UK government introduced a national bus strategy, supported by GBP 3bn of funding for 2021–2024 (Department for Transport 2021a). This strategy aims to make buses cheaper and more reliable by providing new bus lanes and better coordination between contractors and local authorities. The Department for Transport is also consulting on a faster phase-out of petrol and diesel buses, in the period of 2025–2032, motivated in part by the strong air quality benefits of electrifying buses (Department for Transport 2022a).

The government announced in June 2020 that GBP 2bn would be allocated specifically towards increasing the uptake of cycling and walking (Department for Transport 2020). The first stage of this project involved GBP 250m in immediate funding to construct pop-up bike lanes, wider pavements, safer junctions and cycle and bus-only corridors.

Aviation

The UK recently released its Jet Zero strategy which outlines the proposed approach to reduce emissions from this sector to net zero, by a combination of emissions reductions and offsetting (Department for Transport 2022b). This aims for domestic aviation to reach net zero emissions by 2040, and total aviation emissions to reach net zero by 2050.

The strategy relies heavily on as yet unavailable technological innovation and carbon dioxide removal to enable a ‘net zero’ aviation sector. In the strategy, the use of sustainable aviation fuel (SAF) reaches 10% of overall fuel use by 2030. This is five times the level included in the CCC’s balanced net zero pathway (CCC 2020) and would require an unprecedented scale-up.

SAF deployment remains very low globally and has consistently failed to meet expectations (Rutherford 2022). Relying so heavily on this option therefore represents a major delivery risk. In 2050, the UK expects that aviation will still be emitting 19 MtCO2 per year, which will need to be compensated for by CO2 removal. The strategy also ignores the non-CO2 impact of aviation, which represents up to two-thirds of the sector’s overall climate impact (Lee et al 2021).

The strategy also fails to address demand. The Government states that “the sector can achieve jet zero without the government needing to intervene directly to limit aviation growth” (Department for Transport 2022b), and envisages that passenger numbers could rise 70% from 2021 to 2050. This is in contrast to the CCC’s advice, which was that no net expansion in airport capacity should be permitted, and passenger growth should be nearer 25% maximum (CCC 2020). Numerous airports are currently planning expansions or have received approval to expand in the past two years (AEF 2022), which again could threaten the UK’s ability to achieve its climate targets.

For more information on the need to align aviation and shipping emissions with the Paris Agreement, see the sectoral pages on international aviation and international shipping.

Buildings

Buildings represented 20% of total UK GHG emissions in 2021, and there has been no significant reduction in emissions from this sector in the past decade (CCC 2022b).

The UK Government released the Heat and Buildings Strategy in October 2021, which outlines the proposed approach for buildings decarbonisation in the UK (UK Government 2021c). In this strategy, the government set a target of installing 600,000 heat pumps per year by 2028 and adopted a market-based approach to achieve this goal. Clear signals were also set about the standard that new homes will have to comply with.

However, significant policy gaps remain. Of the emissions reductions required until 2037 to achieve the Government’s climate targets, only 10% was covered by credible policy as of June 2022 (CCC 2022b), with 67% covered by policy with serious risks to delivery. Two key weaknesses in the Government’s strategy are the lack of ambition on energy efficiency measures, and the limited funding provided to drive heat pump uptake.

Uptake of low-carbon heat

Decarbonising the buildings sector will require a move away from natural gas, which provides around 75% of heating and hot water demand in the buildings sector. The Heat and Buildings Strategy includes a ban on the installation of all new gas boilers by 2035. This is much later than many European countries such as Germany and Netherlands, which have announced bans in the 2020s (Bah 2022, Shrestha 2022).

The Strategy provided GBP 450m to drive heat pump installation, through the Boiler Upgrade Scheme (UK Government 2021c). However, this is only enough to install 90,000 heat pumps over the 2021–24 period (Harrabin 2021b). This leaves a substantial gap to achieve the government’s target of 600,000 annual installations by 2028 (which itself lags the CCC’s target of 900,000 installations by 2028).

The Government has proposed a market-based mechanism to accelerate uptake, which could include an obligation on boiler manufacturers to sell an increasing proportion of heat pumps (analogous to the ZEV mandate in the transport sector). However, the details of this mechanism are unclear. The Government should urgently set out detailed plans on how its proposed market-based approach would work.

Building standards

The Future Homes Standard requires that, from 2024, new homes must include high levels of fabric efficiency and zero-carbon heating systems such as heat pumps or district heating (UK Government 2021g). Houses will have emissions 75–80% lower than homes built under current standards (including indirect emissions). An interim reduction target of 31% has been set for 2021–2024. However, there is no commitment to reach ultra-high efficiency standards, and the interim standard still allows houses to be built with gas boilers. It may therefore fail to accelerate construction of zero carbon buildings pre-2024 (CCC 2022a).

Energy efficiency

UK energy efficiency policy in buildings is inadequate and needs urgent improvement to align the UK with its climate targets. The need for greater action on energy efficiency is only heightened by the current energy price crisis, which could lead to two-thirds of UK households being in fuel poverty by 2023 (Evans 2022).

The Government aims for every home in the UK to reach EPC Band C by 2035, where “practicable, cost effective and affordable” (UK Government 2017). The Energy Performance Certificates (EPCs) measure the energy performance of a building, and range from EPC Band A (most efficient) to Band G (the least efficient). In support of this, the Government pledged GBP 9.2bn to fund energy efficiency improvements over 2019–2024. However, only around GBP 2bn of this funding has been allocated to-date.

The government has also scaled back, on multiple occasions, its support for energy efficiency upgrades, which damages confidence in the retrofitting industry. In particular, the Green Homes Grant, which was meant to cover efficiency improvements in owner occupied homes, was scrapped prematurely with only 10% of the funding delivered (Harrabin 2021a). This has not been replaced, leaving no substantial policy to drive efficiency improvements in owner occupied homes. With the least insulated homes set to pay up to GBP 1000/yr more in energy bills in the current price crisis (ECIU 2022), this policy gap needs to be addressed urgently.

Industry

The UK’s Industrial Decarbonisation Strategy (UK Government, 2021b), aims to reduce industrial emissions by two-thirds relative to 2018 levels in 2035 and 90% by 2050. The strategy has three-pronged approach: switching to low carbon fuels, efficiency gains, and carbon capture and storage. Of the abatement required out to 2037, only 4% is covered by credible plans to-date, although a further 46% is covered by policies that require relatively minor changes to address delivery risks (CCC 2022b). Key areas for improvement include greater action to drive resource efficiency in industry, and policy to incentivise industrial electrification.

Fuel switching

57% of industrial final energy is provided by fossil fuels (UK Government 2022e), and this will need to be reduced substantially on the path to net zero. Two key options are the use of hydrogen, and direct electrification.

The Industrial Decarbonisation Strategy sets a target of 50 TWh of fossil fuels to be replaced by low-carbon alternatives in 2035 (UK Government 2021d). This is roughly a third of fossil consumption in 2021 (UK Government 2022e). To support this target, the government introduced the Industrial Decarbonisation and Hydrogen Revenue Support (IDHRS) scheme.

This is similar to the CfD scheme in the power sector, providing financial support to cover the additional cost of low-carbon hydrogen production. GBP 100m has been allocated to support fuel-switching in 2023, with further funding to be allocated in 2024. This provides a business model to support industrial fuel-switching to hydrogen and is to be welcomed. However, there is no comparable model for industrial electrification, despite the significant potential (Madeddu et al 2020).

Carbon capture and storage

The UK Government aims to deliver 6 MtCO2/yr of industrial CCS by 2030, and 9 MtCO2/yr by 2035. This represents around 22% of total abatement in the industrial sector in 2035 (CCC 2020). This ambition is supported by the GBP 1bn CCUS infrastructure fund, as well as a business model for industrial CCS which will cover the additional costs for fitting carbon capture to industrial applications. Relying on CCS to deliver emissions reductions in the industrial sector could be risky, as the majority of previous CCS projects have ended in failure (Abdulla et al 2021). In many sectors, the role and value of CCS is also being eroded as the cost of renewables declines (Grant et al 2021b, Luderer et al 2021).

Resource and energy efficiency

The Government sees resource and energy efficiency as a key strategy for industrial decarbonisation, saving 11 MtCO2e in 2035 (UK Government 2021e). This represents 27% of total abatement, more than from CCS, hydrogen or electrification alone. Policies to support energy efficiency include the Industrial Energy Transformation Fund and the Climate Change Agreements (UK Government 2022d). However, more action is needed to drive industrial resource efficiency, in both the production and consumption of goods. Key to this is expanding the scope of current extended producer responsibility (EPR) schemes and improving data transparency on the production and use of industrial products (CCC 2022b).

Agriculture

Agriculture was responsible for 46 MtCO2e of emissions in 2020, representing 11% of UK emissions (CCC 2022b). The UK’s exit from the EU’s Common Agricultural Policy (CAP) represents a unique opportunity to redesign UK agricultural policy with a focus on emissions reductions and other environmental goals. While new policies such as the Environmental Land Management (ELM) schemes represent a step forward, targets and policies remain largely short-term, unambitious and incomplete. As a result, currently no policies or plans exist that can be seen as credible in reducing emissions (CCC 2022b). This needs to be urgently addressed.

A central part of the UK’s strategy to address agricultural emissions are the ELM schemes. There are three schemes, which together will replace the EU’s CAP. They represent a shift towards farming subsidies being focused on the delivery of public goods, including environmental protection and carbon sequestration (Department for Environment Food & Rural Affairs 2021). However, these schemes have suffered from delays in implementation, and also lack key details which make a full assessment of their sufficiency challenging.

Increasing carbon sequestration in agriculture will require freeing up some land that is currently under agricultural production for alternative uses such as afforestation. This can be achieved by productivity improvements in farming (producing the same level of food with less land), or by demand measures such as dietary change and food waste reductions (which can reduce the demand for certain land-intensive products such as meat and dairy).

The Government’s strategy relies heavily on productivity improvements to free up agricultural land, while neglecting the potential for demand-side solutions. The Net Zero Strategy envisages that up to 7 MtCO2e of emissions could be saved by productivity improvements, and aims to achieve this via the Farming Investment Fund (UK Government 2022g), which provides payments to drive productivity improvements on farms.

The strategy fails to address possible demand measures in agriculture, most notably dietary change and food waste prevention. The Government Food Strategy does not introduce measures to support and accelerate dietary shifts, despite the clear health benefits of doing so, and the evidence of consumer appetite for reduced meat consumption (UK Government 2022i, Stewart et al 2021). The Food Strategy also only addressed food waste from large businesses, despite the majority of food waste occurring at the household, farm and supply-chain stages.

The UK has updated the methodology it uses for calculating emissions from peatland which has turned the historical LULUCF sector from an emissions sink into an emissions source (Evans et al 2017, UK Government 2022h). LULUCF was responsible for around 1% of total emissions in 2021 (BEIS 2022d). Achieving a strong LULUCF sink in the UK will require protecting and restoring degraded peatland, and large-scale afforestation.

The UK has one of the lowest level of forest cover in Europe, at 13% (Forest Research 2022). The Government has set a target of planting 30,000 ha/y by 2025, which is aligned with the CCC’s recommendations. This would need to rise further to 50,000 ha/y by the mid-2030s.

Afforestation policy is the responsibility of the devolved administrations, with different policies in each region. In England, the England Tree Action Plan commits GBP 500m of funding to support afforestation between 2020 and 2025 (UK Government 2021b). This will drive tree planting rates to 7,000 hectares a year by 2025, around 20% of the UK’s total target.

The plan also considers developing carbon markets to drive private investment in afforestation. Over 80% of UK afforestation takes place in Scotland (Forest Research 2021), which recently updated its tree-planting targets from 12,000 ha/yr to 18,000 ha/yr by 2024/5 (Scottish Forestry 2021). Meanwhile, Wales aims to plant 43,000 ha of new forest by 2030 (Welsh Government 2021b).

Policy to protect and restore degraded peatland is still lagging in the UK. The Government has committed to restore 280,000 ha of peat in England by 2050, which represents only 20–40% of England’s peat (UK Government 2021a, Evans et al 2017). Likewise, the Government’s ban on rotational burning of peat applies to only 9% of peatland, despite the CCC recommending a complete ban on the practice (CCC 2020, WCL 2021). Further action to protect and restore the UK’s peatlands is urgently needed.

Further analysis

Latest publications

{kind=link}

Stay informed

Subscribe to our newsletter