China

Policies & action

Record-high renewable deployment is sufficient to meet China’s growing electricity demand, curb coal-fired power generation, and reduce CO₂ emissions in the power sector. At the same time, increased EV uptake, declining cement and steel output, and deeper electrification and efficiency gains in building operations have stabilised or reduced CO₂ emissions in non-power sectors.

If China sustains policy interventions that secure a downward emissions trajectory, it could lock in a 2025 peak in emissions.

- In CAT conservative scenario, China’s emissions are projected to decline gradually, with an average annual reduction of 0.5% through 2035, reaching 4% below peak levels by 2035.

- In CAT optimistic scenario, featuring accelerated renewable deployment in line with the 15th FYP target of doubling non-fossil energy supply over the next decade, emissions decline more rapidly at an average rate of 2.7% per year. This pathway would result in an additional 20% reduction in emissions by 2035 relative to the conservative scenario.

New targets announced in the 15th Five Year Plan, combined with revisions to historical emissions data, have lowered the CAT’s projections of China's average absolute emissions by around 6% in 2030 and 4% in 2035 compared to the previous assessment.

However, the pace of China’s energy transition remains insufficient to align with limiting warming to 1.5°C. China’s overall policies and action rating remains “Insufficient.” The “Insufficient” rating indicates that China’s climate policies and action in 2030 need substantial improvements to be consistent with limiting warming to 1.5°C. If all countries were to follow China’s approach, warming would reach over 2°C and up to 3°C.

Further information on how the CAT rates countries (against modelled domestic pathways and fair share) can be found here.

Policy overview

China’s current policies scenario projections have been updated to reach GHG emission levels (excl. LULUCF) of 13.7-14.4 GtCO₂e in 2030 and 11.2-14.2 GtCO₂e in 2035. This represents an additional 4-6% of emission reductions compared to the previous assessment, mainly driven by revisions to historical emissions data and targets announced in China’s 15th Five-Year Plan (FYP).

In the 15th FYP, China targets a non-fossil fuel share in energy consumption of 25% by 2030 and 30% by 2035, and a 17% reduction in CO₂ intensity from 2025 levels by 2030 (National People’s Congress of China, 2026). These targets are conservative and achievable without additional policies, even under the CAT’s conservative current policy projection (CPP).

China also aims to double non-fossil energy supply by 2035 from 2025 levels, which adds significant ambition and could deliver around 10% emissions reduction by 2035 under the CAT's optimistic CPP. However, the 15th FYP still contains notable gaps, including the continued prioritisation of domestic gas exploration for energy security and the absence of a clear coal phase-down plan.

China’s CO₂ emissions may have peaked in 2025, following a “flat or declining” trend from March 2024 through year-end. In Q1 2026, emissions rose slightly by 2% due to increased wind and solar curtailment, but remained below the early-2024 peak (Myllyvirta, 2026b, 2026a). The CAT estimates total GHG emissions at 14.8 GtCO₂e in 2025 (excl. LULUCF), with CO₂ emissions declining by 0.1% year on year. This decline in CO₂ emissions is being driven by structural changes in China’s economy, including the clean transition in the power sector, accelerated electrification in transport, and reduced cement and steel production.

China’s clean energy economy continues to outpace overall economic growth. Solar power, batteries, electric vehicles (EVs), and related technologies drove more than one third of total economic growth in 2025 and accounted for over 90% of the net increase in investment (Myllyvirta and Schäpe, 2026). China also continues to dominate the global energy transition supply chain, manufacturing over 80% of solar panels, 60% of wind turbines, and 75% of EVs and their batteries worldwide (IEA, 2022; Hayley, 2024; Lombardo et al., 2025).

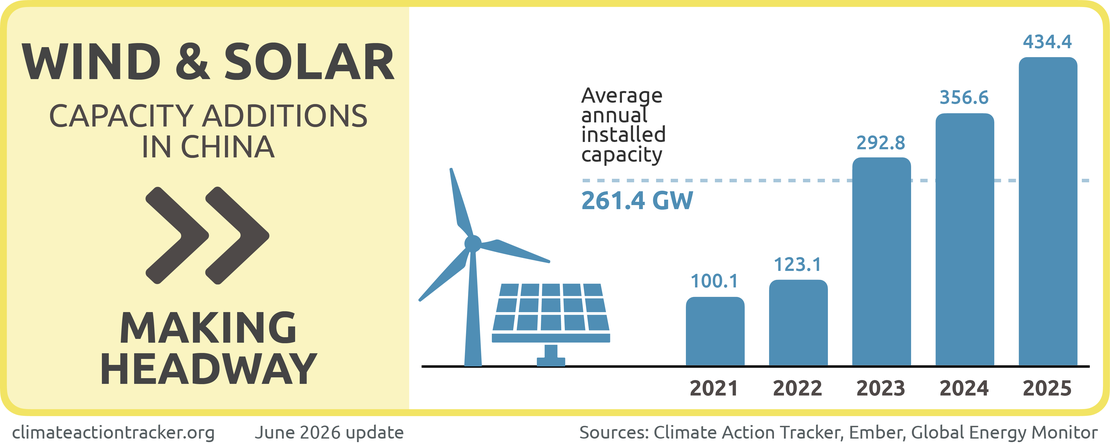

China’s rapid renewable deployment is a central driver of power sector decarbonisation. In 2025, a record 430 GW of wind and solar capacity was added, raising total capacity to 1,840 GW. However, continued fossil expansion creates a structural tension. By end-2025, 291 GW of coal capacity remained in the pipeline, despite declining coal demand in the power sector, increasing the risk of carbon lock-in and stranded assets.

Deep electrification is advancing in China. From 2015 to 2025, electricity’s share of final energy consumption increased from 23% to 30% (Ember, 2025; CREA, 2026a). Electrification-driven fossil fuel displacement has been concentrated in industry and transport, which together accounted for 85% of the total. Within this, the expansion of EVs alone contributed 16%, underscoring their growing role in reducing oil demand (Ember, 2025).

China’s 15th Five-Year Plan for a “new-type energy system” sets an electrification target for the first time, aiming to raise electricity’s share of final energy consumption to 35% by 2030, achieving the level envisioned in the COP31 global electrification goal (2035) five years ahead of schedule (NDRC, 2026).

Emissions in China’s heavy industry are generally on a declining trend, with the chemical sector representing a significant exception. China’s growing demand for upstream inputs for plastics production, coupled with declining coal use in the power sector and falling coal prices, has accelerated the expansion of coal-based polyolefin pathways.

As a result, in 2025, coal consumption in the chemical sector increased by 15%, contributing to a 12% rise in emissions. This growth partially offset broader industrial decarbonisation trends: absent the increase from the chemical sector, China’s total emissions would have declined by approximately 2%, compared to the estimated reduction of 0.3% (Myllyvirta, 2026b).

In the cement and steel industries, observed reductions are primarily driven by weakening demand rather than substantive structural decarbonisation. Cement production has fallen to its lowest level since 2010, while steel output has declined to levels last seen in 2018 (SunSirs, 2026a; Yermolenko, 2026).

The transition to green steel and broader industrial decarbonisation is becoming increasingly urgent as the EU’s CBAM, due in 2026, is expected to weaken the competitiveness of emissions-intensive exports. China expanded its national ETS in 2025 to include cement, steel, and aluminium, aiming at accelerating the transition. This is complemented by additional policy tools, including energy efficiency improvements, capacity replacement schemes, and electrification incentives.

China has revised its definition and measurement of carbon intensity, introducing changes that weaken target stringency and increase uncertainty in tracking progress. The new methodology lacks clear rules and appears to depart from the previous scope in two key ways: it incorporates additional industrial process emissions, notably from the cement sector, where output and emissions have been declining; it excludes emissions from the non-energy use of fossil fuels, particularly in the rapidly expanding chemical industry.

These shifts in coverage mechanically reduce measured carbon intensity, helping to explain why reported improvements appear faster under the revised methodology (Myllyvirta, 2026c).

Deepened electrification in the transport sector, with EVs exceeding 50% market share and 12% of vehicle stock in 2025, has stabilised oil consumption and driven down CO₂ emissions in the sector (Xinhua News Agency, 2026a, 2026c).

Buildings sector emissions are entering a phase of stabilisation, with growth slowing after a decade of increases. This trend is driven by urbanisation saturation, efficiency improvements, and accelerated electrification of end uses. In parallel, the sector’s energy mix is decarbonising, with increasing reliance on lower-carbon electricity and cleaner heating through the expanded deployment of heat pumps, distributed solar, and low-carbon district heating systems.

China has overachieved its 2030 NDC target of increasing forest stock by six billion m³ from 2005 levels and has raised the target to 11 billion m³ by 2035 in its updated NDC. This progress reflects sustained afforestation efforts, including large-scale programmes such as the 300,000 km² Three-North Shelterbelt and the 3,000 km green belt encircling the Taklamakan Desert (Reuters, 2024; CGTN, 2025). Forest coverage has reached 25%, with a further increase to 26% targeted by 2035 (Xinhua News Agency, 2025d).

Power sector

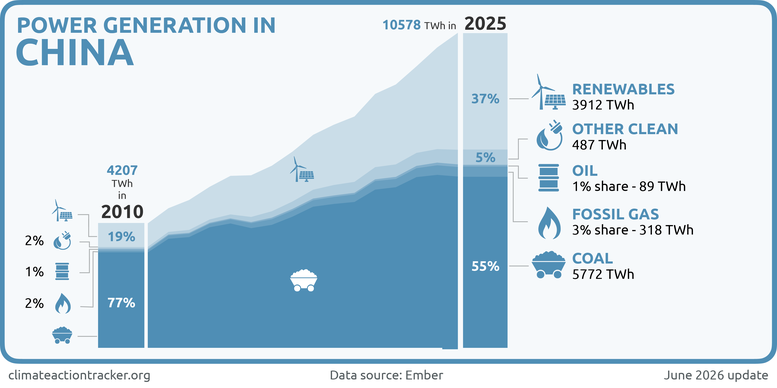

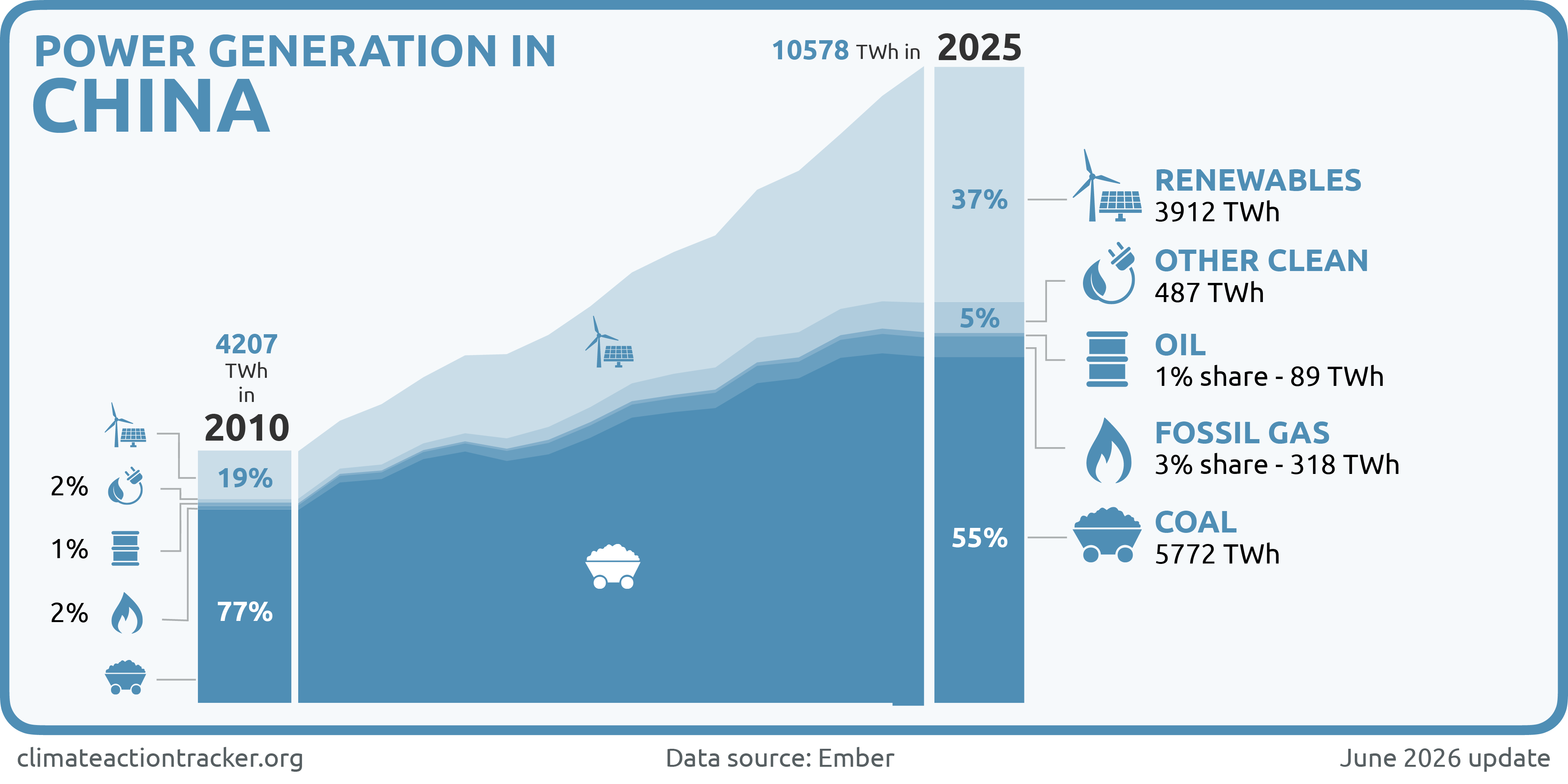

The power sector is the largest source of GHG emissions in China, with power demand exceeding 10,000 TWh and accounting for more than one third of global consumption. China’s power sector exhibits two opposing trends.

On one hand, China leads global renewable deployment. Wind and solar generation doubled between 2022 and 2025, reaching 22% of total supply. This growth met rising electricity demand and drove a decline in fossil‑based generation in 2025, the first in over a decade.

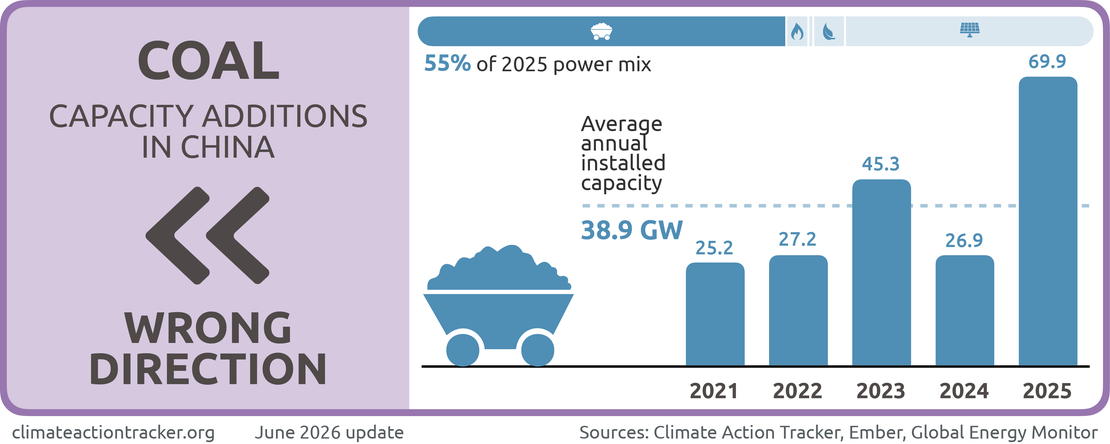

On the other hand, coal remains dominant, although its share fell from 70% in 2015 to 55% in 2025. Despite declining utilisation and profitability across the coal fleet, new capacity continues to be approved and constructed at scale, increasing risks of carbon lock‑in and stranded assets.

Coal

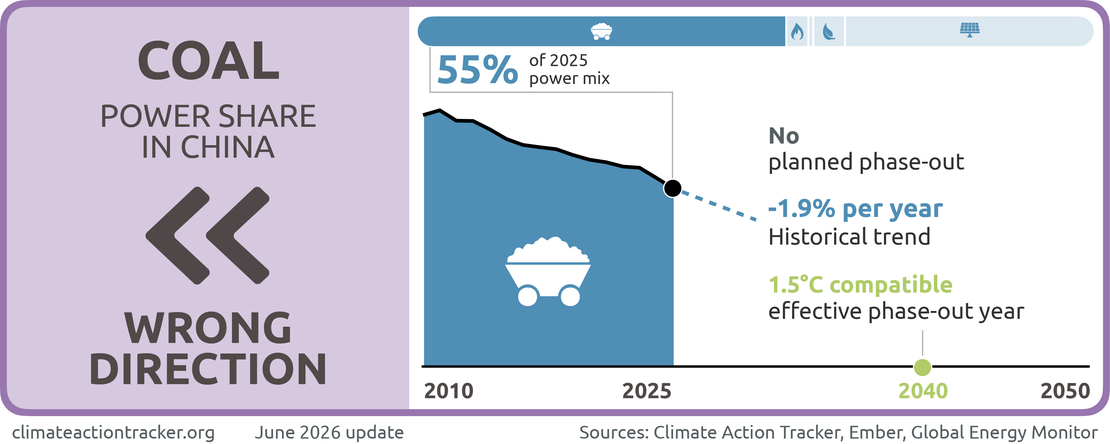

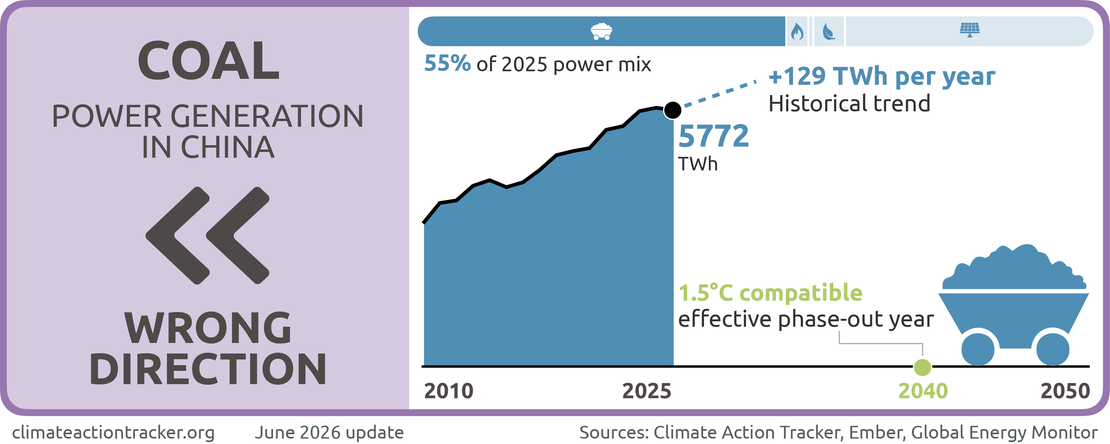

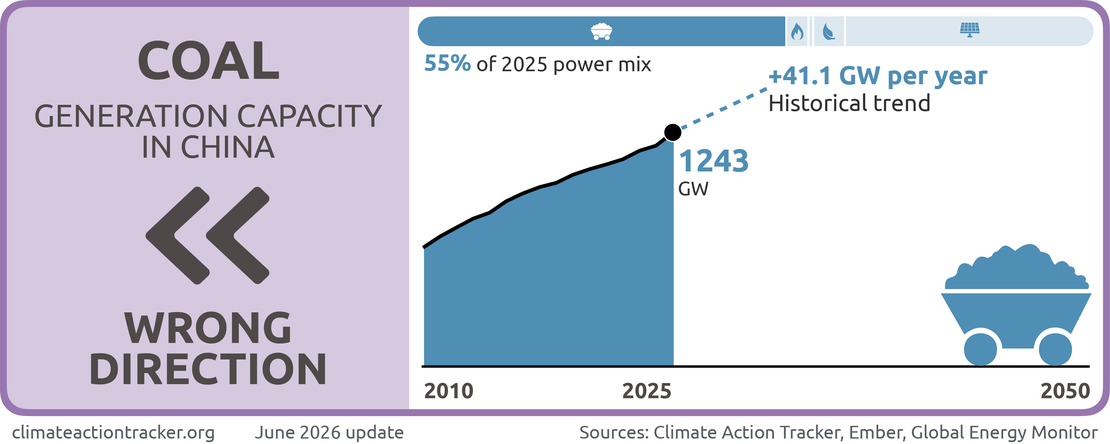

China remains the world’s largest producer, importer, and consumer of coal. Coalfired generation grew by over 3% annually between 2020 and 2024, before declining in 2025, while its share of the power mix fell at a similar pace. There is no coal phaseout target, and substantial additional capacity is planned. Progress in this sector is assessed as “Wrong direction”.

Declining coal‑fired generation alongside continued coal capacity expansion creates a structural contradiction. Under current policies, the CAT projects the coal-based power generation declines by around 3% from today towards 2030, while we project the coal capacity will continue increasing.

In 2025, China’s new and reactivated coal power project proposals surged to a record 161 GW. By year end, 291 GW of coal capacity remained in the pipeline, including permitted and under-construction projects (Qin and Christine Shearer, 2026). This expansion partly reflects a legacy of the permitting surge that began in 2022 in response to power shortages linked to limited system flexibility.

But this build-up occurs despite coal plants becoming more expensive to operate as cheaper renewables are added to the grid. In China, coal-generated electricity is typically 1.5 to 3 times more expensive than power from solar and onshore wind. When full system and compulsory decarbonisation costs are taken into account, coal-fired power ranges from approximately $0.059 to $0.087 per kWh, compared with $0.029 to $0.042 per kWh for solar and $0.017 to $0.035 per kWh for onshore wind (CPEM, 2025).

High power generation costs, coupled with decreasing renewable electricity prices, have led to financial losses and generation inefficiencies for coal companies. If the pipeline projects proceed without accelerated retirements, utilisation rates across the coal fleet, which stood at 50% in 2024, are likely to decline further, exacerbating overcapacity and stranded asset risks (Qin and Myllyvirta, 2025).

Given China’s large operating and pipeline coal capacity, the viable pathway to meet climate targets is to ensure that these plants only play backup roles before retiring at the end of their lifespans. They would support high renewables penetration while operating at lower utilisation and reduced efficiency.

China’s NDC targets allow no growth in power sector emissions, and the 15th FYP signals a gradual shift away from fossil fuels and an increasing share of wind and solar in the energy mix. The CAT’s current policy projections indicate that coal’s share could fall to around 40% by 2030, while a 1.5°C-aligned pathway requires a much steeper decline and a complete phase-out before 2040 (Climate Action Tracker, 2026).

While shifting away from coal is essential for achieving a 1.5oC-compatible power system, reducing emissions from coal plants that will remain in use for some time through technical improvements is still sensible before 2040 (Climate Action Tracker, 2026).

China planned a set of "low carbon" retrofitting projects for selected coal power plants during 2024 to 2027 (NDRC and NEA, 2024). The target is an average 20% reduction in CO₂ intensity per kWh by 2025 compared with comparable plants in 2023, rising to 50% by 2027, approaching the level of gas‑fired power plants. Reductions will depend on biomass co-firing, green ammonia co-firing, and CCUS technologies, all of which remain costly and technically unproven at scale, posing significant risks to widespread deployment.

This strategy also raises the cost of coal-fired power, encouraging a further shift to renewable energy when much of China’s coal-fired generation is already unprofitable even before incurring the costs of new measures (Myllyvirta, 2024). It is, however, crucial to ensure that these low-carbon retrofits do not become an excuse for new coal projects or delaying the phase-down of existing coal plants.

With coal being squeezed out from the power supply by renewables, China is accelerating a transition in coal use from a single energy source to a dual role as both fuel and feedstock, with the emergence of the coal chemicals industry. Technological breakthroughs and expanding capacity in coal-to-liquid fuels, coal-to-gas, and coal-to-ethylene glycol are driving this shift (China National Coal Association, 2025).

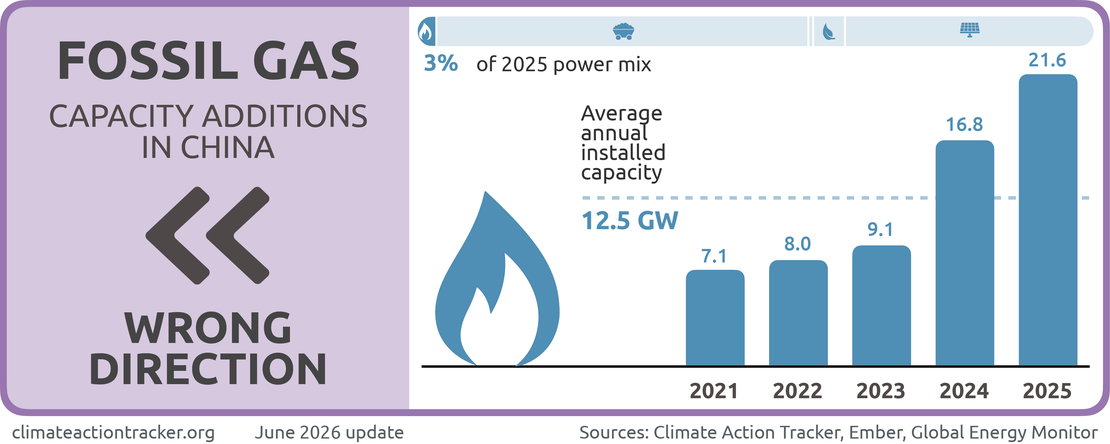

Fossil gas

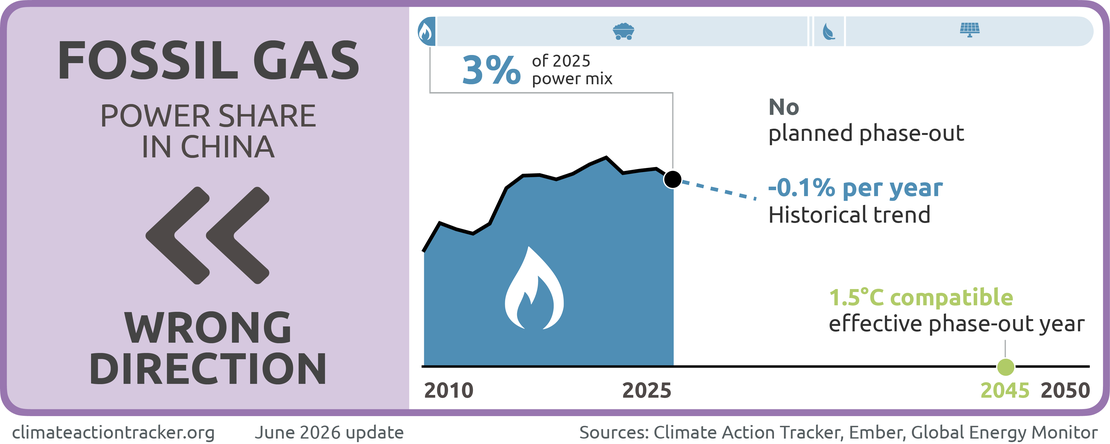

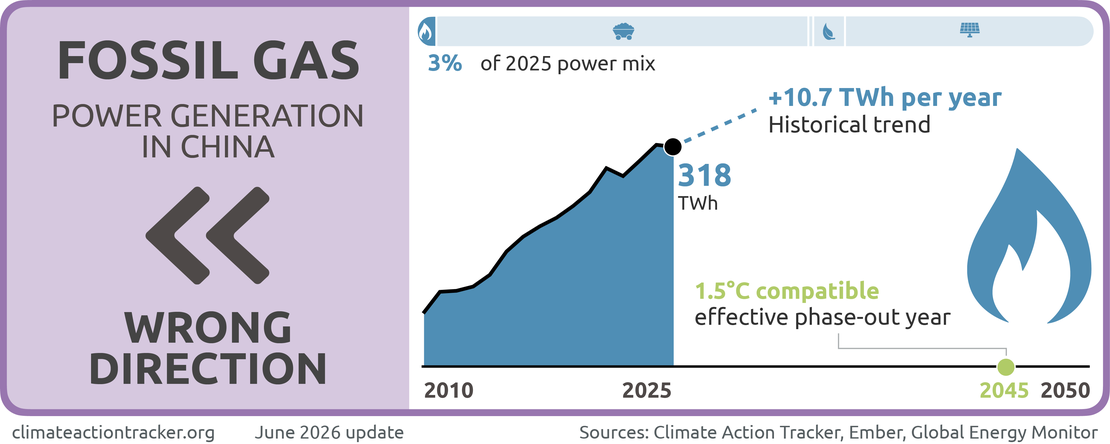

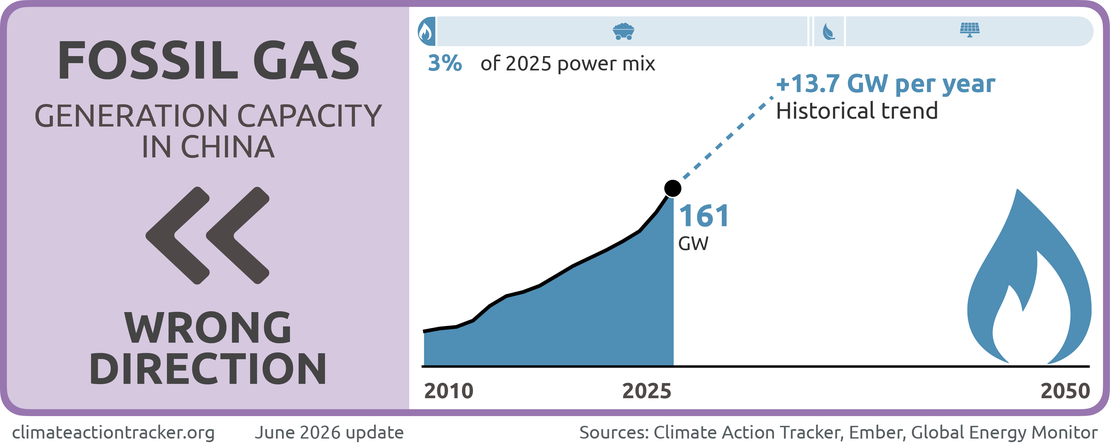

Fossil gas plays a minimal but growing role in China’s power sector. Gas‑fired generation increased by nearly 6% per year over the past five years, while its share of the power mix stabilised at around 3%. There is no gas phase‑out target, and additional capacity is planned. Progress in this sector is assessed as “Wrong direction”.

China installed a record 22.4 GW of gasf-ired power capacity in 2025, accounting for over one third of the global total of 60.4 GW commissioned that year (Jenny Martos, 2026). Gas-fired generation is projected to grow by 3-5% annually on average to 2030. However, a 1.5°C trajectory requires reducing gas use in power generation, with a complete phaseout by 2040 (Climate Action Tracker, 2026).

In the 15th FYP, the government emphasises “scale expansion” and “high-quality development” in the fossil gas sector, positioning these goals as essential for enhancing energy security and supporting grid flexibility. Supported by measures such as accelerating the construction of trunk pipeline networks and storage infrastructure, China’s fossil gas consumption is projected to reach close to 500 billion m3 by 2030, up from the current level of 427 billion m3 (SunSirs, 2026b).

Renewables

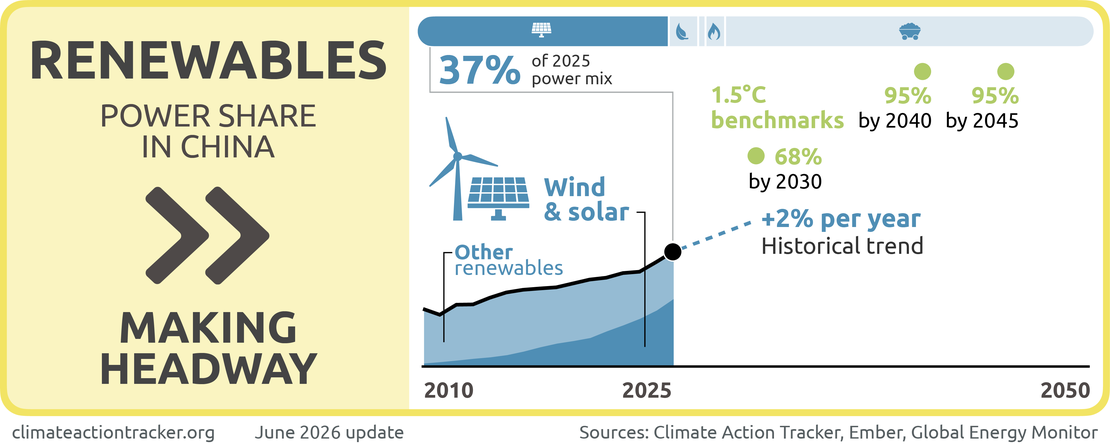

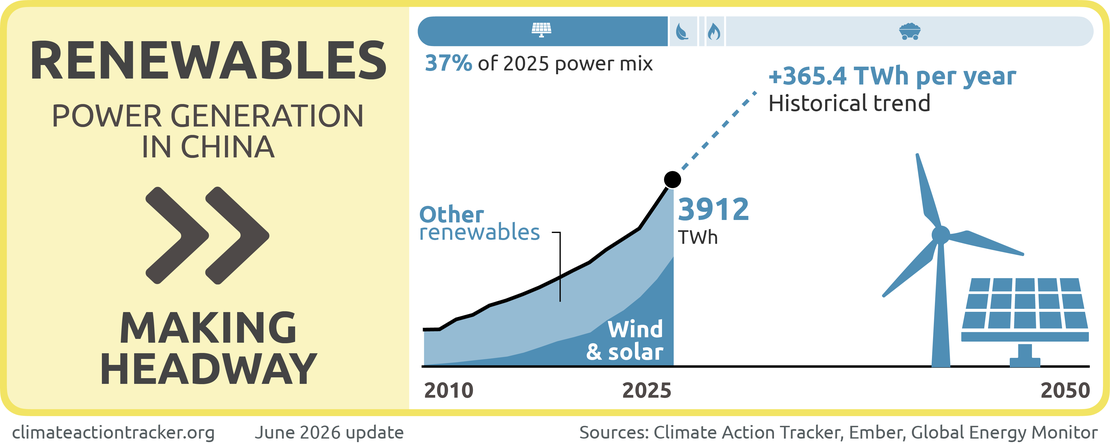

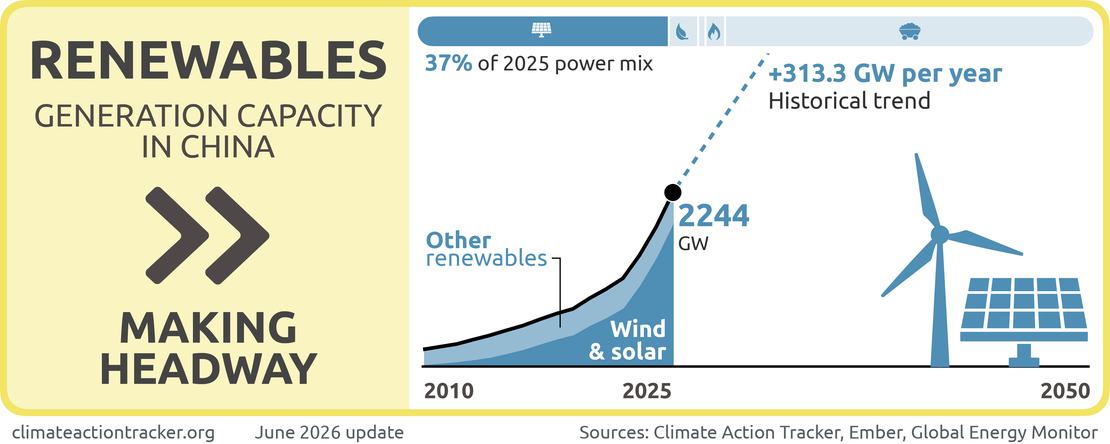

China’s renewable deployment is “Making Headway”, with its share rising from around 28% to 37% over the past five years. In 2025, China added a record 430 GW of wind and solar capacity, bringing total renewable capacity to 2,395 GW, accounting for over 60% of installed power capacity (NEA, 2026a).

In 2025, renewable-based generation accounted for 37% of the power mix, with wind and solar making up almost 22% of China’s electricity generation. A recent analysis by the CAT shows that aligning China’s power sector with a 1.5°C pathway would require renewables to supply 68% of electricity generation, with wind and solar alone providing 53% by 2030. Meeting this trajectory would require average annual additions of around 310 GW of solar and 150 GW of wind capacity to 2030. Combined wind and solar capacity would need to reach about 4,500 GW by 2030 (Climate Action Tracker, 2026).

Under current policies and market trends, CAT projects installed wind and solar capacity could reach up to 4,277 GW by 2030, implying a small residual gap in ambition and implementation relative to a 1.5°C pathway.

To create stable demand for rapidly expanding wind and solar, China introduced the Electricity Demand Side Management Measures in 2023, requiring each province to achieve demand response capacity equivalent to 3% to 5% of peak load (NDRC, 2023). Building on this, the government released a draft in 2025 outlining implementation procedures, compliance mechanisms, and penalties (NDRC, 2025).

Renewable energy consumption in China remains constrained by the inflexible operation of coal power plants and the grid. In the first quarter of 2026, China’s CO₂ emissions rose by 2% year-on-year, alongside increased curtailment of wind and solar generation. This is largely driven by the existing system of medium and long-term contracts, under which coal-fired plants are required to supply fixed volumes of electricity at predetermined prices, leaving little incentive to adjust output to accommodate renewable generation (Myllyvirta, 2026a).

The government has implicitly acknowledged these challenges and is promoting reforms to address them. These include expanding trans-provincial power trading, improving the operational flexibility of coal-fired plants, enhancing the integration of energy storage into the grid, and reforming electricity pricing mechanisms to reduce curtailment.

China is expanding transmission and storage capacity. Energy storage reached 144.7 GW in 2025, accounting for over half of the global total, with a target of 180 GW by 2027 (Reuters, 2025; NEA, 2026b). As of October 2025, China had 45 ultra-high voltage transmission lines in operation. A further 15 lines are planned for 2026 to 2030. These are expected to enable around 200 GWh of renewable electricity to be connected annually and increase cross‑provincial transmission capacity by 35% (Reuters, 2026b).

China's distributed renewable capacity, predominantly composed of rooftop solar, reached approximately 530 GW by the end of 2025. In its 15th FYP for the energy system, China aims to develop an integrated platform that optimise coordination across generation, grid, load, and storage. By 2030, these upgraded systems are expected to accommodate around 900 GW of distributed renewable energy capacity, effectively enabling the addition of nearly 100 GW of distributed renewables per year (NDRC, 2026).

Nuclear

Nuclear accounts for 4-5% of China’s total power generation and is viewed as a strategic source that enhances energy security while reducing reliance on fossil fuels.

China operates the world’s fastest-growing nuclear fleet. By end-2024, it had 57 reactors in operation with a total capacity of 59.76 GW, and 28 units under construction totalling 33.7 GW. The China Nuclear Energy Association projects installed capacity to reach 110 GW by 2030 and 200 GW by 2040, with nuclear generation accounting for 10% of total power supply (CNEA, 2025).

China’s 15th Five-Year Plan for the energy system promotes the integrated use of nuclear energy based on local conditions (e.g., power generation, district heating, and industrial applications), while targeting around 110 GW of nuclear capacity in operation by 2030 (NDRC, 2026).

However, nuclear remains less economical and slow to install, even in China, compared to wind and solar. We have not integrated these projections of nuclear buildout in our current policies projections pending further developments.

Industry

Industry is the largest energy-consuming sector in China, accounting for almost 60% of the country’s total final consumption (IEA, 2025). Industrial energy demand is expected to plateau over the coming decade, with emissions stabilising as a result of increased electrification and improvements in energy efficiency.

The national emissions trading scheme (ETS) expanded significantly in 2025, with the inclusion of the steel, cement, and aluminium sectors adding more than 1,300 key emitters and increasing coverage to over 60% of national CO₂ emissions (MEE, 2025, 2026). Despite reaching a record annual trading volume of 235 MtCO₂e and a total turnover of USD 2.2bn, the ETS currently provides limited incentives for industrial decarbonisation due to the absence of a binding emissions cap and the continued reliance on predominantly free allowance allocation. As a result, the scheme has yet to establish a sufficiently strong carbon price to drive substantial emission reductions.

China has outlined plans to progressively strengthen the ETS by expanding coverage to all major emissions-intensive industries by 2027, introducing a cap-and-trade system with both free and auctioned allowances by 2030, and extending coverage to all major high-emitting sectors by 2035 (Xinhua News Agency, 2025c, 2025d). If effectively implemented, these reforms could strengthen carbon pricing signals, drive deeper industrial emissions reductions, and accelerate the green transition of heavy industry.

Steel

China produces over half of global crude steel, with the sector accounting for 16-17% of national CO₂ emissions (Yermolenko, 2024). Emission reductions to date have been driven primarily by declining demand rather than a structural shift towards low‑carbon production. Steel output fell to 961 Mt in 2025, the lowest since 2018, exceeding the scale of reductions implied by policy targets (Yermolenko, 2026).

To achieve a 1.5°C-compatible steel industry, China must cease building new coal-based steel plants and retire its emissions-intensive blast furnace-basic oxygen furnace (BF-BOF) facilities. The resulting capacity gap should be filled through increased scrap recycling and green hydrogen-based direct iron reduction (DRI), with steelmaking prioritising the use of electric arc furnaces (EAF) powered by clean energy (Climate Action Tracker, 2024).

The green steel transition in China is sluggish, with slow progress in shifting away from BF-BOF steelmaking. China targets an EAF capacity share of 15% by 2025 and 20% by 2030, but the share remained close to 10% through 2025 (Transition Asia, 2024; CREA, 2026b). Structural overcapacity, weak steel prices, and compressed margins have constrained the transition. Compared with BF-BOF producers that benefit from economies of scale, EAF steelmakers face higher electricity costs and thinner margins, resulting in slower capacity expansion and lower utilisation rates.

In 2026, the government revised its Steel Capacity Replacement Implementation Measures, raising the nationwide replacement ratio for both ironmaking and steelmaking to no less than 1.5:1 requiring more old capacity to be retired for each unit of new capacity (MIIT, 2026). The policy introduces differentiated rules for EAF and hydrogen‑based metallurgy, aiming to promote lower‑carbon industrial upgrading while constraining overcapacity.

Hydrogen applications in steel decarbonisation are gaining momentum. In March 2026, the government launched a pilot programme rewarding five city clusters for achieving hydrogen deployment targets, with a focus on promoting the steel sector’s transition through the use of low-carbon hydrogen (Dialogue Earth, 2026).

China published its National Hydrogen Strategy (2021–2035) in 2022, confirming the technology’s key role in China’s future energy system and mitigation efforts. China's total green hydrogen production capacity built or currently under construction hit more than 1 Mt per year by the end of March 2026. Of that, over 250,000 tonnes per year is already completed and operational. A further 900,000-plus tonnes per year is under active construction (Fuel Cells Works, 2026). Under the 15th Five-Year Plan, China aims to double this level to 2 Mt annually by 2030 (NDRC, 2026).

China’s H₂-DRI steelmaking pipeline is expanding, led by major producers such as Baowu Steel and HBIS. In late 2025, Baowu commissioned a 1 Mtpa hydrogen DRI–EAF production line in Zhanjiang. HBIS operates the other large-scale hydrogen-based steel facility in Zhangjiakou, with a capacity of 1.2 Mtpa (Dialogue Earth, 2026).

Cement

China produces more than half the world’s cement, generating 13-15% of its national CO2 emissions (Climate Analytics, 2025). Similar to steel, CO₂ emission reductions are mainly driven by weaker demand due to the slowdown in real estate and infrastructure construction, although efficiency improvements, electrification, alternative fuels, clinker substitution, and carbon capture technologies are gaining policy attention. In 2025, China’s cement production declined to 1,693 Mt, the lowest since 2010, while overcapacity and shrinking demand continued to erode profitability (SunSirs, 2026a).

China’s cement policies align with its “dual carbon” goals of peaking emissions before 2030 and achieving carbon neutrality before 2060. In 2024, the government released an action plan for cement sector decarbonisation, targeting a reduction of around 13 MtCO₂ during 2024 to 2025 through industrial retrofits and equipment upgrades, alongside energy savings of 5 Mtce (NDRC, 2024). China also mandated ultra‑low‑emissions retrofits for cement clinker production capacity, targeting 50% completion in key regions by 2025 and 80% nationwide by 2028 (MEE, 2024).

To decarbonise hard‑to‑abate sectors, China is prioritising carbon capture, utilisation, and storage (CCUS). By end‑2024, China had 15 CCS projects operating with a total capacity of 4 million tonnes per annum CO2 captured (Shangyou Nie, 2025). Chinese cement producers have made early progress on CCUS, but commercial deployment remains distant. Costs are a key barrier: building a CO₂ capture facility in China is estimated to cost around three times that of a clinker plant, with similarly high operating costs (Climate Analytics, 2025).

Chemicals

China is the world’s largest producer and consumer of plastics. Despite relatively higher production costs compared to conventional oil and gas-based feedstocks, the country’s abundant coal reserves and declining demand for coal in power generation have incentivised the expansion of coal-based polyolefin pathways.

The chemicals industry is now the largest driver of energy consumption and emissions growth in China. Coal and oil use increased by 15% and 10% respectively, driving a 12% rise in the sector’s CO₂ emissions (Myllyvirta, 2026b). As coal prices fall and coal demand in the power sector declines, major coal producers are turning more towards high-margin coal-based chemical production, where profits can be 8 to 12 times higher. Without intervention, emissions from the chemicals sector could increase to 1.3 times above 2019 levels by 2030, putting China’s climate goals at risk (Qiu and Schäpe, 2024).

Transport

China’s transport sector accounts for 14% of final energy use and 43% of oil consumption (IEA, 2026). Decarbonisation is progressing rapidly, driven by deep electrification led by electric vehicles (EVs). As a result, oil demand for transport fuels has plateaued (Healy et al., 2025).

Passenger vehicles are the largest energy consumers in the transport sector. The government set targets in 2021 for new energy vehicles (NEV), including plugin hybrid EVs and battery EVs, to reach 20% of new sales by 2025 and 40% by 2030 (Government of China, 2021). Actual progress has exceeded these targets. NEVs accounted for 50% of new vehicle sales in 2025, increasing to a record 63% in May 2026 (Evans, 2026; Xinhua News Agency, 2026a). NEVs now make up over 12% of all vehicles on the road in China (Xinhua News Agency, 2026c).

By end-2025, China had built 20.1 million EV charging facilities, supporting 43 million NEVs. The network is set to expand further, with plans to reach 28 million charging points by 2027 and 40 million charging points by 2030 (Bai et al., 2026; NDRC, 2026).

The rapid growth in NEV sales was initially driven by central purchase subsidies introduced in 2009, which ended in late 2022. Current support mainly includes purchase tax exemptions, trade-in programmes, and regional incentives (Xinhua News Agency, 2023; Zhang, 2025).

China’s EV and battery industries have evolved from heavy reliance on subsidies to becoming major drivers of economic growth. In 2025, these sectors contributed 44% of the economic impact and more than half of the growth in clean energy industries, driven by strong expansion in both output and investment (Myllyvirta and Schäpe, 2026).

Meanwhile, highly competitive Chinese automakers are expanding in international markets. In response to China’s dominance in the global EV market, the EU, US, and Canada have introduced tariffs or import restrictions on Chinese-made EVs to counter perceived market and price advantages, with further policy developments remaining uncertain (Song et al., 2024).

The government is also prioritising the electrification of heavy-duty trucks, scaling local electric transit, and expanding the highspeed rail network.

EVs accounted for 29% of new heavy truck sales in China in 2025, with the monthly share reaching 54% in December 2025 (Parkinson, 2026). The government targets EVs to reach 40% of new heavy truck sales by 2030 and 20% of the total fleet (Reuters, 2026a).

New energy city buses exceeded 80% of new sales and reached 100% in pilot cities such as Shenzhen and Taiyuan, supported by policy incentives and mature supply chains (Xinhua News Agency, 2025b). The transition of the fleet for trucks will be faster than for passenger cars, as lifetimes are shorter.

By end-2024, China's operational railway network had reached 162,000 km, with more than 120,000 km, or 75.8% electrified (Li, 2025). By end‑2025, the fully electrified high‑speed rail network exceeded 50,000 km, with operating speeds of up to 350 km/h (Xinhua News Agency, 2025a).

Decarbonising the power grid is as critical as transport electrification. With coal still dominant in the electricity mix, a high EV share does not automatically translate into lower transport emissions.

Buildings

China’s buildings sector lifecycle, spanning materials production and transport, construction, and operation, accounts for up to 38% of national carbon emissions, ranking second only to the power sector (Caixin Insight, 2024).

In 2021, building operations accounted for 22.0% of China’s final energy consumption and 21.7% of energy-related CO₂ emissions, while construction contributed a further 22.7% of final energy use and 26.6% of emissions (Tsinghua University BERC, 2025).

Emissions from building operations have risen over the past decade but are now decelerating, with a medium-term plateau likely. Drivers include urbanisation saturation, efficiency gains, and rapid electrification of end uses such as heating and appliances. During the 14th FYP (2021–2025), large-scale retrofits improved performance, with public building energy efficiency rising by 20%. By end-2024, energy-efficient buildings accounted for over 66% of existing urban floor space. In 2024, electricity consumption accounted for over 55% of China's total building energy consumption (China’s State Council Information Office, 2025).

The government developed the “Green Building Evaluation Standard” in 2019, which includes a set of indicators such as safety and durability, health and comfort, user convenience, environmental responsibility, and resource efficiency, including energy conservation. In 2024, the floor space of China's new green buildings accounted for almost 98% of all newly constructed buildings in urban areas (China’s State Council Information Office, 2025).

The buildings sector’s energy mix is shifting towards lower-carbon electricity and cleaner heating, driven by wider deployment of heat pumps, distributed solar, and decarbonised district heating. In northern regions, large-scale transition from coal-based systems to gas, electric, and renewable heating has progressed since 2017, with over 40 million rural households retrofitted. By end-2024, clean heating accounted for 83% of supply in northern China, an increase of nearly 20% since 2020 (China’s State Council Information Office, 2025).

For compatibility with the Paris Agreement temperature goals, China’s emissions intensity in residential and commercial buildings needs to be reduced by at least 65% in 2030, 90% in 2040, and 95-100% in 2050 below 2015 levels, while energy intensity needs to be reduced by at least 20% in 2030, 35-40% in 2040, and 45-50% in 2050 compared to 2015 levels. China will also need to achieve renovation rates of 2.5% per year until 2030 and 3.5% until 2040 to achieve a Paris-compatible buildings sector by 2050 (Climate Action Tracker, 2020).

Forestry

China’s forests and grasslands absorb over 1.2 GtCO₂e annually, making them the largest carbon sink globally, according to government estimates. This sink is projected to offset over half of residual emissions by 2060, positioning it as central to carbon neutrality (Xinhua News Agency, 2024).

In 2021, China signed the Glasgow Declaration on Forest and Land Use (which commits to “halt and reverse” forest loss and land degradation by 2030) at COP26 and issued separate joint agreements with both the EU and the US on enhancing cooperation on reducing deforestation around the same period (Directorate-General for Climate Action, 2021; United States Department of State, 2021).

Afforestation is expected to play a key role in expanding sequestration capacity; however, climate benefits depend on forest quality, species composition, and long-term management. From 2000 to 2020, China gained 6.7 Mha of tree cover, equal to 5.0% of the global total (Global Forest Watch, 2026).

By the end of 2024, China’s forest coverage exceeded 25%, driven by large-scale afforestation efforts such as the Three-North Shelterbelt Forest Program, which has added over 300,000 km2 of forest (CGTN, 2025). In the same year, the completion of a 3,000-kilometre green belt around the Taklamakan Desert marked a major milestone in desertification control, helping reduce desertified land to 26.8% of the national territory (Reuters, 2024).

However, assessments of the carbon sequestration potential of China’s forests contain uncertainties in science and accounting, leading to diverging estimations (e.g., Qiu et al., 2020; Yu et al., 2022). Thus, for Paris Agreement compatibility, sinks from the forestry sector cannot be used as an excuse to delay emission reductions in other sectors (Climate Action Tracker, 2016).

China’s 2030 NDC committed to increasing forest stock volume by 6 billion m³ from 2005 levels, targeting an estimated 18.5 billion m3. It achieved this target ahead of schedule, with forest stock reaching 20 billion m³ in 2024 (China’s State Council Information Office, 2025). Under the updated 2035 NDC, China has raised its targets to 24 billion m³ of forest stock and 26% forest coverage (Xinhua News Agency, 2025d).

Methane

Methane accounts for 11.7% of China’s total GHG emissions, with coal mine fugitives as the dominant source, contributing around 40% of methane emissions (Government of China, 2025). However, their diffuse and hard-to-monitor nature complicates measurement and reporting, implying actual emissions may exceed official estimates (Patel, 2023).

China published its Methane Emission Control Action Plan in 2023, prioritising the establishment of a methane MRV system. The plan outlines sectoral control measures and sets short-term targets, including manure utilisation in livestock, domestic waste recycling, and sludge treatment. However, it does not include quantitative emissions reduction targets nor binding commitments (MEE, 2023).

China’s 2030 NDC covered only CO₂, while the updated 2035 NDC expands scope to all GHGs, including methane. This broadening is a material step; however, the absence of standalone quantitative targets for methane or non-CO₂ gases limits accountability and may constrain mitigation outcomes (Xinhua News Agency, 2025d).

In its 15th FYP, China commits to strengthening monitoring and control of non-CO₂ GHGs, alongside implementing targeted mitigation projects for methane, nitrous oxide, and HFCs in sectors including coal mining, agriculture, and chemicals. These measures are expected to build capacity to reduce emissions by 30 MtCO₂e (National People’s Congress of China, 2026).

Further analysis

Latest publications

{kind=link}

Stay informed

Subscribe to our newsletter